I assume this means there may be some survivorship bias.

Just to be clear, P123 technically maintains control/owns the models even if they are removed by the designer? You don’t happen to have the data on all of the designer models without survivorship bias do you?

If so can we see that?

BTW, I fund a port. We will see how it does out-of-sample. But I think there may be some value at P123.

My point is that, taking my surviving ports that are on auto, sorting them to show the best ones that I am still running would not be very good proof that I can make a good model.

It would not be proof that I cannot make a good model either. Actually, it would not show much of anything.

Taking the results of all of one one’s models that are funded (as Marco does for his ports here) is good evidence, however. Not proof perhaps but evidence that he might be able to make good models. And I would certainly hope that would be the case.

Thank you for sharing that Marco.

Can we get some more solid evidence? See my comments above about the possibility of getting data with no survivorship bias (somehow).

Maybe start a good sample of models from Yuval Dan and Marco that are never removed if P123 will not show us designer models with no survivorship bias?

BTW, Yuval’s designer models have little survivorship bias and he has removed zero models recently. But also he is just one model designer and there is a bit if a multiple comparison problem if you just look at his models. Still, there is some evidence for the value of P123 in Yuval’s results.

P123 does have ways to prove there is value in its ports (assuming there is value there). And to even quantitate that value in a rigorous way.

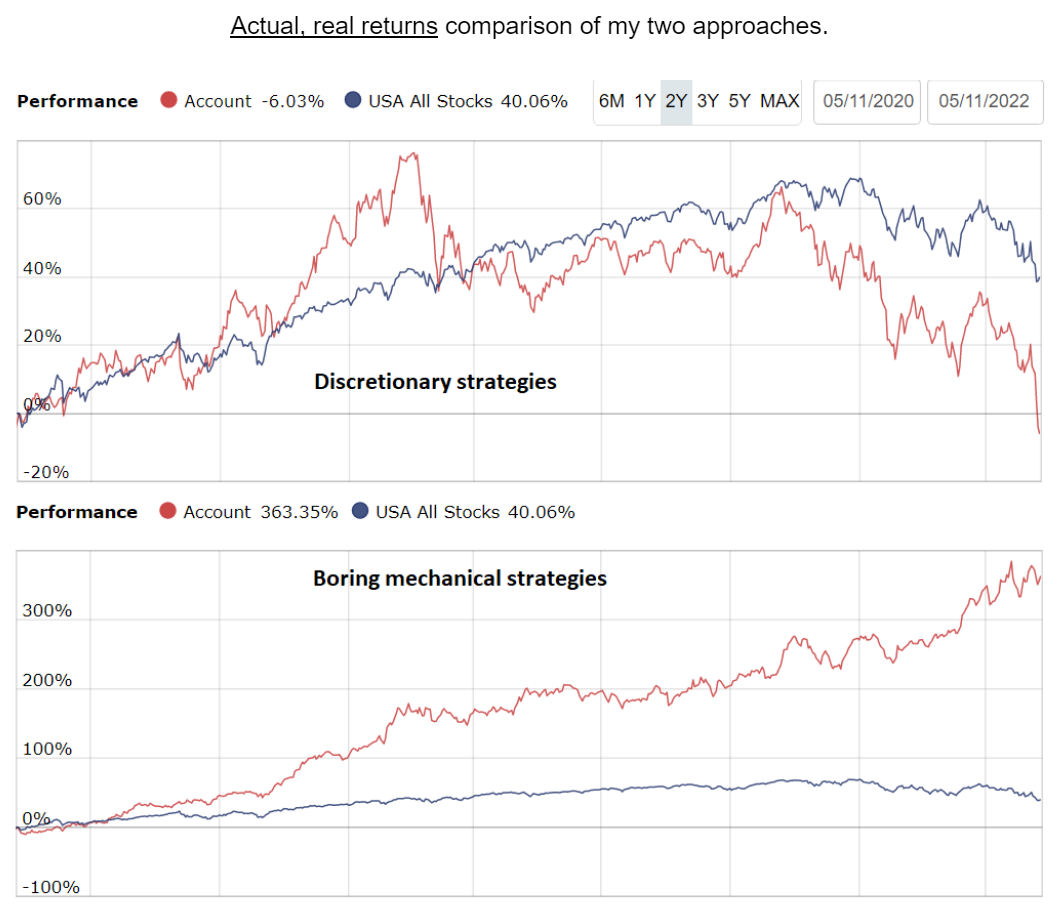

BTW, to be balanced (with Yuval’s generally good results) and to see the multiple comparison problem as well as the problem of looking at just the last 2 years, has anyone looked at Marc’s results recently? Alert: Serious survivorship bias there.

Jim