I would like to launch :+:Quantonomics 3 US Sector ETFs:+: . It is combo of market timing and sector rotation strategies on the 10(9) GICS SPDR ETFs.

When I click R2G, it says 5 holdings minimum. But the issue is that 5 out of a universe of 10 (9) sectors is too much. 3 holdings is the optimum in my test.

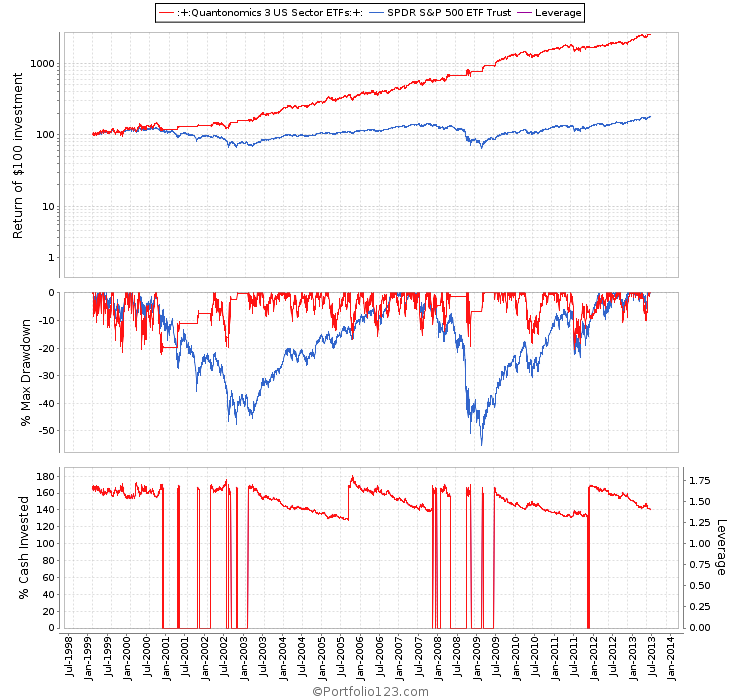

Here are the stats:

1.5 Leverage (Margin Account)

300M$ Bottom 20% Daily Liquidity

+25.0% CAGR 1999-2013

-22.5% Max DD

80%+ Winners

140% Annual Turnover (you trade once every 180 days).

0.70 Correlation

For potential subscribers:

This ETF Portfolio is great for investors who cannot own a diversified portfolio of stocks AND/OR who doesn’t have time to follow individual companies AND/OR who wants just to have access to the market timing signals without buying my stock models… You just fire a market order once in a blue moon on three ETFs and sleep on it - that’s it that’s all.

For current subscribers:

This model may be considered as the CORE of all my future stock models. You can subscribe to it if you want, but I will eventually update my previous models to include the components of this model. That way, you will hopefully be able to gain the alpha of this new market timing/rotation system combined with the stock picking alpha of the older ranking system.

Can you bend the rules for ETF Portfolios and allow the creation of mine? ETFs are already well diversified, specially the ones I chose and they have tons of liquidity. I’m sure there would be high demand for this R2G ETF Portfolio.

List of all compliance issues:

Minimum positions 5: Lower it to 1 for ETF Portfolios.

Ticker not allowed: Allow Ticker(“XLY,XLK,XLU,XLB,XLF,XLP,XLI,XLE,XLV”)

Leverage not allowed: Allow Leverage now that it works for stocks.

Q, no need to bend rules, they have not been implemented for ETFs. And it would be nice to have ETF R2Gs

I think I agree with all the ones you mention. I would also remove the bottom 20% liquidity check of at least 50,000. That’s because some volume data is missing for some etfs.

As far as margin, the Maintenance Margin must be at least 35% and the Margin Call Action ‘Stop’. This way a sim that generates margin calls cannot be launched.

The inverse of 35% is 2.85 leverage. Your highest appears to be 1.75. Maybe 40% Maintenance Margin is better.

Pretty sim. 3 sector US stock ETF rotation is a lot more stable than a 5 stock microcap port. with 1000% turnover and low liquidity. So, agree with your general point that there is not really a reason to exclude it in this case. But, opening up custom ticker lists on backtests opens up whole worlds of ‘overfitting’ issues - that it may be hard to make general rules for. So, that’s one complicating factor.

Question: How will you be able to use the info. from sector rotation in a stock sim through P123 - if at all? Somewhere in the past, I had a feature request to use 1 sim as a timing rule in a second sim. Some modified form of that would be needed, right? But if would be even more complicated. Would need an If XSim holding = X, then Y Rule (Sector = xxx), right? Is there a way to do this now?

Are you going to use this to create a custom list? Curious how you plan to handle this.

And why daily rebalance? Assume it’s sell rule or market timing rule (or profit taking) related to smoothing backtest. But, don’t know if this is practical right now on R2G’s? How much is the fall off for weekly?

Tomyani

I don’t want ticker(), I just don’t have the choice. The universe builder for ETFs is not granular enough to allow the filtering of only the 9 SPDRs. I end up with a Bank ETF, a Software ETF, etc. that’s why I have to use ticker(), not because I want to overfit. Give me the universe I want and I will be more than happy to to not use ticker() anymore in the buy rule.

Since the portfolio turnover is only 130-140%, placing the model as weekly will only reduce the turnover more but the reduction lowers the return because some market timing signals happen during the week. Don’t get me wrong it’s still very good in weekly but if changing to daily is just 130-140% turnover, then it’s not a big deal. I will show the weekly version if you want.

But we’re going to relax a few restrictions and instead “flag” uses of functions for potential curve-fitting. These flags will appear prominently in a “disclosure” section and the will be required to explain.

Specifying Ticker(“XLY,XLK,XLU,XLB,XLF,XLP,XLI,XLE,XLV”)

makes this simulation not survivorship bias free. This is the same as specifying a stocklist with the now known losers weeded out and backtesting it back to 1999. You get very high returns this way, I have tried it.

While in general I agree about custom ticker lists, specifying all of the possible SP500 sectors is very mild in the world of cherry picking a universe. Much more mild than many other rules likely already in R2G’s. Its saying you want to test sector rotation within large Cap S stocks to see if it makes sense. The model itself still may or may not be optimized based on other rules. But sector rotation is viable objective.

In fact the non-disclosure of simulated performance with and without all market timing rules is a much greater and wide spread potential abuse of curve fitting.

Not at all, what are you talking about? You talk like if I was trading stocks when I’m actually trading ETFs. If you take SPY, you break it in it’s 10 components and you have all of them, there is no bias. If I would voluntarily omit a sector and only kept the performing ones, you would have a point. The only sector I don’t have is Telecom - not because it’s a dog sector - but because SPDR never released such ETF because it’s essentially just three companies: Verizon, AT&T and another one historically. Vanguard eventually released a TELS ETF but let me tell you: this model would do better with TELS so it is a disadvantage not to have an existing ETF for it. If anything I’m penalized and my excel spreadsheet proves it.

This is the same thing if I launched a model that allocates between Russell 2000

Value and Russell 2000 Growth. Your thinking is that I would create a bias by choosing these two sub-indices… No… If my benchmark is Russell 2000 and all the companies are sorted either in the Value or Growth basket, there is no bias.

And there it is. A perfect example on how “flags” and the new disclosure feature would work. Ticker() can be mis-interpreted, but should be allowed with explanation. If the explanation is not clear, misleading, simply choose another model.

I’ve even found cases where I needed Ticker() in regular stock sims due to some crazy data which , while technically not wrong (meaning S&P won’t change it), caused spikes in sims . I can’t recall which ticker at the moment.

Remember that rules cannot be changed once launched. So Ticker() with proper explanation, should be allowed. We can put checks so that the explanation matches the exact Ticker() function.

A) I updated the settings with 40% and stop as you suggested. When do you think I my ETF R2G can pass the test? I will work on it more but just to have an idea. Thanks alot for helping create ETF R2Gs.

B) Can you allow designers to manually uncheck some ETFs in the universe filter/creation process? For example for SPDR General Financial United States Equities I will have Financials ETF and Banks ETF. Banks is a GICS Level 2. I don’t want the Level 2s like Retail or Software, I would like to remove them before applying any ranking system. They can affect my ranking system because with Bloomberg I don’t have them in my backtests.

C) By the same token, might as well reclassify Utilities as General.

Thanks again Tomyani & Marco to explain why Ticker() can be mandatory in some cases.

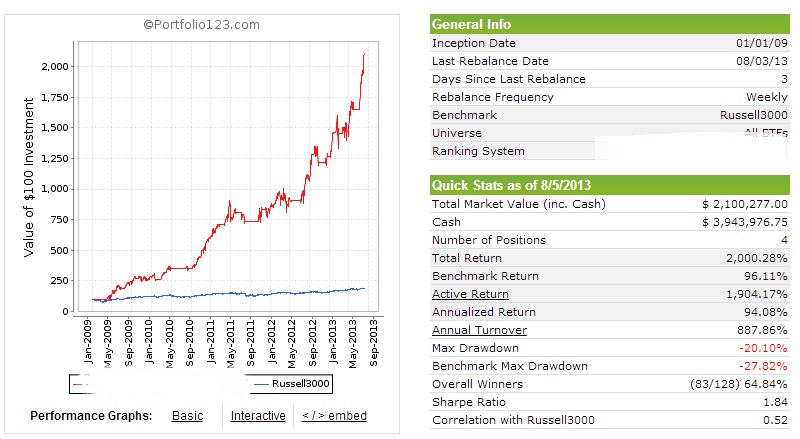

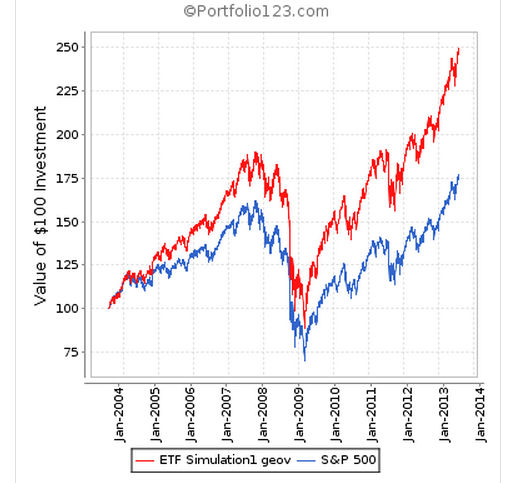

Q, nice sim, kudos. So your market timing exited the market ~12 times (if I see correctly from the chart) in the time span on record. How many rules does the timing system use, is it one rule or did you need multiple rules to exit 12 times?

Thanks, Zvi

Hi,

Any chance that leveraged ETF strategies would be allowed, and therefore limited history as well? It really opens up possibilities. This strategy can only be tested accurately from 2009, but it trades ETFs with $25M liquidity. You just can’t get this with $25M stocks.

I understand many ETFs got their inception recently but I don’t think it’s a good idea to launch an ETF R2G without at least one bear market. I think the minimum date would have to be either 2006 or 2007.

Here is my sim, select only one from XLU, XLP, XLI and XLE.

With leverage of 2, I get a CAGR=30.0% and a max drawdown= 36.7%.

Seeing we can now pick the Sector funds we like, then this should be an acceptable R2G model. It is also useful for retirement accounts, where one can then rotate between then sector funds according to this model. Also only 53 trades since 99 and lots of time in cash. We need to be able to hedge when in cash with interest bearing ETFs.

Wow you clearly do not understand the concept behind R2G ETF Portfolios. You need symmetrical universes or sum=1 universes. Therefore if you want to do a US Sector R2G, you must use the 9 SPDR starting in 1999 or the 10 Vanguards in 2006-2007 or the 9 SPDRs + 1 VOX. This is the only way acceptable. Yours is a mere cherry pick of what worked in the past but if you can do the same the way I told you, then great. On an financial institutional level, your model is deeply flawed. I’m surprised you don’t even grasp what we have been discussing since you first posted about ticker().

If you want to do an international ETF strategy, the only way acceptable would be to separate countries in DM and EM. And rank by GDP adj PPP. And maybe create a universe of X DMs: Us, Japan, France, Germany, UK and equally X EMs: China, India, Russia, Brazil, Mexico. Only then you make your model around this… No cherry picking of countries.

The difference between yours and mine is that I didn’t choose my sectors beforehand while you did. Me choosing all the sectors is not a cherry picking because they are all there.

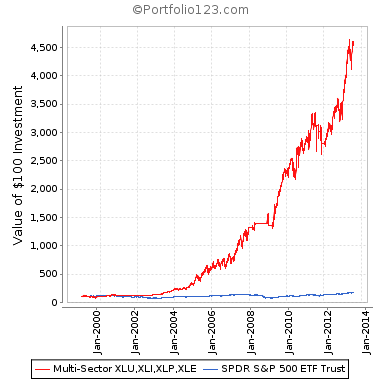

Well obviously ticker(“common sense”) goes at this stage. Since you provided a universe of four cherry picked US Sector. Let me show you how your four cherry picked US Sectors actually performed in the past:

1926-2013 (The Forest) AND 1999-2013 (The Tree) 10 Sectors [Ln Scale] vs. your Four Cherry Picked Sectors

Morale of the story: if you create a R2G ETF (or if anyone manage a fund in real life using any kind of equity-based sector rotation), you need to break down a whole index and backtest on all its sub-indices components in a best effort basis (depending on availability of the components as tradable instruments). If they are all readily available to trade, use them all. Anything else is cherry picked, and theoretically not sound / correct. In real life, I have S5TELS in my backtest and if I ever need to buy TELS, I would either buy the three US shares or I would grab the new ETF by Vanguard VOX but it is not traded with too much volume so I sometimes go with Verizon, etc.

The sim must be submitted for approval. I will then turn off every rule, buy or sell, except Ticker() in the buy rule. Maybe also force a rebalance to equal weight every 6 months or so. If the sim , which now buys only the ETFs in Ticker() grossly outperforms the S&P, then the ETFs were cherry picked.

If it doesn’t, then it the combination of ranking and the other buy/sell rules that is generating the alpha, and is allowed to be launched.

And all ETFs should have long enough history and a Management Fee imposed.

Here’s Geov ETFs, equal weighted every 6 months.

Ticker(“XLY,XLK,XLU,XLB,XLF,XLP,XLI,XLE,XLV”)

Is this cherry picking ?

Maybe a tad, but compared to his returns with his complete system, sure looks like alpha to me.

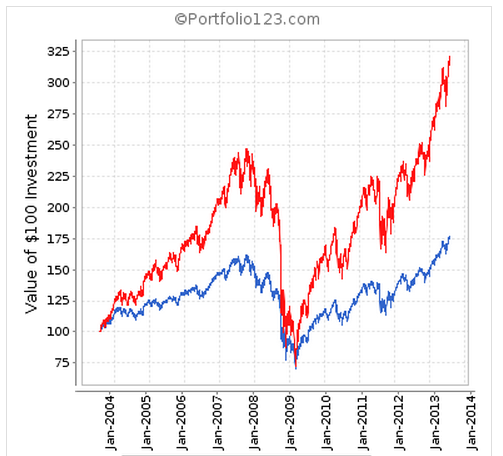

Second image is 1.5 levered with 2% margin cost

Lets not forget that equal weighting is also what make a portfolio of all SP500 outperform by a wide margin the market cap weighted S&P.