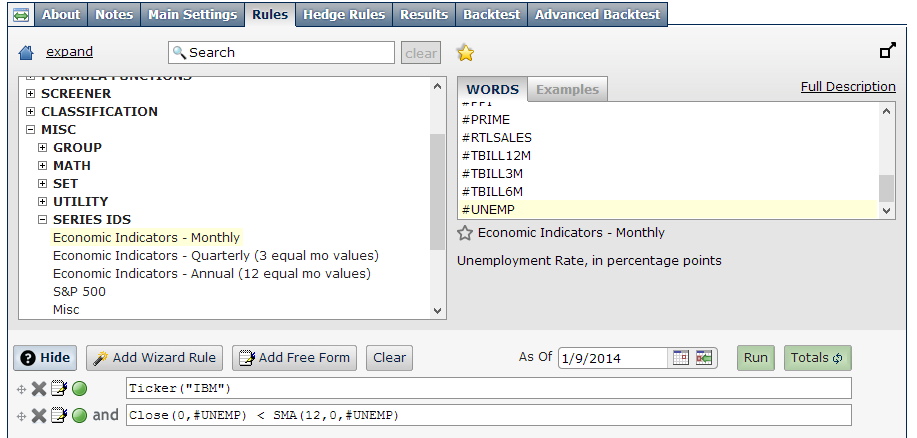

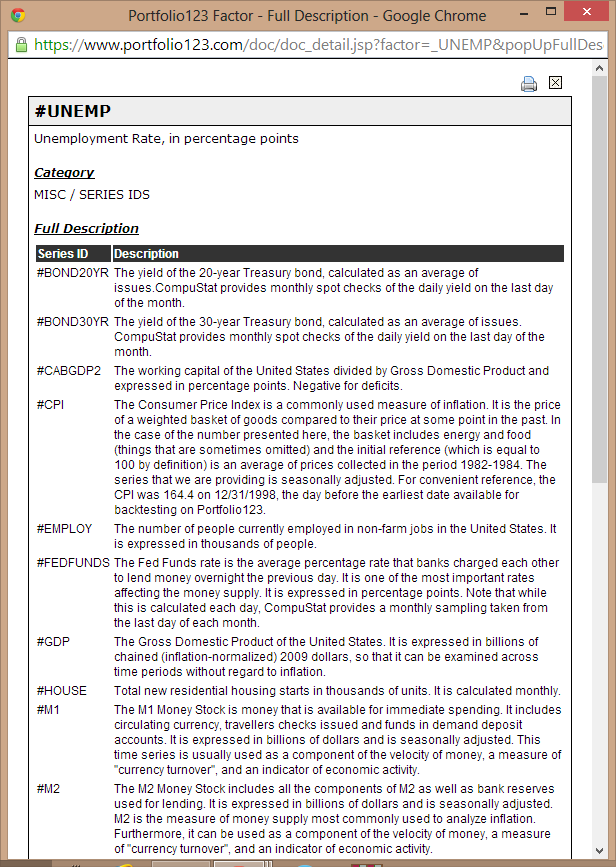

You can now access a variety of economic indicators such as unemployment, GDP, CPI etc. At the moment they are only accessible in technical functions that allow the “series” parameter, like Close() & SMA(). You will find the Series-IDs in : MISC->SERIES-ID.

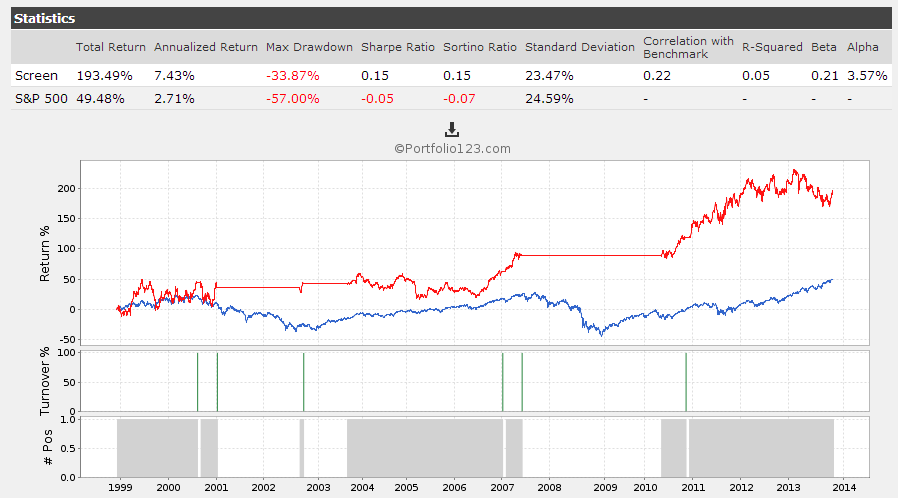

Please see the images below of a screen that buys IBM only when the Unemployment rate is below its 12 month average, in other words, only when the Unemployment is trending lower.

Much more to come. Let us know what you think.

NOTES:

The values are NOT true point-in-time. Economic are often revised and we only have the latest revision. Compustat does not have the data for us to create point-in-time data. We have plans to create point-in-time data from other government sources. However, we did some analysis, and it may not be all that significant (revisions don’t really affect the overall trends)

At the moment using these indicators is a bit cumbersome. We are planning a complete separate tool and pre-built ratios that will allow you to easily create a timing signal rank based on these indicators.

Great addition to P123. I have been using the unemployed data for recession prediction in this model http://www.advisorperspectives.com/newsletters12/The_Unemployment_Rate.php

Nobody should be long the market during recessions. Tomorrow (Friday) I will update this model and you can see it at dshort.com or at imarketsignals.com.

This is the only data that goes back to 1948 and the unemployment rate has consistently been a good indicator for recessions.

Wow… just when I think it can’t get any better here you keep pulling out the stops! Thanks Marco. I am truly impressed - this will help with market-timing A LOT.

At the moment, we’re using a limited dataset consisting of items included in our regular Compustat downloads and which we have been able to identify and match up on the federal Reserve platform. Over time, there are many more series that can and will be added when we take data from the Fed, as well as additional functionality.

I would not want to describe this initial launch as a beta; the data is fine and we’ve got Series functionality down pat. Instead, consider it a starter set; something with which we can get our feet wet. And as we gain collective experience with the economic data, we’ll be able to fine tune our ideas on what what else we’ll need and the kinds of functionality that will help us most effectively use what we have.

Remember this P123 data is monthly. Also this economic data is available outside P123 for about 50 years, some daily, weekly and monthly. Most of it can be downloaded from FRED. If you want to use it for market timing you should test your timing rules in a spreadsheet spanning over the last 50 years, which includes 7 recessions. If your market timing rules work over this period then you can use it also for P123 sims. I would not assume that market timing rules based on only the last 14 years’ economic data at P123 will work under all market conditions.

FYI, these are the next steps for the econ indicators:

We are doing a project to download from FRED, point-in-in time, 50y+ of econ data.

We will make this data available in the the multi-factor “economic/timing” score tool we’re planning which will let you backtest using all the data, and then use the signal in portfolios , hedging, or screens.

The timing score will work much like a Piotroski screen. The Piot screen has 9 true/false conditions, and you can, for example, buy stocks that pass 8 or more conditions (doesn’t matter which). The new tool will let you specify multiple conditions(rules) based on econ trends, SP EPS, etc. The score is the weighted sum of the conditions which you can use in rules, hedging etc. You will be able to specify multiple scores for exiting the market or re-entering.

The final addition will be to add market-breadth factors in the timing tool.