I stipulate that there are some people better at investing than others. And that some people have nothing to worry about long-term. Also if I did not believe in what P123 was doing I wouldn’t be here. I use P123 and have made money with P123. But less so as I near retirement.

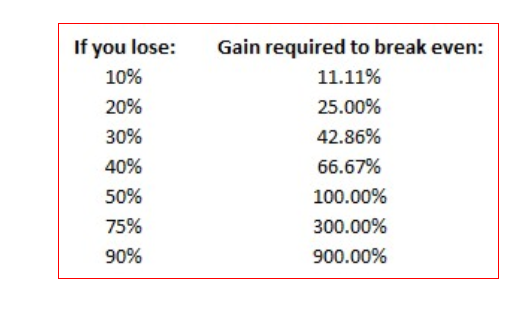

A smart person at P123 pointed out that after a 50% decline, one has to double-up to get back to where they were. I think Marco may have made a similar comment, if I am not mistaken. I paraphrase and Marco can correct me or share his present beliefs if that is not correct math. I think it is just a fact no matter who said it.

Even holding QQQ has caused severe declines that took over a decade (closer to two decades with inflation adjustment) to get back from in the dot.com bubble.

One can look at the designer models to see that being down 75% is about as likely as being up 75% for the average member.

One has to double-up and double-up again to get back to even after a 75% decline.

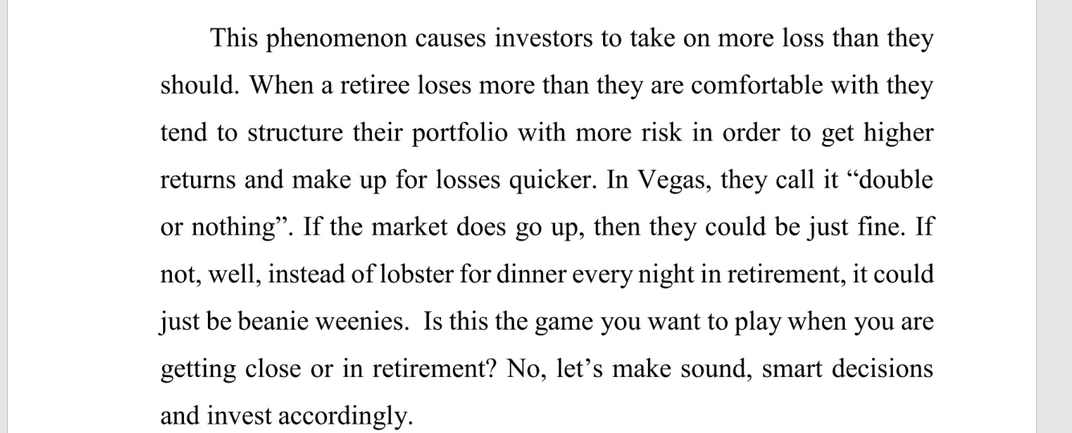

I wonder if Hem or Rikki could begin a reasonable discussion of risk control for the average member. There are a limited number of gambling addicts that P123 could hope to attract. Or expect to last long at P123 with that type of volatility.

I think you have made a very important point here (risk control).

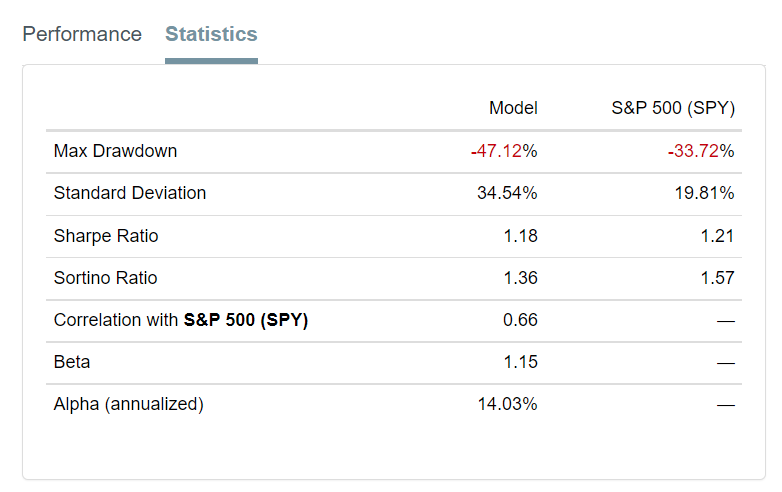

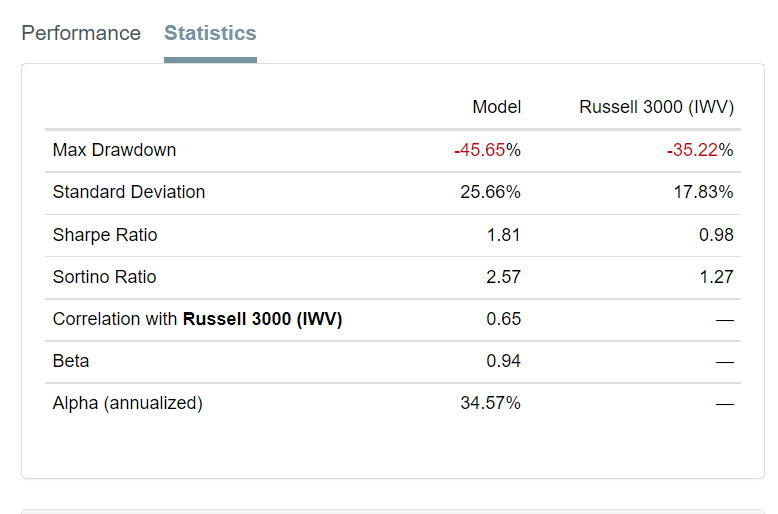

Out of curiosity, I make a quick check on the designer model database. Below are two examples with an almost 50% drawdown despite a relatively short (2-3 years) since the launch of the model. (i.e. you may lose up to half of your capital within 3 years).

The P123 model “Small Cap Quality” by Yuval was down 50% and came roaring back.

Is Risk Control another phrase for Market Timing? I gave up on both

I’m fully invested now and trying to be more and more systematic (still doing too many emotional decisions bc I love tech). I use a bit of leverage too since money is cheap.

I stipulated that some have no worries and I have no problem with looking at those cherry-picked models.

But some are down 50% or more and will never recover here at P123 if they did not get out of their models. We can see some of those models. Designers–and probably P123 members in general --underperform their benchmark. Many dramatically so over long periods. They could use something–if not risk control.

A few should be encouraged to join gambler’s anonymous: not encouraged to try the same thing again.

Let me just say that I think what Zacks does as far as rotating cherry-picked models that happened to have done well recently to advertise is probably not illegal. I question the ethics of Zacks’ advertising, however.

For sure Zacks site for retail investors does not look very professional. I don’t think it attracts many true professionals. Zacks has other offerings for that.

I think Hem and Rikki probably studied risk control in school if they want to share.

I wonder what specific ideas Chris (ETFOptimize) or other professionals are recommending as far as ETF strategies to reduce overall risk in their client’s portfolios. I assume some of his ETF strategies can be mixed with ports.

I think you need to have a hypothesis (Macro view) of what will work in the future. It will only be 51% correct. Let us not forget that professional money managers over a 10 year period have a 5% chance of beating SPY. Which means designer models have the same and it looks that way. If I put everything I had in QQQ in 1999 versus 2009 the payoff is drastically different. If I used risk parity in 1999 I am brilliant. Timing is everything but no one can tell you when. So what do you do? You create a highly diversified portfolio of uncorrelated assets that are acceptable to your risk tolerance (Volatility/age). Or you concentrate based on your macro view. I do both. I concentrated on tech last year did well. Used options to protective myself. It cost me half of my returns to hedge. Everything I read this year is that it’s 2018 all over again so I will probably lose 20%. Does that mean I have given up on tech no. The world is all about tech but I cannot predict when the big 8 will climb. I just manage my losses and suck it up. My uncorrelated asset portfolio has a everything I’m targeting 12% returns with 10% vol. It did really well in 2018. Will let you know how 2022 goes. P123 is very different than what I do but I love the community and thank you.