Today I entered my first orders through TRADE using a “Market” order early in the morning (after market opened). For some of the stocks I bought, I got spikes of like 1-2% for my entry prices, although my order size was something like 1/1000th of the stocks’ average dollar volume . Immediately after my orders were filled at those high prices, those prices immediately went back down. I assume this was slippage, although I didn’t expect it to be so large.

This makes me wonder; should I have used a different order type? I simulated the strategy I’m now using live, and the (simulated) returns are basically the same regardless of my setting the fill price to “next open”, “next close” or “average of high and low”. So in theory I don’t care much at which time of the day my order gets filled. I obviously do care about impacting the market with my trades.

So what can I do to minimize impact? I supposed I could, for example, buy a couple of shares per minute during the day at market, but I’d prefer not to go through the hassle of that. Same with limit orders; I’d prefer not to have to monitor constantly whether the market price got too far away from my limit order.

So is there some other order type I could use? I saw there’s “vwap” and “pctvol” order types, but I’m not sure how these work. Are these a possible solution? Is there anything more or less automated I can use to minimize slippage/ market impact?

I currently don’t use IB to trade P123 orders. It also heavily depends on the liquidity and size of the stocks you are trading, as well as the turnover of your strategy. The 1-2% could easily result from the bid-ask spread if you are trading small and microcaps.

This is what I used to do:

1a) for less liquid stocks with lower turnover where it does not matter if you buy at the open or the close, or during any time of the week, you could set limit orders or trading algo that joins or creates and maintains a best bid (for buys), so you don’t have to pay the spread. If you really need to buy the stock on the same day, you could also use IB’s OCA (one-cancel-all) where you create multiple orders, linked together, so for example a Market-on-Open (MOO) or Limit-on-Open to join the opening auction, a limit order valid during the day (until 30 minutes before close), and then a Market-on-Close (MOC) order that buys the remainder of your unfilled order.

1b) for less liquid stocks where you want to be filled on the same day or asap, you can do a best-bid strategy, this will fill you soon, especially if you don’t limit your size participation because you are going to be small anyway.

for mid-liquidity stock you may do percent-of-volume or VWAP

for liquid stocks you could simply buy at the market, preferably during the opening auction, or just VWAP (if you don’t care when during the day you need to be filled).

I have noticed that it really matters a lot which execution strategy you choose for micro and small cap orders.

Very important question and it will probably be very important that you continue to evaluate slippage as you are doing.

I am looking at slippage in various ways and continue to look at different trade options. So, one small piece may be what you have just observed. It looks like at very small volumes–on the order of 1/1000 that you are talking about–volume is poorly correlated to slippage. It becomes more correlated at higher percentage volumes.

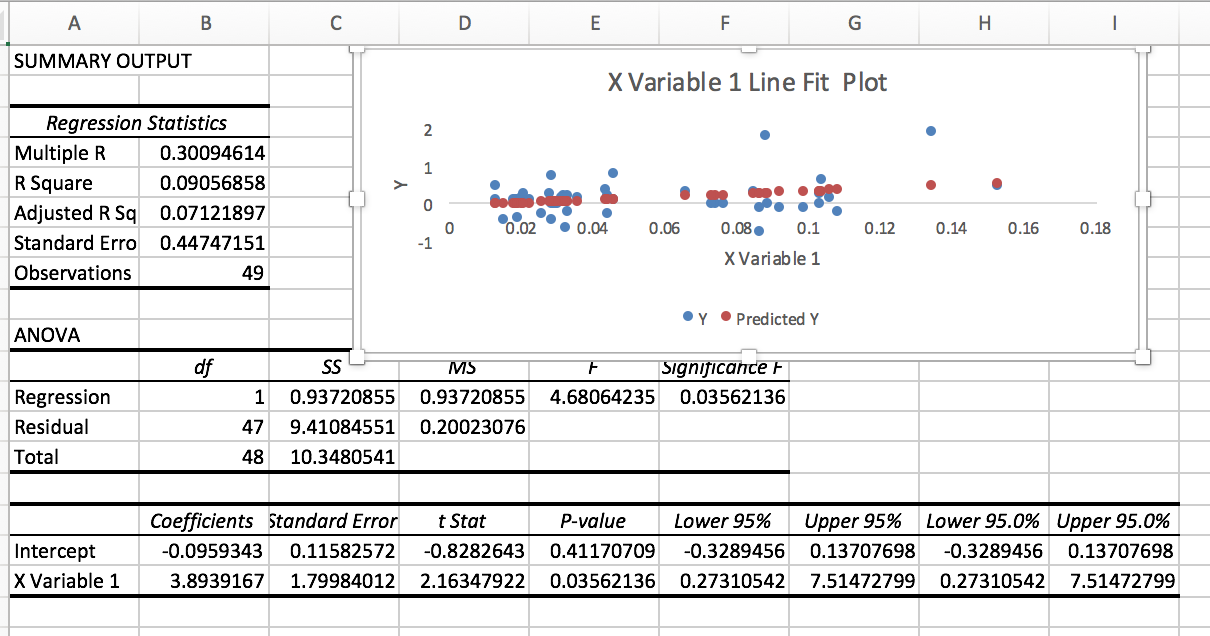

First these are window trades so you have to consider whether this applies to you. Note Folio Investing uses Knight Capital Group and does no internal matching now. So basically trades though a dark pool as you do but still significant differences.

This is the price just before the window compared to my fill price in percent difference. The x-axis = (percent deviation from P123 for one year) * (volume of my trade/Average 3 month volume)^0.5. This equation is derived from the literature.

You can see the R^2 is very small. The correlation does get higher for higher trade volumes.

I have been fairly satisfied with using Market On Open orders that participate in the opening auctions. It seems to be about the only time to trade in the early morning since bid-ask spreads decrease as that day progresses. I would be interested to hear others experience with MOO orders.

I use limit orders with the close price of the previous day plus ~0.25% (for small-caps), which fills most of the orders. One hour before market closing I check the state and adjust the limit of the unfilled orders.

Here is an interesting article on: “The Limit Order Effect” In the abstract they say: “We show that institutions earn large trading profits by triggering households’ stale limit orders…”

It would suggest that even when we have recent information from P123, there are institutions that trade against our limit orders with newer information that occurred after the P123 data updates. Examples might be earnings releases, changes in oil futures, or just news during the day after we have placed our morning limit orders. They may have most of the day to decide whether to take us up on our offer (or bid)–and they have no obligation to do so. It functions like an option for institutions.

This is probably something most of us do not have time to worry about. Besides, I am likely to trade the wrong way on the news anyway–i.e., buy (or sell) on the news rather than sell (or buy) on the news. A prime example would be the recent collapse of the OPEC (and non-OPCE countries) deal due to tensions between Saudi Arabia and Iran (April 17). I would have traded the wrong way had I used my discretion. One of my energy holdings at the time (SN) would have made 14% on the 18th alone by placing a limit order (as Sebastian does) before the open: the day after the deal fell through.

This is to say this may be a good way for many of us to trade. Still it is nice to know that we are doing our part in making sure that the institutions have a stable source of revenue–I wouldn’t want to have to bail them out again if they are “too big to fail.”

I’ve made longer posts and detailed comments in the past, one of which has already been linked to in this thread, but I’ll throw in a quick paraphrase again since it seems apt.

If you’re trading a TINY amount of the ADV, like <.1%, then market orders are a viable option to you. Your order isn’t large enough to stand out or be exploited and you can virtually always get a quick fill at the current bid/ask.

If you’re trading a SMALL amount of ADV, say <.5%, then limit orders are okay. You can likely fill quickly at a price you’re comfortable with and although your order will be visible sitting on the book its small enough to not be easily exploitable or significantly move the price.

However, over large samples algorithmic order types will always result in better fill prices for orders of any % of ADV. If you’re trading more than 1%, and especially if you’re up in the 5%+ range, then you really need to be using order types that break your order into many small lots and fill over time. You will have less market impact and achieve better transaction prices.

If transaction costs are important to you then stop using market/limit orders.

IB just announced a new “adaptive” algos. From the announcement…

Marketable orders generally result in a fast fill. Non-marketable orders may deliver a better price, but may take a long time to execute and may not even get filled. Enter the Adaptive Algo, the newest member of our growing IB Algo family. The Adaptive Algo aims to deliver the best of both worlds. By adapting to market conditions, it attempts to achieve the fastest fill at the best all-in price.

Most useful when the spread is wide, but could also be helpful when the spread is only one tick.

Works with any quantity. The adaptive order will automatically break large orders into smaller chunks to avoid overwhelming the market.

Easy to use. Just set the buy/sell action and order quantity, then select the algo from the order types list.

It can be used as an Adaptive Market or Adaptive Limit order depending on your objective.

Adaptive Market - Unlike a simple market order that hits the ask and fills (for a buy order), the Adaptive Market buy order dynamically selects and varies the price in an effort get a fill at best all-in price.

Adaptive Limit - Works similar to the Adaptive Market order, but uses the limit price as a cap. Like a simple limit, the Adaptive Limit will only fill at the specified limit price or better.

The user can tweak the behavior of the algorithm by setting the urgency from the drop-down selector. The available choices are: critical, urgent, normal (the default) and patient.

I’ve been playing with the new order type a little. At a glance it looks like a solid and simple option when trading a small (<1) % of ADV. I’m not sure how it will work on low liquidity or very large orders, but that’s not really its intended niche anyway.