Anyone interested,

I found a formula for market impact of a trade: Link Here

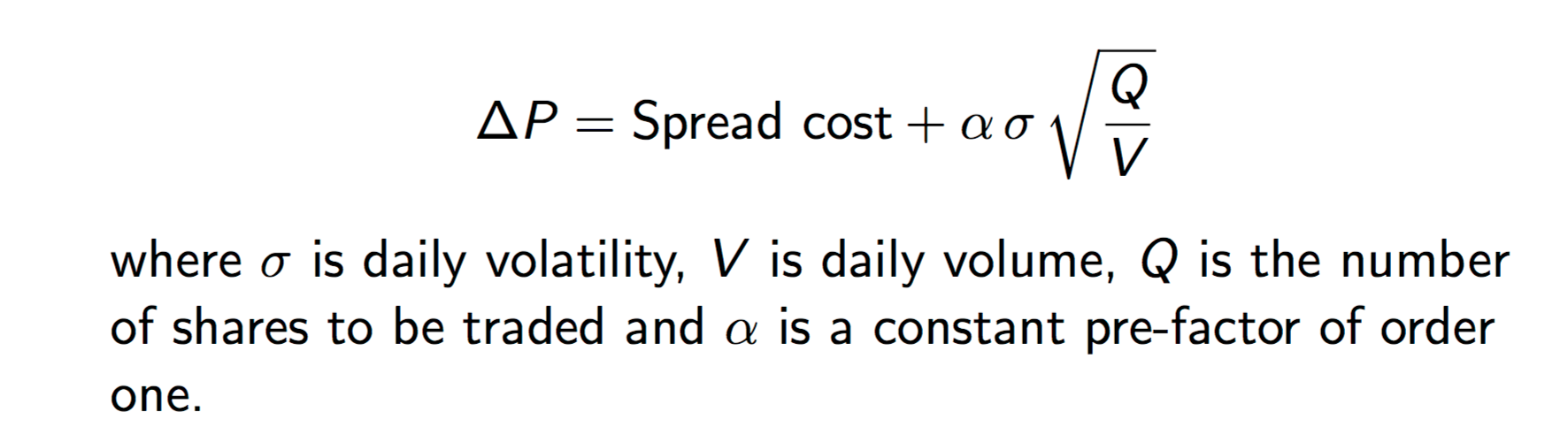

I also attached the image of the formula.

There are other articles and this is used by in the Bloomberg Terminal for their Transactional Cost Analysis (TCA), for example.

The formula is in this one too with a lot of calculus that I did not wade through:Page 16. I found the sage advice of old traders interesting: “this formula is consistent with the trader rule-of-thumb that says that it costs roughly one day’s volatility to trade one days’ volume.” Trade a whole days volume? Wow!!! And I am just worried about increasing my trade size by $5,000.

This last article does say there is evidence that this formula holds for trading sizes in the 1% to 25% of daily volume range.

I researched this because I want to increase the amount of money in one of my ports without impacting the slippage too much. Can I? If so how much more can I put into this port?

So a hypothetical example with round numbers (somewhat close to my situation). Say each trade in my port is $5,000 and my ADT is $1,000,000 for the bottom 20% of liquidity. Can I increase my trades to $10,000 for each trade?

5,000/1,000,000 is the same as Q/V * (stock price/stock price). I.E., I can multiply Q/V by 1 and use trade cost/ADT in the equation.

The constant in the equation is generally about 1/2 in most articles (see the graph in the link).

Using ShowVar I find generally my daily volatility or the standard deviation of the daily percent change in my stock price is 3% or below for the last year. Using this variable converts the equation into the percent change in price rather than the absolute change in price. This is in essence dividing both sides of the equation by the price of the stock and multiplying by 100.

So the percent change in price (slippage due to market impact) is: 1/2 * 3 * sqrt(5,000/1,000,000) = 0.106%

If I increased my trades to $10,000 per trade the calculations come to 0.15% or a difference in slippage of 0.044%. The BID/ASK (spread cost) would be the same for either trade size.

This seems low. But the calculation is conservative considering this is calculated for just the bottom 20% of my liquidity. Presumably there would be little difference in market impact for the S&P 500 stocks in my port. Even if I am off by a factor of 3 it would mean that I should have tried this a long time ago. Of course, if I do increase my trade size I will keep track of the result as best I can. I get that a formula and a lot of hand waving proves nothing: trust the papers and the better experts but verify.

Any ideas, experience in the market or corrections welcome.