I realized I was making my discussion about risks too theoretical. Also I was not sharing my own data as others have generously done. My view on risk can be simplified to:

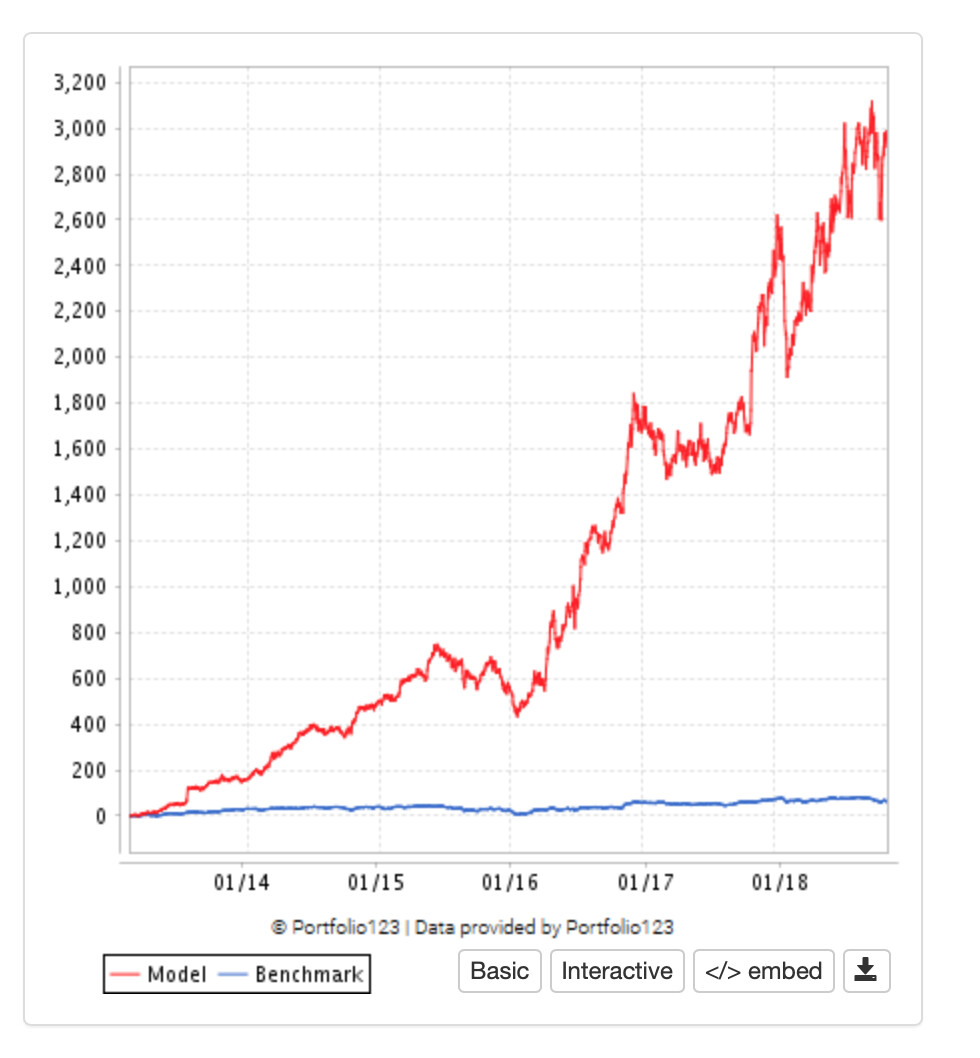

Sometimes it works (first image)…

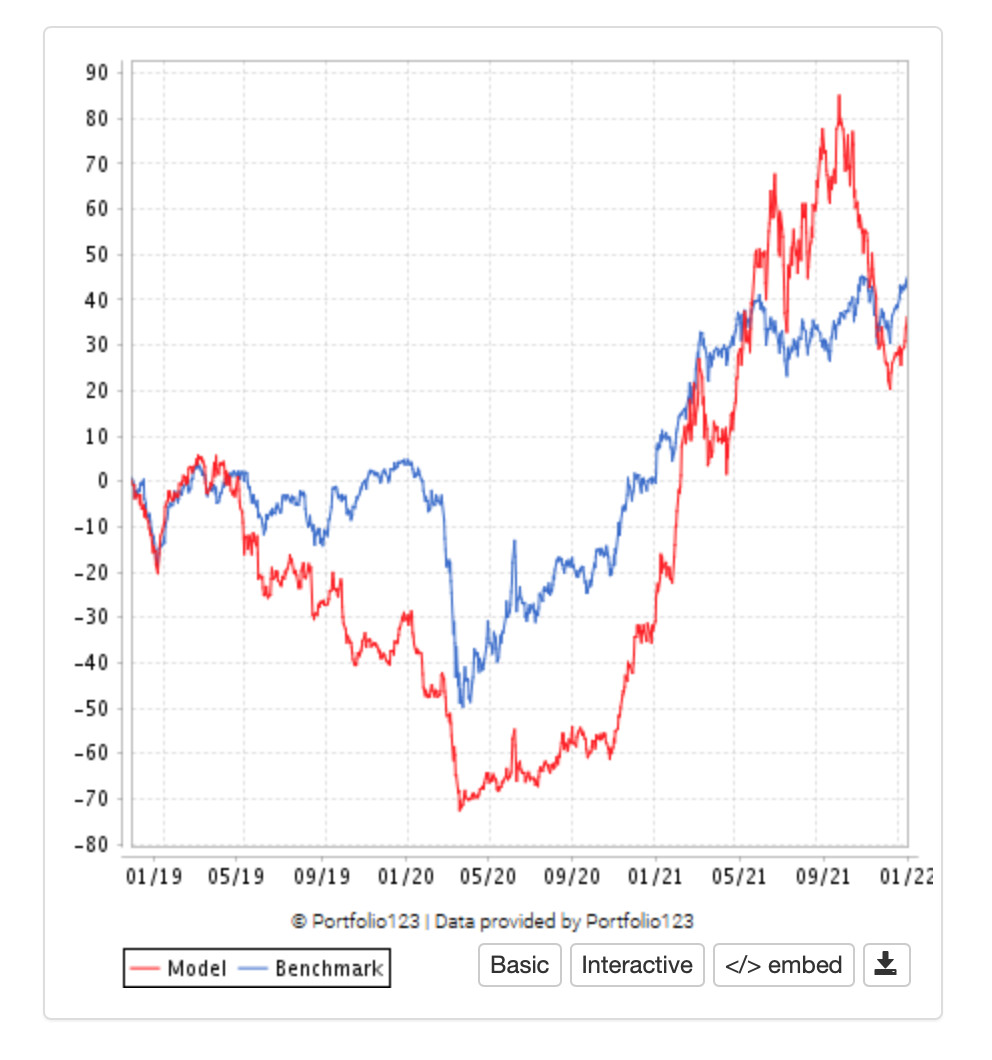

…until it doesn’t (second image).

I started here in 2013. This does not represent my entire portfolio since 2013. I am not saying I was full invested in this at all times. I am not going to look through my brokerage account and try to fill in those details: there are better things to read if you have trouble getting to sleep–assuming I got it right in the first place. I have changed brokers making that potentially impossible, anyway. It is accurate to say I have zero dollars invested in this strategy today.

A discussion of how much was invested in this strategy, how that changed over time, what I should have done in retrospect, or what I will do going forward might start to get back into that “too theoretical” discussion. But it is clear that “sometimes it works until it doesn’t” is a provable fact (proved in this post actually). I think I will leave it at that for now.

Jim,

part of the problem with this sim seems to be for me, that from 2017 on more and more people have started trading similar strategies. And because the earlier growth of the sim did not correspond to a quite exceptional long-term growth in the prices of the assets contained (?), the outperformance had to go back.

…But perhaps this is rather misleading, and the strong recovery of the sim since spring 2020 shows, that it has still outperformance potential. So, if you can wait 5 - 10 years, you will know better.

You have several good points that I agree with. I don’t disagree with anything you said.

I agree that the port might do well again. In addition, the sim was overfit, I believe. Maybe I have something a little better now. I do not know if it is actually better but I am fairly confident that what I might use going forward is less overfit.

The other thing is that most recently the problem with the sim is more its volatility than the returns. The returns are about the same as the benchmark which is not good. But it is not super-bad either.

I have touched on the idea in other posts that beta is not always bad. The largest hedge fund in the world uses what it calls “beta strategies”: Bridgewater Associates

I am still trying to understand some of what Ray Dalio does. But my working idea is that beta is not always bad and that Ray Dalio may have a point. I am still learning, however.

It is clear that Ray Dalio does what he does with risk in mind. But at the same time, he does not hate beta everywhere finds it. I am not advocating my father’s ideas on risk to be sure. Which is not to say I have fully developed my own ideas on risk.

What I am trying to add to what you have said is that even if the port produces no alpha going forward it may not be a bad idea to put some money into it. And I cannot predict the future. It may begin to produce some alpha in the future, as you suggest.

That’s my long way of saying I think you are right and I am probably going to do what you are recommending.

The earlier performance greatly outperforms the benchmark while the latter performance looks similar to the iwc etf vs spy etf. This can happen with bad luck (factors lose favor, picking an unfavorable universe, or a low turnover portfolio with an unfavorable entry point) and/or over fitting. Ways to decrease but not eliminate this risk are multi factor portfolios, bigger or different universe, multiple entry points or increased turnover, and a sensitivity analysis (change all the portfolio parameters including the universe and time frame to look for a slow degradation in performance). I’m sure you thought of most if not all of these ideas but I’m putting them here in case you didn’t.

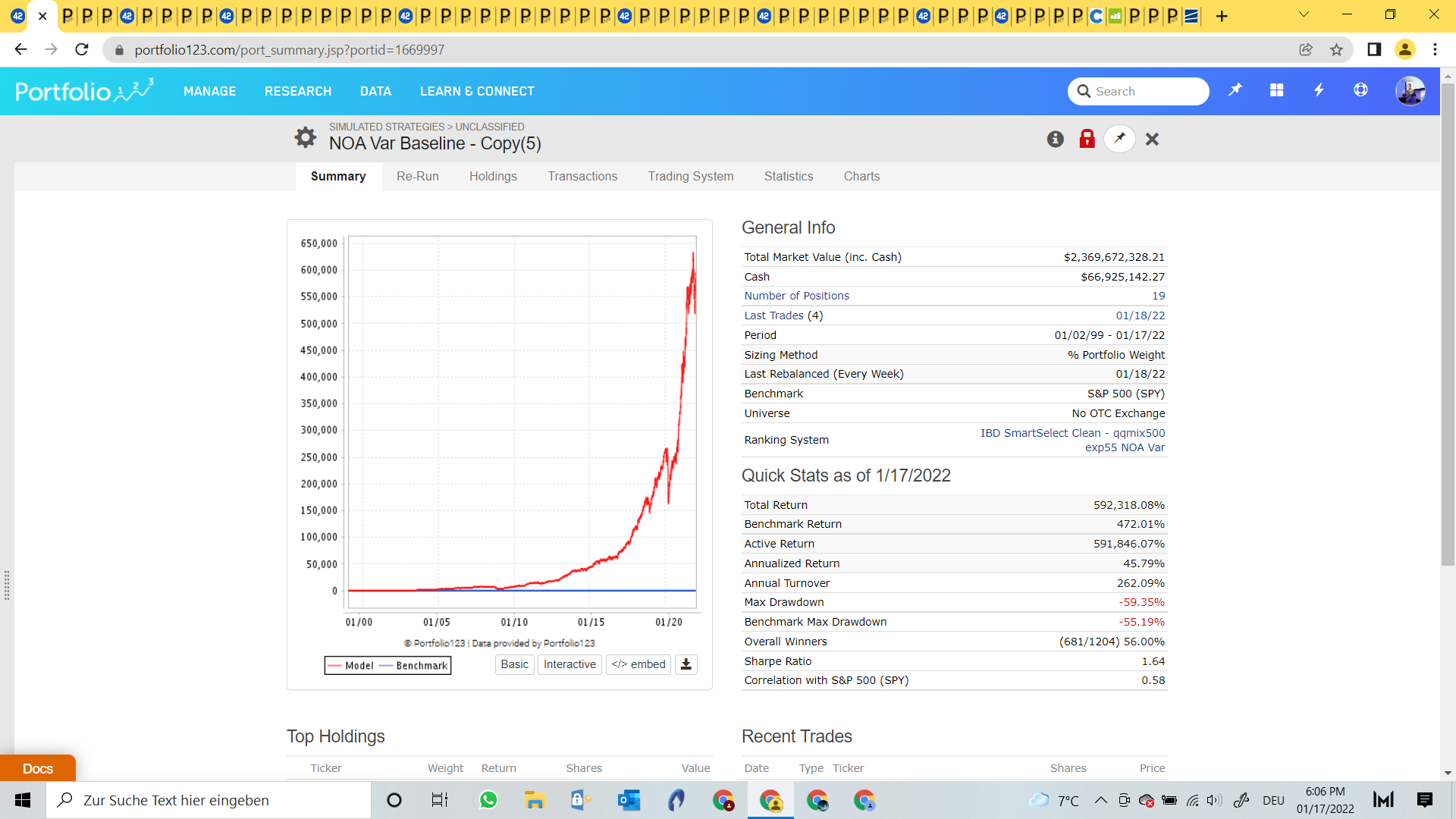

All good points. I had some of your same thoughts. It is actually a strategy with pretty high turnover. I took some action on your idea of overfitting The “until it doesn’t” period starts 11/14/2018 (until now).

I used factor analysis to reduce the overfitting. The resulting less-overfit SIM is imaged below. Same period and I checked to make sure it was variable slippage with average of hi-lo purchases/sales.

One problem I am having as far as committing any money to this sim is that ports (exact same rules, universe etc) run over the same period are very different.

By that I mean different holdings, different rankings for the holdings when bought and sold and different returns with the port (anecdotally) underperforming the sim.

People (including me) can speculate or guess what that discrepancy might mean but I do not think anyone really knows for sure (this applies to me).

I am left with the idea that a little beta might not hurt and any speculations that there is still some alpha there may be entirety correct.

Regret can go both ways (first): " Gosh I lost a lot of money on that." But also (second): “I wish I had just funded that sim and figured out why the port had different holdings later. I could have been super-rich.”

I think I will fund it as a beta strategy and fund it to a greater extent later if it turns out to be a strategy with alpha.

In other words, I agree with you (and Matthias) completely. Thank you.

Looking at the cap curve I would not trade that model. → See performance from 2015!

What I think is realistic: If the market is up (lets say IWM), the book needs to be up more then the market, if the market is down, your book needs to be roughly as down as the market (but not more!).

So at the end of the day its higher beta, that does not get destroyed in a risk event.

I want to see models that track the performance of the indexes and yes which correlate.

I know that a lot of system traders try to do otherwise, e.g. built models that do not correlate.

At least in the stock market I think that is a bad idea.

Stuff like that (OOS since Summer 2019):

Multifactor Ranking System

1 Buy Rule (picks stocks with low volumne that are still tradeable for a sub 2 Mil account)

1 Sell Rule (Rank)

For the record, I was not recommending my sim/port to anyone either. I’m not using it myself. My post was about risk and the sim was just an example meant to show that models can stop working. But since you are a professional, selling some of your models and advertising this model as being representative, I wonder if I might ask about it and comment since you have posted it.

[color=firebrick]I will take notice of your sims when you show us all of your Designer Models including the ones you have removed (no survivorship bias). These are some of the best models you have produced and you recommended (sold) them at one time, right?[/color]

BTW, your sim is from 1999. What you did with real money since 1999 would be as good as all of your Designer Models without survivorship bias if you cannot find them. [color=firebrick]That would also be some quality evidence.[/color] It speaks to what you really would do with limited knowledge-like the real world. Not a fantasy world where you can cherry-pick any sim/port and imagine what would have happened if you were fully invested.

On the topic of this thread, I know you have learned something about risk over the years as you had an 84% (or greater) drawdown that put you out of the market for several years (before P123)? Correct me if I am wrong and please expand further on the general topic of risk. You should be an expert on what can happen with too much risk.

Good thread for your post. Thank you. Please expand and let us learn more about risk from your experience.

I don’t use high turnover portfolios in my taxable account. As far as trading costs go if the security is liquid enough relative to your position size it should be minimal.

I trade in a SEP-IRA so tax issues are not a concern of mine and I do not understand that very well.

What one does with regard to trading costs can depend on what one thinks about P123’s variable slippage.

The liquidity on the above sims (and the universe) is actually very high and I think P123 overestimates the trading cost for my sims. Meaning my slippage is probably a lot lower for market orders. I don’t have any experience to offer on some of the lower liquidity universes used in some portfolios.

While I worry about the accuracy of the sim, regression to the mean out-of-sample etc., slippage is not one of my concerns.

This is why I compare my entire account with a realistic benchmark (what most non active investors do) which are the ETFs: aor, aom, and aoa which returned 10.7, 6.8 and 14.7 % respectively in 2021 (and if they had an advisor their fees would be reduced by that amount). A 60/40 US stocks/bonds would have returned 15.8 % but that is a less realistic portfolio for most investors as they have an international component.

So, I would say of the ETFs you mentioned AOA might be an appropriate benchmark for me as I do hold bonds or rather leveraged bond futures. And it is probably fair to use the adjective “aggressive” as in the phrase “aggressive bond fund” to describe my portfolio. I say this because of the leverage if nothing else.

I did beat AOA (iShares Core Aggressive Allocation ETF) last year as well as Fidelity’s benchmark: "Index Blend 85% Stocks "

Obviously, I do not understand much about your portfolio but is sounds like we might be on the same page or at least in the same ballpark.