I have been at this a long time now, and I am beginning to wonder if creating ports vs. using ETFs and funds is worth it. My basic approach has evolved to 50 stock Mid Cap ports with no more than 20% sector allocation. I feel that small and micro stocks are just too volatile and open to manipulation. I also feel that if a 50 stock version of a strategy doesn’t out perform a 10 stock version that does, is not robust, but lucky. P123 has published some solid ranking systems and many seemingly intelligently constructed combinations. Applying these, however, rarely leads to significant outperformance, which if it does is eaten up in fees and taxes from short term trading. There are countless factors and custom combinations, of which I have found 99% to be worthless in generating alpha, when controlling for sector or size bets. I am left looking at the data, which I have beaten to death and seeing no real alpha to be had in the large and midcap space, and unpredictable and unreliable performance in the small and micro space. Just throwing my experience out there.

Here is a good stock picking strategy which should provide a 20% annualized return:

- Select large-cap stocks from PRussell 1000 universe only.

- Select stocks that have a higher dividend yield than SPY.

- Specify the required excess yield over SPY for each FactSet sector. (TECH has low excess.)

- Use a simple ranking system.

- Trade only once a month.

- No market timing

Just posted detail description.

Anybody can replicate this on P123 with little effort.

A Dividend Growth Strategy for Perennial Income

https://imarketsignals.com/2020/a-dividend-growth-strategy-for-perennial-income/

Dividend yield is great in normal times, but I have doubts about high(er) yield stocks in this microenvironment. The coming quarterly results are going to be devastating and yields will likely be slashed. That’s my 2 cents anyway.

Steve

Steve, if stock yields are slashed then yield of S&P500 will also be slashed. Since my model is based on excess return over SPY it will still pick the better stocks.

Georg,

The backtest looks great with 10 stocks. What about 50? In a taxable account the dividends will be taxed at regular income, and short term gains are almost punitively taxed, which brings you back to no better than an ETF just held.

Charles,

I gave up stock picking long time ago. ETF only I use dynamic allocation each month but just buy and hold and adjust quarterly works. You can easily run the following 3 ETF in a book and see the results. If you are brave you can use the leverage versions for better returns much higher volatility and drawdown. For a permanent portfolio I would use 60% QQQ, 30% TLT and 10% Gold. The dynamic model adjusts the percentages and gives you much better returns. Your timeframe is always important to consider if you need the money in five years you might want to change the percentages. The question I ask is what are the odds that all 3 of these ETF will have a negative return over the next 5 years? I have been asking that question for the last 10 years and I am always getting it wrong. Wrong because every time the market tanks I sell bad move. I missed lots of upside. Good luck.

5 year returns:

QQQ 20%

GLD 9%

TLT 10%

Combined ~ 15%

Cheers,

MV

I’ve been using the tools here for 6 years and have found a method that consistently outperforms the market. I’ve found that stocks in the $2.5B to $15B market cap range provide plenty of opportunity but don’t have the volatility that the small cap stocks have and they are very easy to trade. I rely mostly on buy rules to identify stocks that have good fundamentals. I haven’t found technical factors to be good predictors of outperformance. The models I create select stocks with ranges for each variable. To do this I first identified cutoff values to create 10 deciles for each variable. The FRANK(variable) will get you most of the way there. You then test each variable to determine how each decile performs both overall and over time. I mostly look at performance relative to the market because my goal is to beat the market. After testing each variable you can then combine the best deciles from each variable and keep testing until you get something that has consistent outperformance over time. It’s a lot of work but since I started using this approach almost 2.5 years ago my annualized return is 36.0% on a 50 stock portfolio. These 50 stocks are rebalanced every three weeks with about 9 stocks being bought and sold so it’s relatively low turnover. I graph my return against the benchmark and calculate the ratio of the two which is the excess return. I create graphs for each decile for each variable too. This excess return has continue to grow even through the Covid crisis. The only time period that it flattened for a few months was last Fall. I’m an actuary and spent my career doing predictive modeling so I have experience with volatile data which the stock market is. The most important thing is to not overfit your models. Combining several factors will get you the outperformance you are looking for. Adding more will just add noise from what I’ve seen. The last piece of advice is to rely more on what works in the last several years. What works in the market changes over time. I expect that someday my models will need to change because the variables are found by others. I’m continually tracking each variable to identify if they are changing. I don’t know of a way of anticipating these changes though.

Charles, a 50 position model and holding period > 365 days shows an annualized return of 13.8%.

Avg 10 yr dividend yield = 3.80%.

Starting Capital 1/1/2000 = 100,000

Tot Dividend 2000-2019 = 434,202

Tot Withdrawal 2000-2019 = 0

Portfolio Value 1/1/2020 = 1,592,998

So this looks viable in a taxable account.

Charles,

I believe Mark is very sophisticated on risk, MPT etc.

Anyway, I think Mark is probably right that adding individual stocks to a diversified portfolio of ETFs will not increase the risk adjusted returns very much.

A young person with a longer investment horizon may get higher returns and be compensated for the increased risk of holding individual stocks. Classic risk metrics mean less in this situation (as Warren Buffett has been quoted as saying).

But even if one decides to invest in individual stocks, keeping a portion of your holdings in a dynamic allocation model—as Mark suggests—might be worth considering.

Best,

Jim

Charles -

My personal experience is similar to Erik’s: I have a CAGR of 32% since 1/1/2016, and I’ve put a tremendous amount of work into it. Unlike Erik, I invest mainly in microcaps and small caps and trade every day (possibly to my detriment). I personally find stock-picking immensely rewarding. If I were you I would weigh not only how much money you’re making but how much fun you’re having in the process.

- Yuval

Charles, I had a very similar experience to you about 2 years ago.

Nearly all of the live models I had been using previously with some success started bleeding money. Seemed all of my sims were broken as well. I took a break entirely, and re-booted. Took a deep dive into the P123 forums to learn from those users/investors most similar to my investing personality. I was out of the market nearly all of 2019, working on new models, testing, re-testing, researching.

I only just put my ports to use early this year, but even through these volatile times my live ports are all outperforming their benchmarks (US and Canada).

Quant investing can at times be marketed as “passive”, but I would agree with Erik and Yuval, it does take a lot of work, tweaking, researching, adapting to new market conditions, etc.

My tips, for what they’re worth:

- Micro and smallcaps all the way

- If you use some decent factors, you can minimize the volatility as you’re concerned about

- 20-25 stocks per port

- Limiting sector allocation can be a double-edged sword. I give a decent weighting to industry weighting in my systems, it’s never a bad thing to take advantage of those tailwinds.

- Quants are conditioned to look at returns over the longest time horizon, i.e. “these factors have outperformed over long periods of time”, but in my experience, any backtest that includes the “quant paradise” of the early/mid 2000s will be heavily skewed and give a false sense of out of sample CAGR going forward in 2020. Like Erik and Yuval (and Steve has mentioned many times), weighting more recent periods in backtests can be more effective.

- I would avoid some of the classic factors (P/E, P/B, etc) as the main components of your ranking systems/sims. Secondary factors yes, but there are newer innovative factors that have much more potential for alpha.

- The actual trading/execution is an underestimated part of the whole process IMO, especially for high turnover/weekly rebalance ports. You can lose a lot to slippage (much more than the sims assume) without say limit orders, and knowing when to give up on a stock that runs away from you. This is still relatively new to me, but I keep practicing. Win some and lose some, but at times I can now achieve less slippage than the sims assume.

- You mention taxes, I believe most of these strategies (weekly rebalance and high turnover) are best in non-taxable accounts.

Good luck, feel free to reach out.

Cheers,

Ryan

Over time, I’ve phased out selection of individual stocks, and focused more on asset allocation plus leverage. Here is a video from Ben Felix that helped convince me that leveraging a broad portfolio is more suitable for me to increase risk and reward, instead of stock selection which by definition narrows your portfolio:

https://www.youtube.com/watch?v=Ll3TCEz4g1k

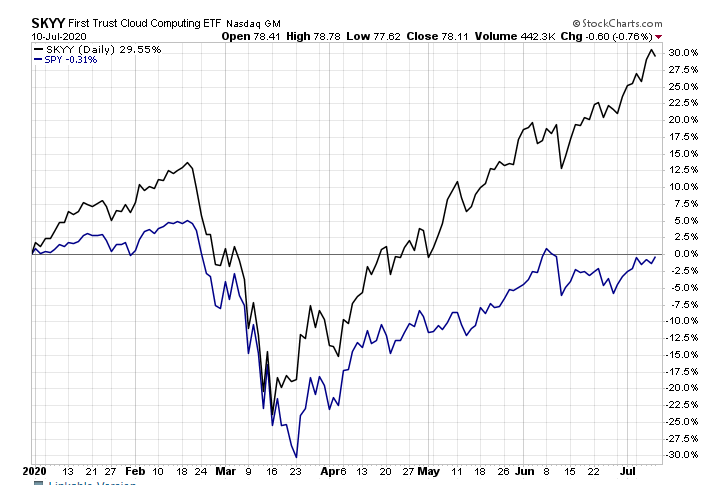

For leverage, I use leveraged ETF’s like TQQQ (3x QQQ), UPRO (3x SP500), TMF (3x treasuries). There are no margin calls, and they are unlikely to go to zero due to circuit breakers. Even if they go to zero, that means the un-leveraged version went down 33% in one day, which means all confidence is gone and they’ll probably go to zero the next day anyways (SHTF). Generally, stocks go up over time, and leverage just means you get there faster. Even though I like something like SKYY (cloud computing), I think it is too narrow, and thus more likely to fall out of favor, and I prefer TQQQ because it is more broad and therefore more robust over time.

I personally have a bucket of money that is 50% TQQQ and 50% GBTC, rebalanced regularly. GBTC is greyscale bitcoin trust, which unfortunately P123 does not allow in models.

I have another bucket of money that is TQQQ, UPRO, TMF, GBTC, NTSX (90/60 stocks/bonds, which is 60/40 leveraged 1.5x). I don’t re-balance this one, and just contribute to what I’m bullish on.

Here’s my 50/50 TQQQ/TMF model:

https://www.portfolio123.com/app/r2g/summary?id=1596865

50/50 UPRO/TMF model:

https://www.portfolio123.com/app/r2g/summary?id=1602218

I really wish P123 will add GBTC. Bitcoin was the best performing asset of the decade. It will likely be the best performing asset of the next decade. It is more scarce than gold. It has superior stock-to-flow ratio vs gold. Every 4 years, the supply of new bitcoin gets cut in half. Imagine if the supply of new gold, or new real estate, or any other commodity, got cut in half every X years. If nothing else, it’s an excellent hedge against inflation and money printing (it has a capped supply) and has low/negative correlation with your other assets.

I do 20 stock picks for yearly competition with a liquid stocks.

I feel stock picking is worth it. it will take passion, knowledge, focus, discipline, believe and faith to become successful in stock picking.

It took me 2017, 2018, 2019 & 2020 experiences.

The important thing is keep journal; why your stock picks failed; why it become successful; how to improve every year.

It is exciting and fun if you are successful; It is observing time and learning tons of lessons if you failed.

Either way i am good; either earning money & happy or learning lessons & happy.

people are spending lot of money to get admission in business school to learn from university;

the market is like university; any one can learn gradually to become successful;

Thanks,

Kumar ![]()

MisterChang - excellent video! Thanks for sharing.

This is false logic for a couple of reasons. One is that not all S&P 500 stocks pay dividends. Second is that the S&P 500 is not something that one should aspire to outperform in today’s markets. The index really hasn’t recovered from the February bear. And the situation could get worse from here as the “V-shape” recovery doesn’t happen.

Steve

charles123,

with help of p123 forum competition, i able to cultivate 20 stock picking performance better than SKYY cloud computing ETFs.

I build believe and faith on my stock picking strategies over last 4 years. I believe it is worth it if you get right education, passion to learn year by year

as i did. It is a investment journey with hard work; no shortcuts as it involves money to invest one should have undivided focus and passion to learn.

Mgerstein, Steve, Yuval, who are inspiration to me believe in fundamentals. without fundamentals; my model can’t hold 1 year performance.

Mgerstein - Value fundamental investor; he review my value model 4 years ago; i learned importance of fundamental from him.

Steve - Very long term P123 experts, counless forum messages; discarded many designer model if not performing well (indirectly admitting his mistakes).

was stockmarketstudent for many years; finally become sector inspector, never give-up attitude when come to learn to become successful in investing.

Yuval - Go out of the box from P123’s computer designer model; brought idea of yearly competing vs benchmark performance from wallstreet crossing website;

he proved for last 4 years. many individual 20 stocks pick can beat the market.

his last year finding was bloomberg 20 stocks for year 2020, i have included in the year 2020 competition, it is performing 2nd for this year competition.

I would like to learn from yuval, some more new sources for quarterly stock picking. So, we will have one more competition for quarterly.

Some more knowledge; for focus on quarterly stock picking. I believe, he will help us by researching in his fair time.

My growth as 1 year investor direct result of Yuval p123 20 stock pick competitions. I able to stay focus for 1 year holdings; not for a daily or weekly or monthly holdings.

I am very thankful to Yuval.

=======================

Thanks,

Kumar ![]()

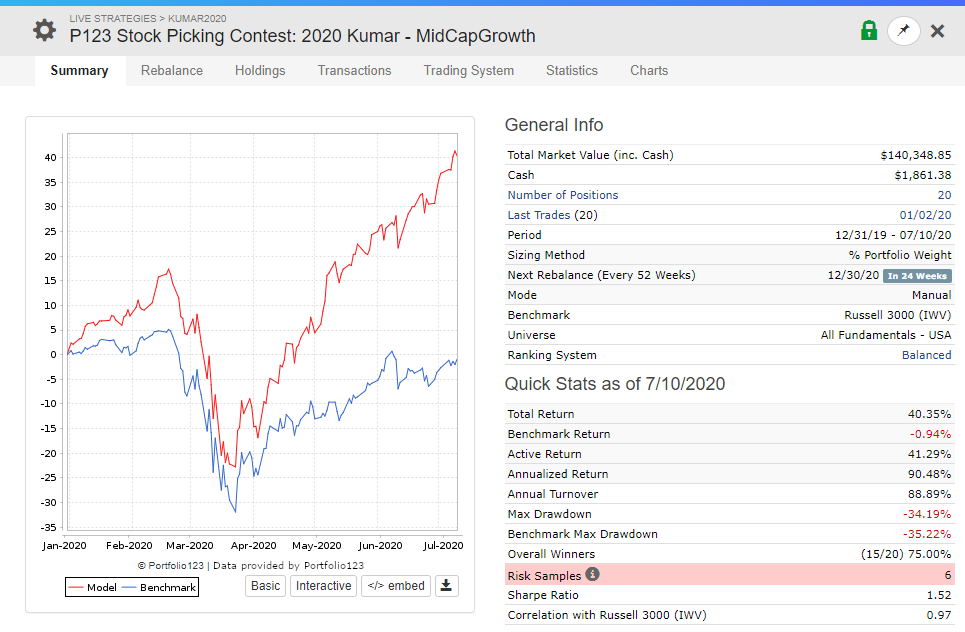

Thanks all for your thoughts. I was particularly interested in this post by Aebouvin. A 36% CAGR on a 50 midcap stock portfolio over the last 2.5years is nothing short of astounding! A few questions:

- Is this one 50 stock portfolio or a combination of smaller ones.

- If the goal is to look for factors that have beaten the market recently (1 year, 2 years, etc.), why bother looking for the factors that contributed to this out performance? Why not just invest in the best returning stocks recently (i.e momentum), as I assume it’s likely that the best performing stocks recently, will have fairly consistent similar factors.

- Would you care to post a screenshot of your portfolio performance? I am interested in the equity curve shape.

Please only share what you are comfortable with. Thanks all

Over the years I have flip-flopped between chasing stocks and ETFs. I now perceive there to be as many issues with ETFs as with stock picking, including flash-crashes and inability to get exactly the product (market niche) that I want. So I currently am back to stock picking. But tomorrow is a new day. Perhaps I’ll flip.

Kumar - Designer Models are a business for me. I don’t keep models based on how well they perform but subscriber interest. If they aren’t making money they get cut. The Cloud Computing model is outperforming every other DM by 40+% over the last year, yet I am breaking even on it. Up until recently I was losing money on it and have thought about cutting it. (I would take care of existing subscribers if I did that).

So don’t read too much into disappearing models. The bigger issue is that the markets, P123 platform, and subscriber tastes are constantly changing. Investors need to adapt to market conditions if they want to thrive. And the Design Model premise is that a portfolio is good forever which is really not the case.

Erik,

I really like what you are doing. One of the many things I like is that you are effectively testing each factor for statistical significance before you add it to the ranking system.

This should help prevent overfitting.

This seems to be a recognition that the optimization procedure itself can also be a source of overfitting. I believe this is true even if each factor is statistically significant on its own.

As you know (as an actuary) multicollinearity can make the optimization difficult and potentially cause problems with overfitting. Arguably multicollinearity does not reduce the predictive performance of a regression model. But we are not talking about a regression model with P123. We are talking about an optimization method that is prone to overfitting. And also–with the stock market–the correlation of the factors can change. Any statements about regressive predictive models assumes an i.i.d. sample as you know. It also assumes the the sample on which you are making predictions is drawn from the same population.

I assert (without a proof here) that you are exactly right. That one can cause overfitting at P123 when optimizing a bunch of factors—especially if the factors are correlated. I agree that this is true even if each factor is significant by itself.

So here is my question. Have you tried principle component analysis to mitigate the problems of mulicollinearity and overfitting?

The factors in each principle component can be placed into their own node at P123 (with the weights you get from your PCA analysis “factor loadings”). Then the nodes will be orthogonal and can be optimized without the multicollinearity problems.

I am assuming that–with your profession–you have some tools to look into this if it interests you.

In any case, thank you for sharing.

Best,

Jim

[edited: error]