One of William O’Neil’s sell rules in his CANSLIM system (as outlined in his book “How to Make Money in Stocks”) is a 7-8% stop loss rule from your entry point. He is adamant in his book that there are no exceptions, i.e. ALWAYS sell if your position if drops 7-8% from entry.

For those who are not familiar, CANSLIM is a growth oriented strategy. For more value oriented investors, a drop in price usually means to buy more of stock. As a growth investor, O’Neil disagrees with this strategy of averaging down.

BTW, for those new to P123 there are some “off the shelf” CANSLIM/O’Neil ranking systems and screens under the P123 ranks/screens.

Curious, I’ve tested the entry stop loss at several thresholds.

Last month Andreas was gracious enough to share the concepts of his latest trading system. I’ve made my own system which is similar, and is also similar to the concepts outlined in CANSLIM.

FYI this is a small/micro/low volume strategy. CANSLIM was originally intended for larger issues. However the sim results with and without stoploss are impressive.

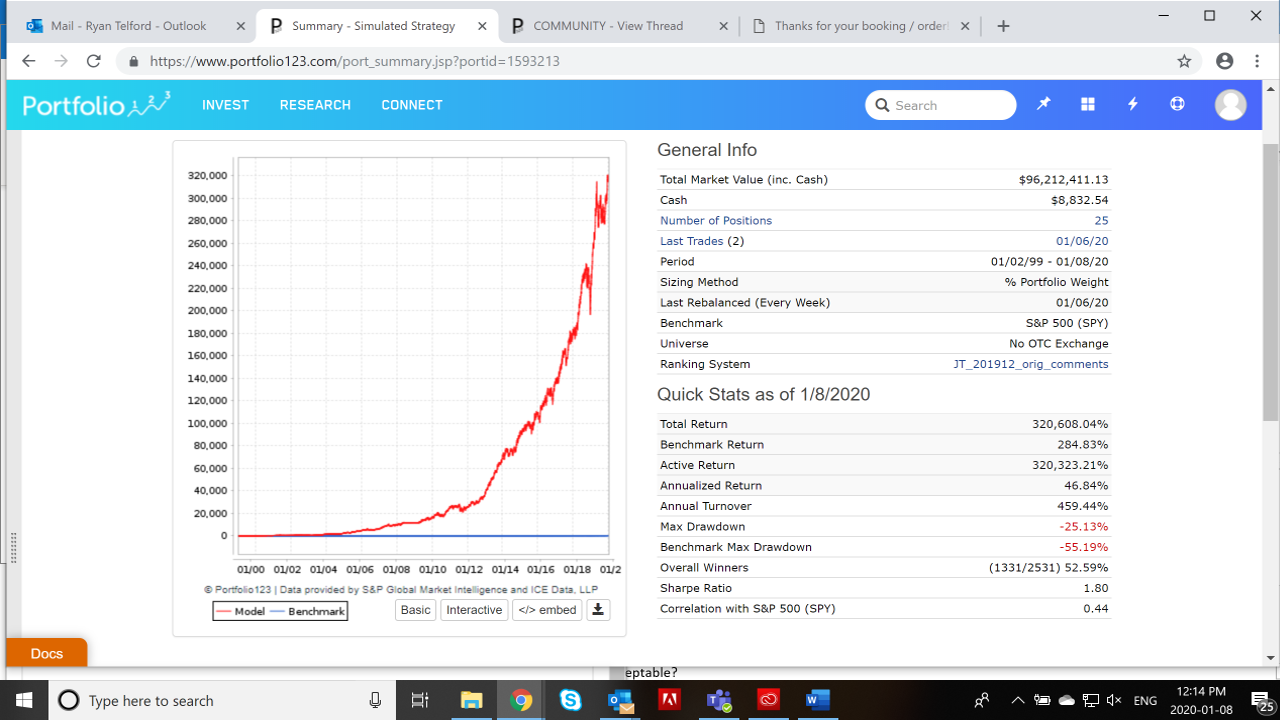

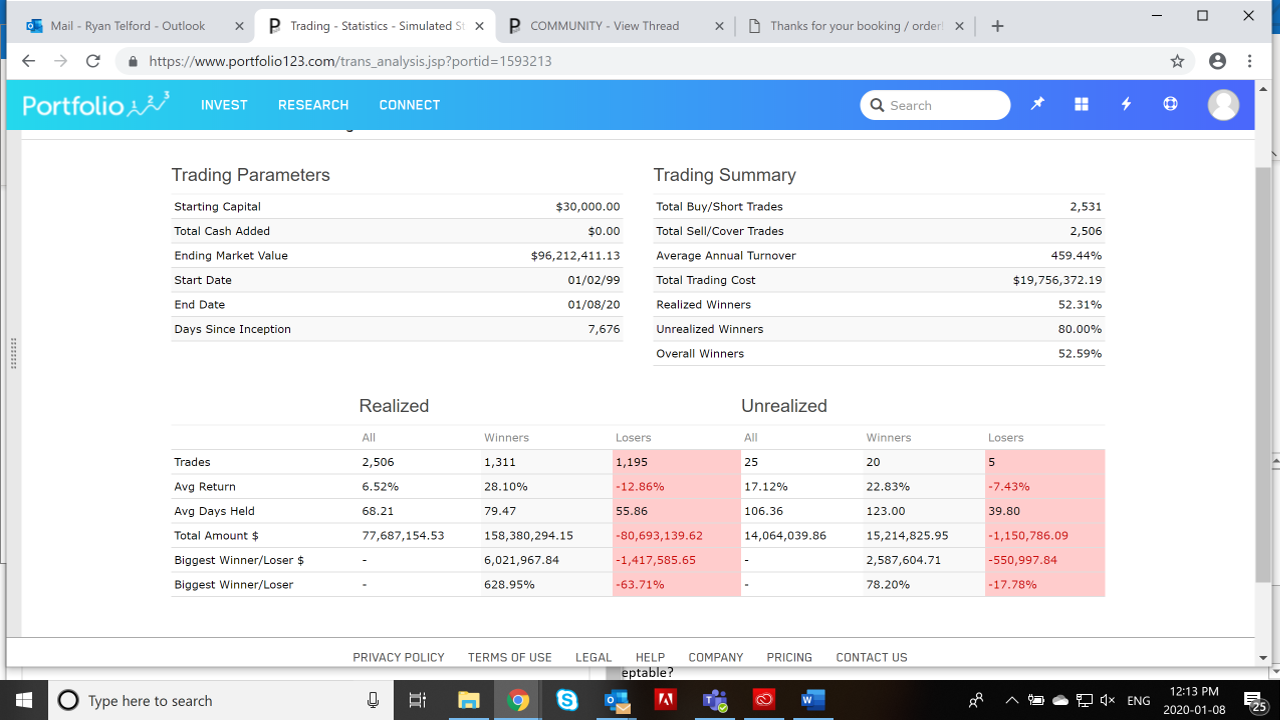

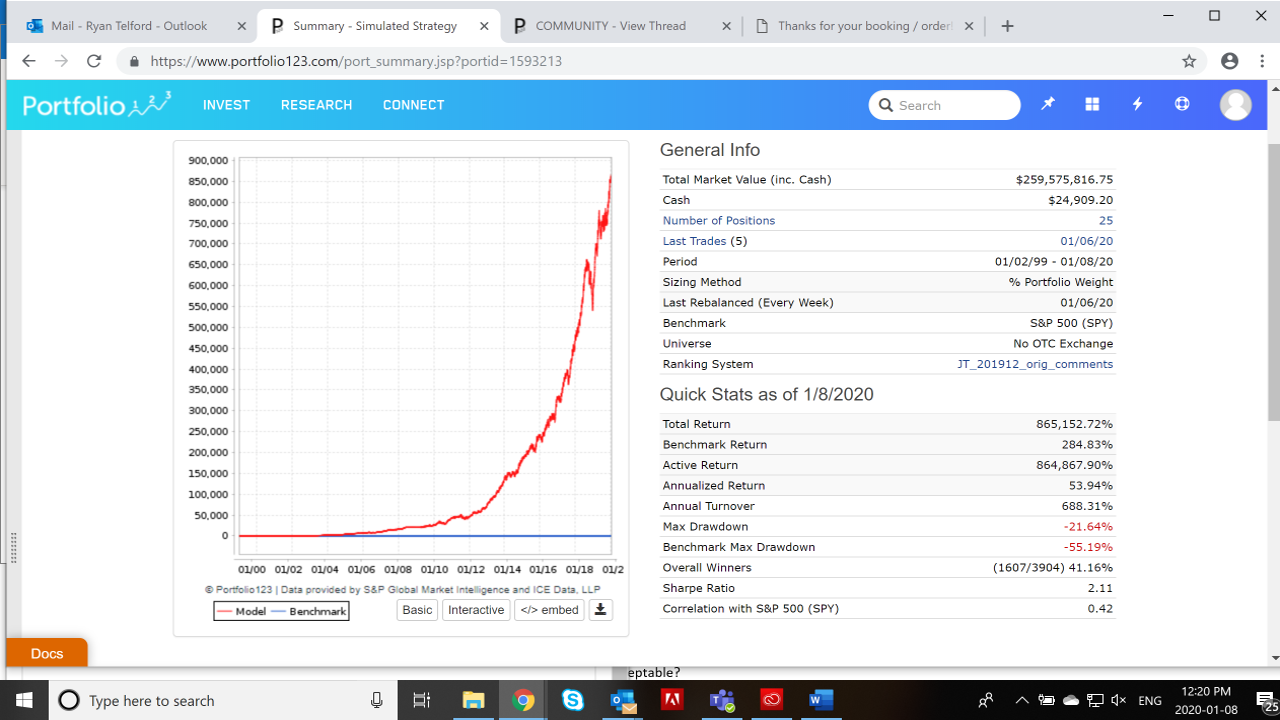

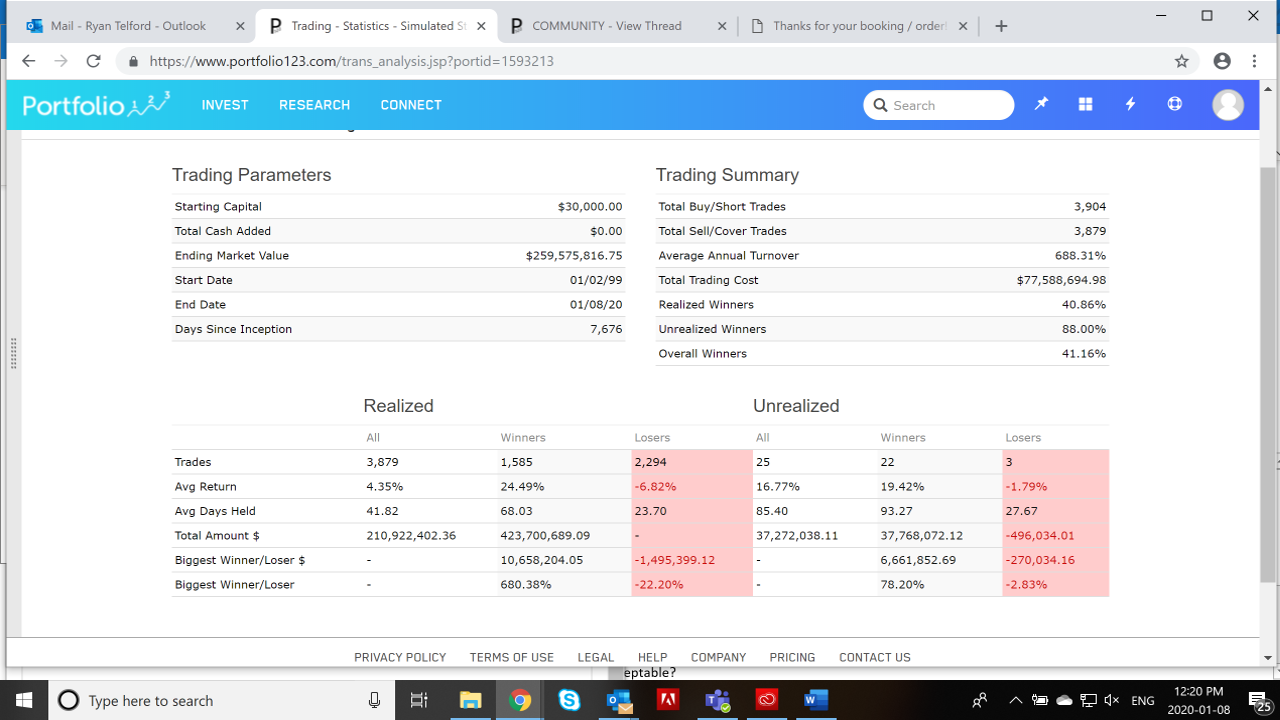

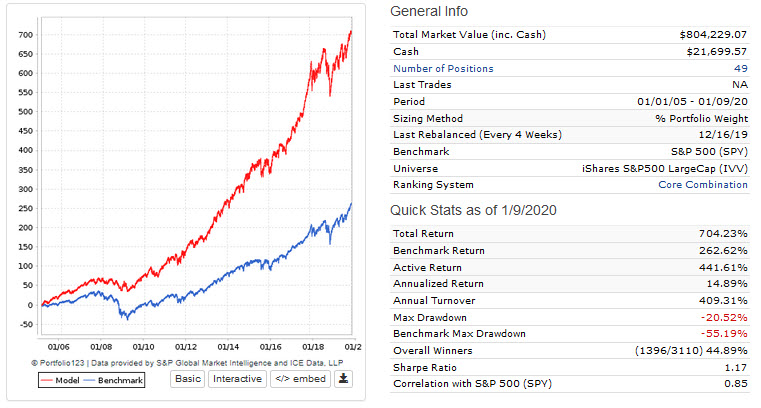

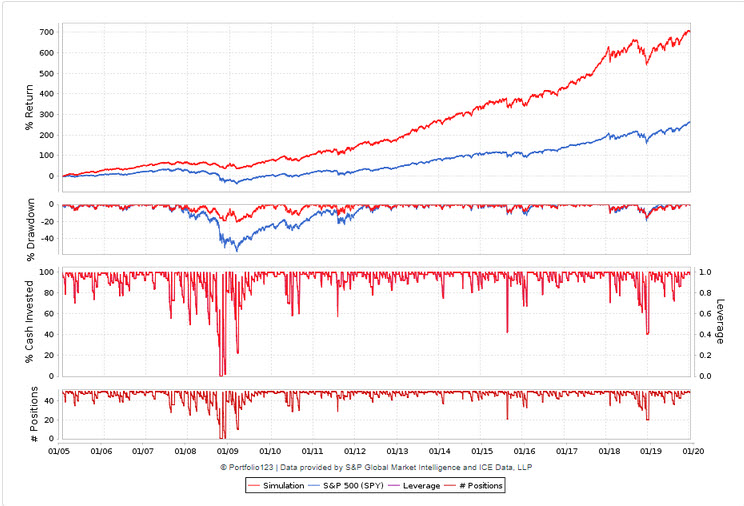

See attached/below 20 year results, variable slippage, minimum daily volume $100k. No stop loss rule.

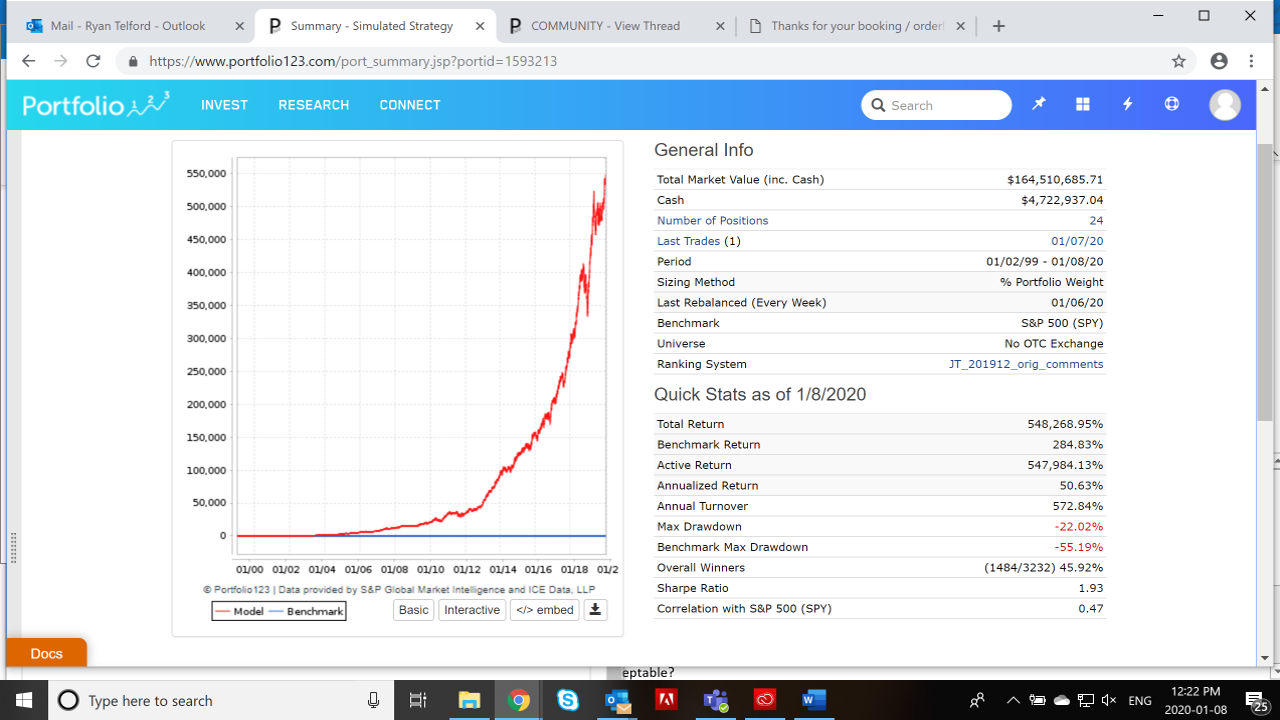

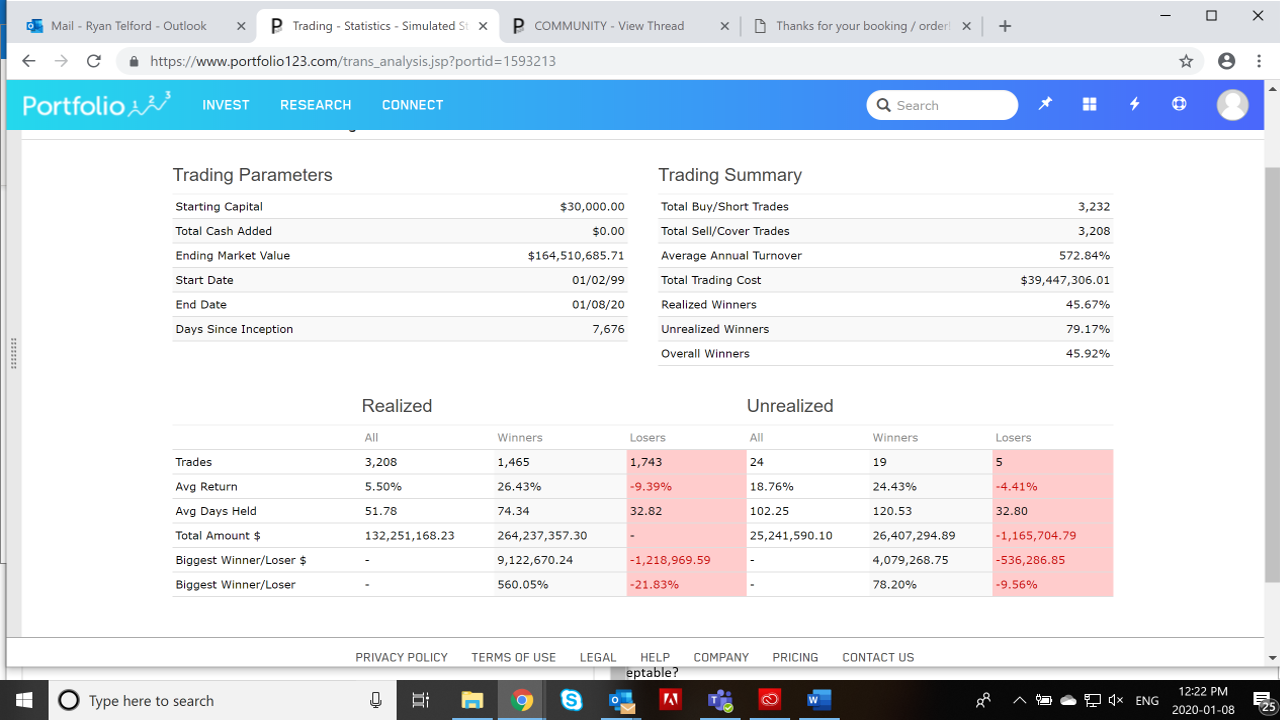

Also below, 7% stop loss, 10%, 15%.

Overall results, 7% stop loss

• Total gain over the period doubles

• Turnover doubles

• % winners decreases about 1/3

• Most significant loss in single stock decreases from 70% to 30%

• Minor improvement to max drawdown

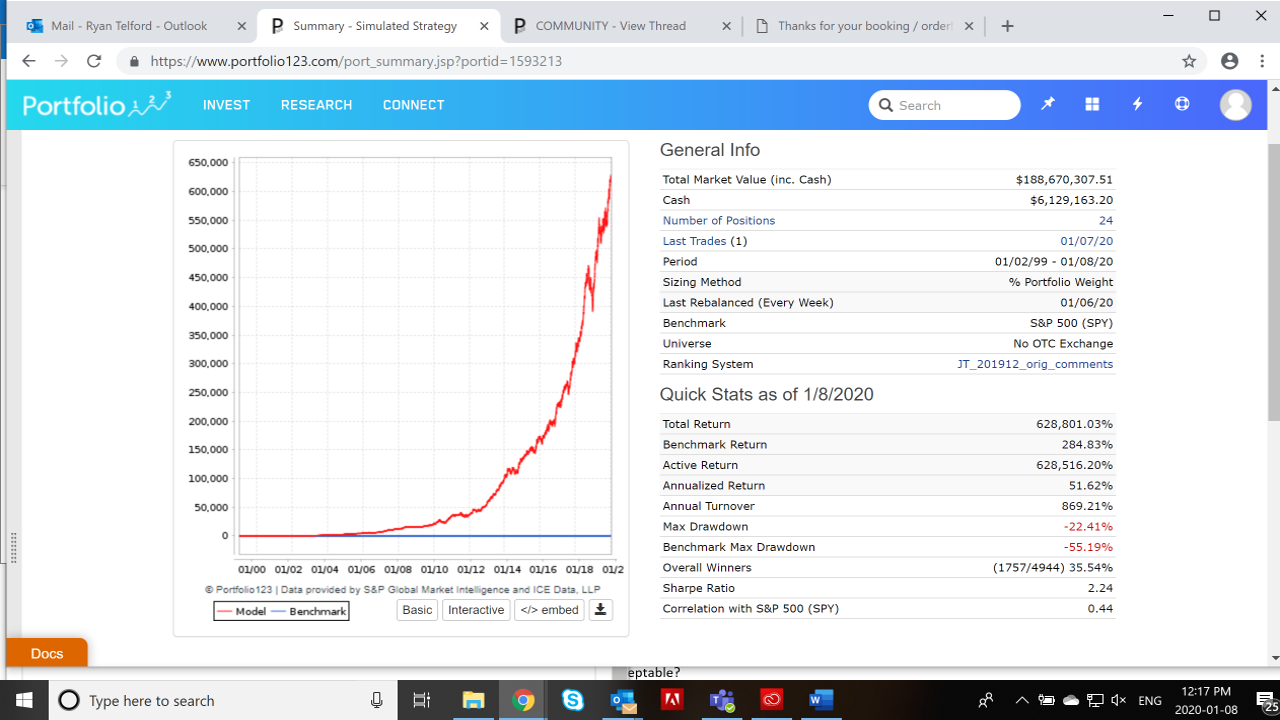

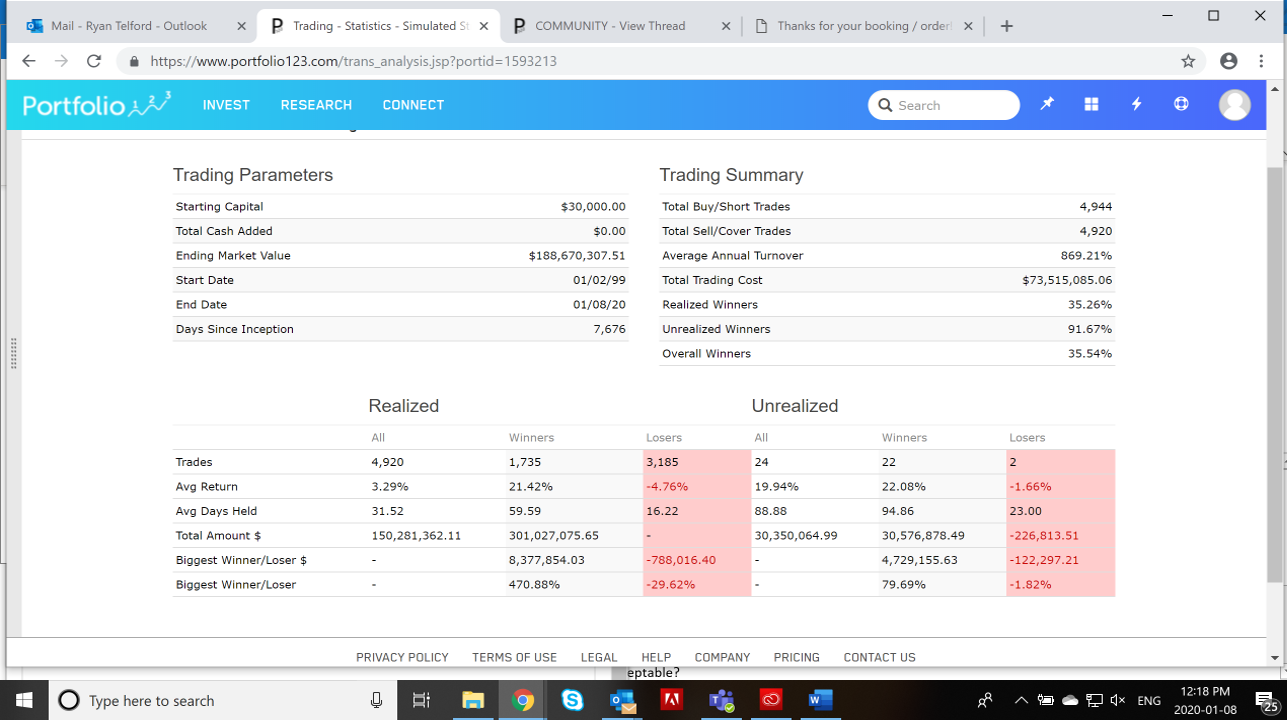

Overall results, 10% stop loss

- Performance increases, turnover improves (decreases) from 7% stop loss, and % winners improves.

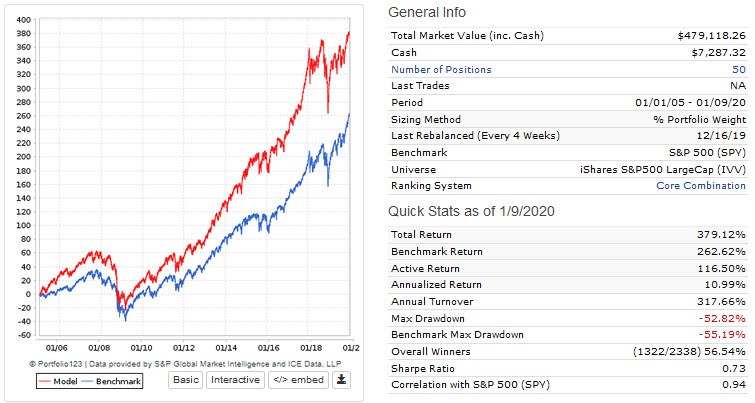

15% shown below as well.

I’ve tried this tactic on another small/micro strategy (with more of a balanced tilt, not as much growth emphasis), results being quite different. The aggressive 7% and 10% stop losses actually drop overall sim performance significantly.

Putting stop losses into practice:

My skeptical side tells me that this stop loss works well on paper but difficult in practice and OOS, even when using variable slippage.

When using entry stop losses, I understand P123 would e-mail a notification that a stock has dropped past the limit. I’m assuming this would be at close.

I’m then assuming the sim assumes that said stock is sold at open next day.

With increased turnover, many more trades, and less % winners, I see this strategy being difficult to trade, i.e. require good, timely and often trading (potentially daily), and psychological strength to see that only 30-40% of your stocks are winners (which is what O’Neil actually states is normal).

That said, I would really like to hear any practical experience from the community:

- Do any of you use aggressive (10%) entry stop losses to benefit your strategy?

- Is the trading doable? Any real world OOS issues/problems/tips?

- Is the increased performance from achievable?

Any other practical experience or thoughts on this would be much appreciated!

Cheers,

Ryan