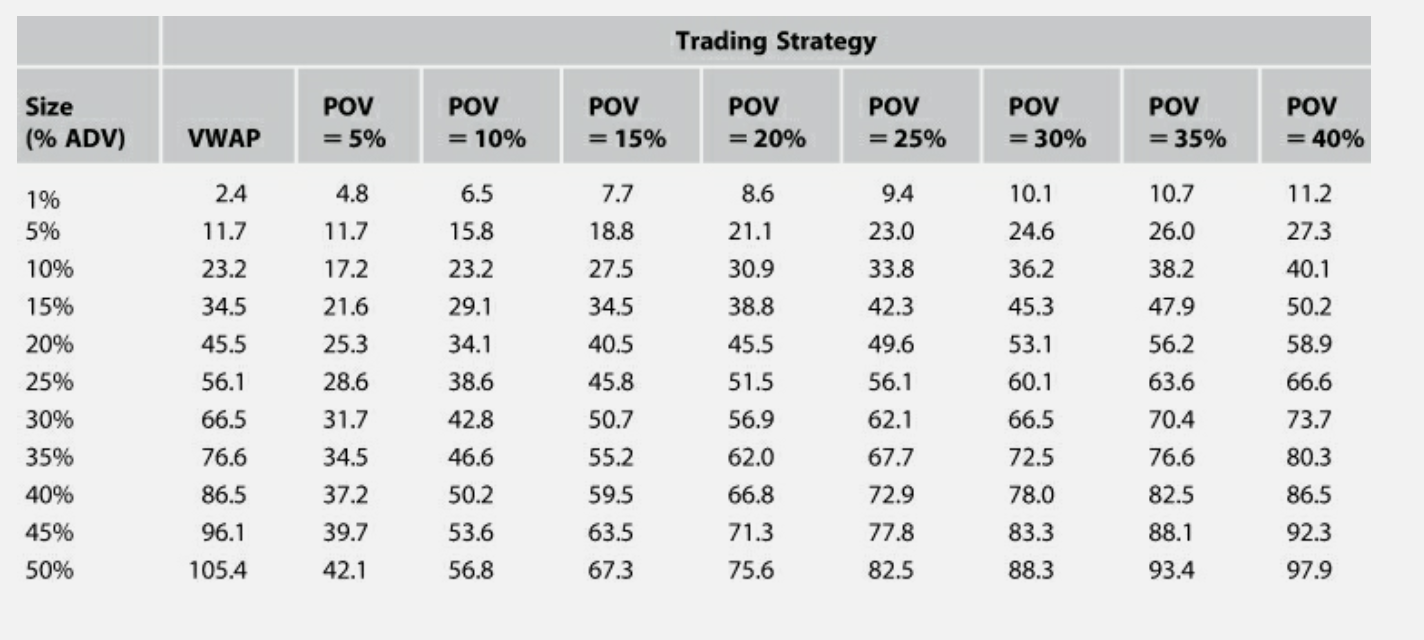

So, keep in mind my portfolio size is literally 17,000USD - but yea I only speculate in shares between 250 & 5000$ in the past 20 days on average. Some of them go inactive and in general I have to set out 4 orders for every one that fills, but the strategy gave me 100% for January. After January, I went on to gravitate to higher volume stocks because I thought the partial fills weren’t worth the fees, which I believe was a mistake for my speculative strat.

It could be worth the money to double your average fee’s and get an extra few percent on the backtested return side, I really don’t know anything about trading positions succesfully in large scale volumes and am really only guessing for lower volumes. I would imagine that if your strategy calls for weekly or biweekly reballancing, it would make sense to buy your small stocks over the course of a few days, basically just reballancing on different days so you dont flood the market with buying or selling.

Also, I noticed that higher volume and an increase in price actually predicts worse speculative returns, so it’s a mistake according to backtesting to buy (as a general example):

AvgDailyTot(20) > (1 + (5/100) ) * SMA(50) // Volume is 5% above 50 day SMA

Close(0) > (1 + (5/100) ) * SMA(50) // price is 5% above 50 day SMA

AvgDailyTot(200)>20000

No OTC, 0.% Slippage, Reballanced weekly at open does 11%.

But, for example buying the inverse has done 23% in the past 5 years.

Close(0) < (1 + (5/100) ) * SMA(50) // price is 5% below 50 day SMA

These results are subject to quite a high increase in the past year or so. It would be worth knowing how the above have done in the past 20 years but they form the basis for my current speculative theory!

I think the reason median does worse than average is because average allows you to look at stocks with lower volumes and the median will in general force you to buy higher volumes, so on the whole I think you’re probably right about the stability of median over average, but it might cause you to be in general buying positions in a market that are occasionally more liquid than you need them to be

There’s a reason my portfolio is only 17,000$ though, so take that with quite a bit of salt!

James

PS my typical position sizes are 250-700usd I pay 10$ per trade and it was 97% after fees for January. 130% prior to fees, so it was absolutely worth it for me to pay the fees on the impartial fills that I thought were hurting my returns. I went to 1,000$ positions around mid february to avoid the fees and actually have been going flat while my backtests have been doing much better than I. I suspect it’s because all my fills would only be in the very active stocks, which have also been flat since February.