Marco,

Will you give us an educated guess as to when you will be able to update the open prices to the actual open price?

I want to postpone re-running my ranking systems and Sims until that can be accomplished.

Denny ![]()

Marco,

Will you give us an educated guess as to when you will be able to update the open prices to the actual open price?

I want to postpone re-running my ranking systems and Sims until that can be accomplished.

Denny ![]()

Bump

Marco?

It’s two projects in one: updating prices around 10PM and bringing in the open prices from our IDC historical dump. It’s the next project after we flush out the main bugs. Working on IndWeight/SecWeight now which is very important. Certainly by end of next week, hopefully sooner.

Thanks Marco, that will be great!

Denny ![]()

Hi Marco, can you please update regarding this one, are the open prices prior to 2004 correct now?

Thanks, Z.

There are two ways to do it, one involves updating Compustat data, the other mirroring the data then updating. Each has its own set of problems. We’re asking Compustat what they recommend. Should have something end of this week.

Marco,

Any update on actual open prices?

I am holding off re-running most of my Sims, Ports, and Ranking systems until we have open prices back to 1999.

Denny ![]()

Denny,

Compustat suggested we mirror the price data in our own database and update the open prices. Obviously they don’t support/like clients manipulating their database, so that any changes that come from them do not over-write ours.

This has merits and drawbacks. I was leaning towards updating their data, so we don’t have to worry about keeping two sets of data in synch. I seriously doubt they would make any updates to price data that is 4+ years old since it’s not even their data (it’s IDC)

However having our own copy of prices has one major advantage. We can populate the last bid/ask since we have that from IDC. This bid/ask spread could be used to automatically compute slippage for each stock. It’s not the only way to have a variable slippage calculation (we could look at price, volume, etc) but it’s probably the most accurate.

How would you rate that feature to help us decide which course to take ?

Thanks

Marco,

I like the idea of using IDC’s data best. Have you considered using your own point in time Reuters’ data? I realize it only starts on 3/31/01.

It would be interesting to run a comparison test between your Reuters’ data and IDC’s data. We might be surprised by what you find!

Denny ![]()

Marco,

Will you give us an update of when we can expect to have actual open prices prior to 08/27/2004?

Thanks,

Denny ![]()

Updating the open prices was discussed first in This Thread shortly after converting from Rutgers data to Compustat data.

However, with all the great accurate point-in-time data in the P123 data set there is no reason that the update to actual open prices hasn’t occurred yet. It has been a year and half since it was discussed. I realize that there are problem with updating the open prices to actual prices, potentially changing Sims, Ports, R2G, Ranking System performance, etc., but come on now, P123 already has the data!

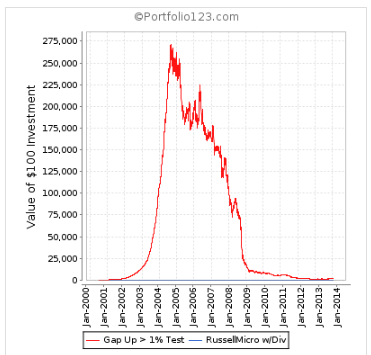

In a few recent threads there was discussion about buying & selling stocks after gaps up & gaps down. Back before the conversion from Rutgers data to Compustat data I tested many cases of gaps up to find methods that implied when to buy and when to avoid gaps (the Rutgers data had actual open prices). I have been running a live Port based on those results every since then with good results.

I just ran a Sim using the new data and found very erroneous results from 1999 to 08/27/2004. The average of Hi & Low greatly distorts the results in that time frame. The below Sim was designed to specifically show how much error there is prior to August 2004. The Sim gained 2,750% prior to 2004 and then lost 99% since then.

Denny ![]()

Bump, any update?