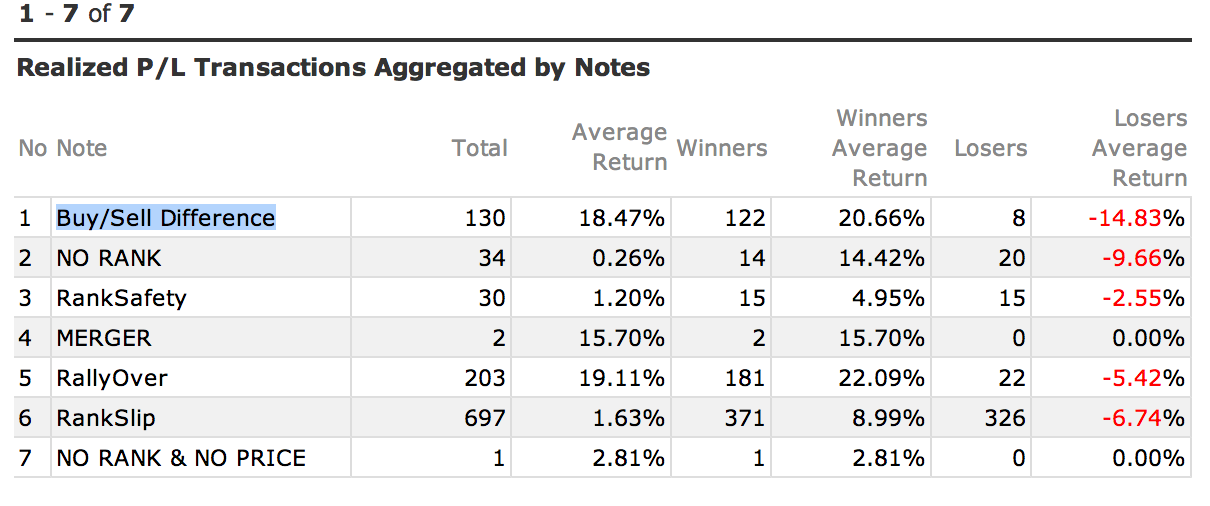

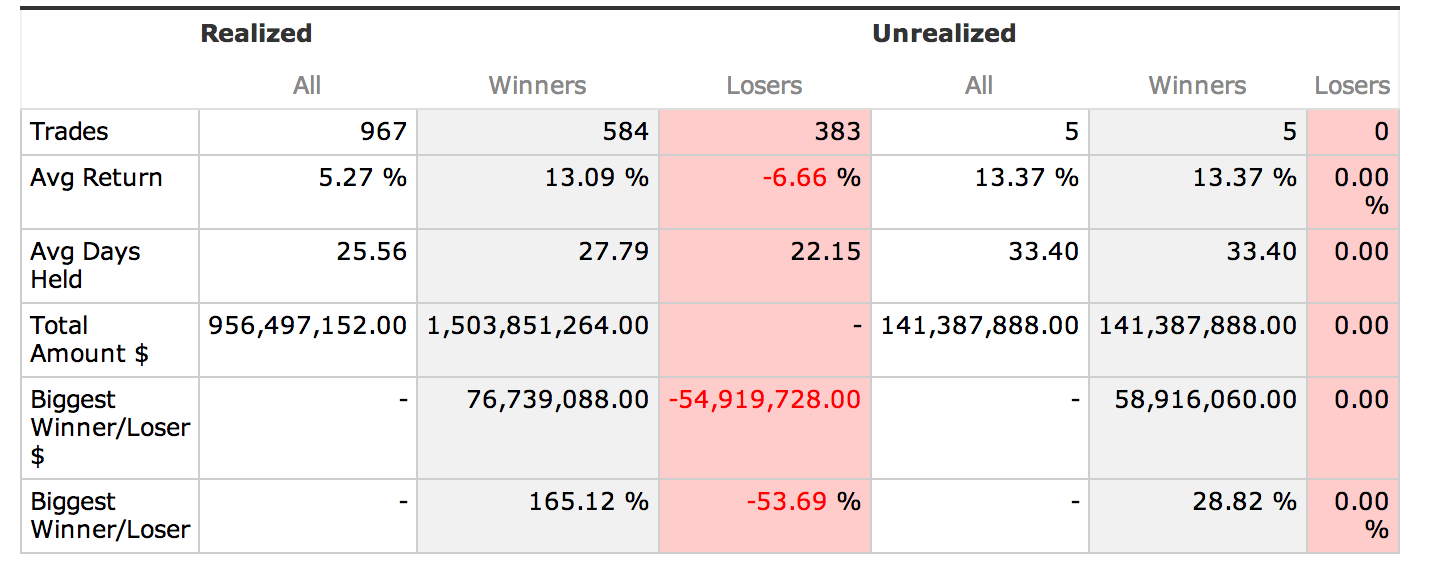

One of my favorite tools is the transaction summary under simulation’s “Transactions->Realized->Aggregate by Transaction note or sell rule”. It’s very helpful for identifing which rules need more work and how the rules behave when I test for curve-fitting. Anyway, I’ve noticed that the realized avg return (under Statistics->Trading) is very different (lower) that what I calculate from the “Aggregate by Transaction note of sell rule” summary. I can reconcile them only if I ignore the “Buy/Sell Difference” data of the latter. Unfortunately, for me that leads to significant differences.

Is there a reason to ignore the “Buy/Sell Difference” data?