Both outperform the market by a wide margin, but they are also cap-weighted. How is it possible to determine whether it is the Fool-100, or Founder-led companies, that drive the return, or if it is simply because a majority of the companies are large cap, and hence benefit from the broader momentum in the S & P500? ( Large Cap)?

Or how to determine how much of the return is attributable to alpha and how much is due to market and cap weighting?

Both ETFs outperformed QQQ–BOSS by a lot, and Fool-100 by a little–and would have done a lot better had they used equal weightings.

However, I using most recent holdings of their respective ETFs so there is a strong risk of look ahead bias. Indeed, the most recent two years saw under-performance from both vs QQQ.

Is there a way to use historical holdings? I know that there was some talk about that.

[quote]

However, I am using most recent holdings of their respective ETFs so there is a strong risk of look ahead bias.

[/quote]Using the most recent holdings from an ETF for backtesting is a NO-NO. This will give survivorship biased returns.

Each ETF is required by US regulations to file quarterly holdings with the SEC. The SEC form is called NPORT-P. I assume that with a little more work I should be able to automate the process of downloading these forms.

This link works better than mine. Remember the dates are actual filing dates. Point-in-time for us is 2 months later. So the list of 10/31/2021 would be PIT as of 12/31/2021.

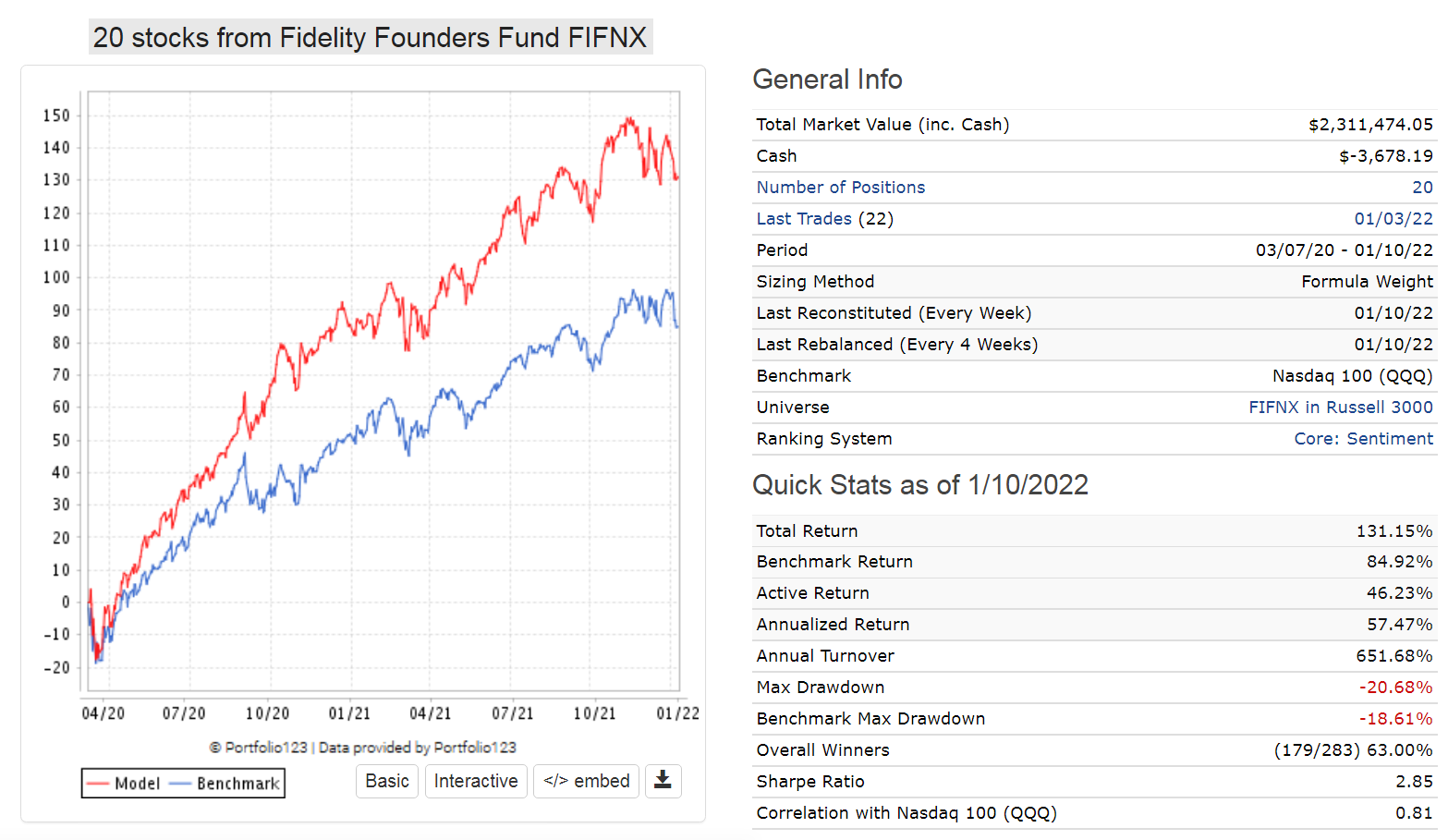

Here is the performance over the same period of 20 stocks from Fidelity Founders Fund FIFNX with P123 Core Sentiment ranking system.

Much better performance.