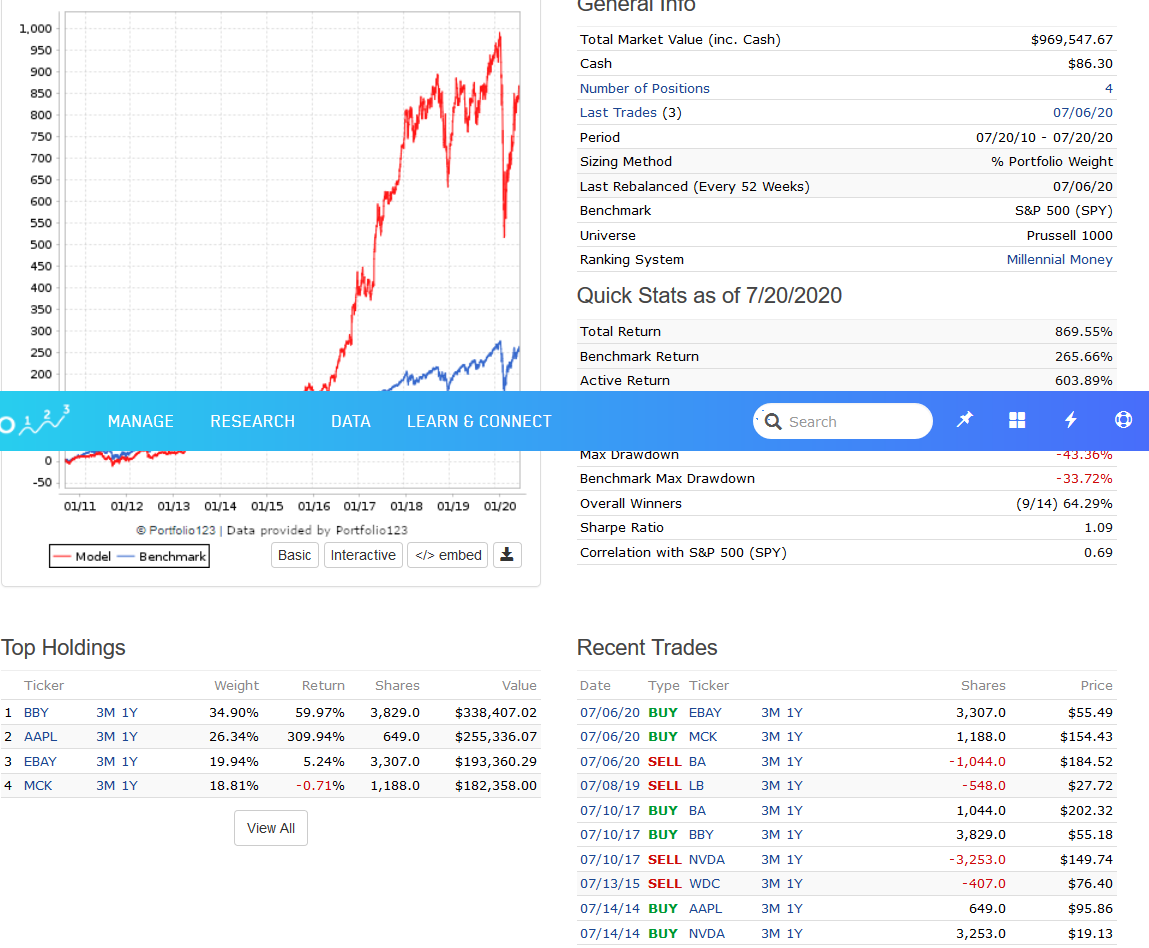

Hey guys,

This is my first post on here. So don’t hesitate to let me know if you need any additional info. I used the simulation tools, and I got the result in the attached pic. The strategy uses only a few holdings of very high quality companies. While the overall return is great, the max draw-down for the simulation is much worse than for the S&P 500. Is there any way I can sell when the portfolio dips 15% immediately? I’m not exactly sure how to do this because the simulation re-balances annually. I would like to keep it this way because this re-balancing frequency works best for this simulation. I would also appreciate any other suggestions for how I may be able to reduce the draw-downs. Thanks.