Thank you both Walter and Paul.

Using FHist was a great idea (I forgot about that one). I can get it to work quite well by doing and add and divide by weeks as suggested above by Paul.

However it makes for a long formula when creating more complex signals. For instance if I was creating a MACD of sorts then it looks like this:

((Yield+FHist("Yield",1)+FHist("Yield",2)+FHist("Yield",3)+FHist("Yield",4)+FHist("Yield",5)+FHist("Yield",6)+FHist("Yield",7)+FHist("Yield",8)+FHist("Yield",9)+FHist("Yield",10)+FHist("Yield",11))/12)-((Yield+FHist("Yield",1)+FHist("Yield",2)+FHist("Yield",3)+FHist("Yield",4)+FHist("Yield",5)+FHist("Yield",6)+FHist("Yield",7)+FHist("Yield",8)+FHist("Yield",9)+FHist("Yield",10)+FHist("Yield",11)+FHist("Yield",12)+FHist("Yield",13)+FHist("Yield",14)+FHist("Yield",15)+FHist("Yield",16)+FHist("Yield",17)+FHist("Yield",18)+FHist("Yield",19)+FHist("Yield",20)+FHist("Yield",21)+FHist("Yield",22)+FHist("Yield",23)+FHist("Yield",24)+FHist("Yield",25))/26)

I can’t seem to get LoopAvg to work though. Am I doing something wrong?

LoopAvg("FHist("Yield",CTR)",12)-LoopAvg("FHist("Yield",CTR)",26)

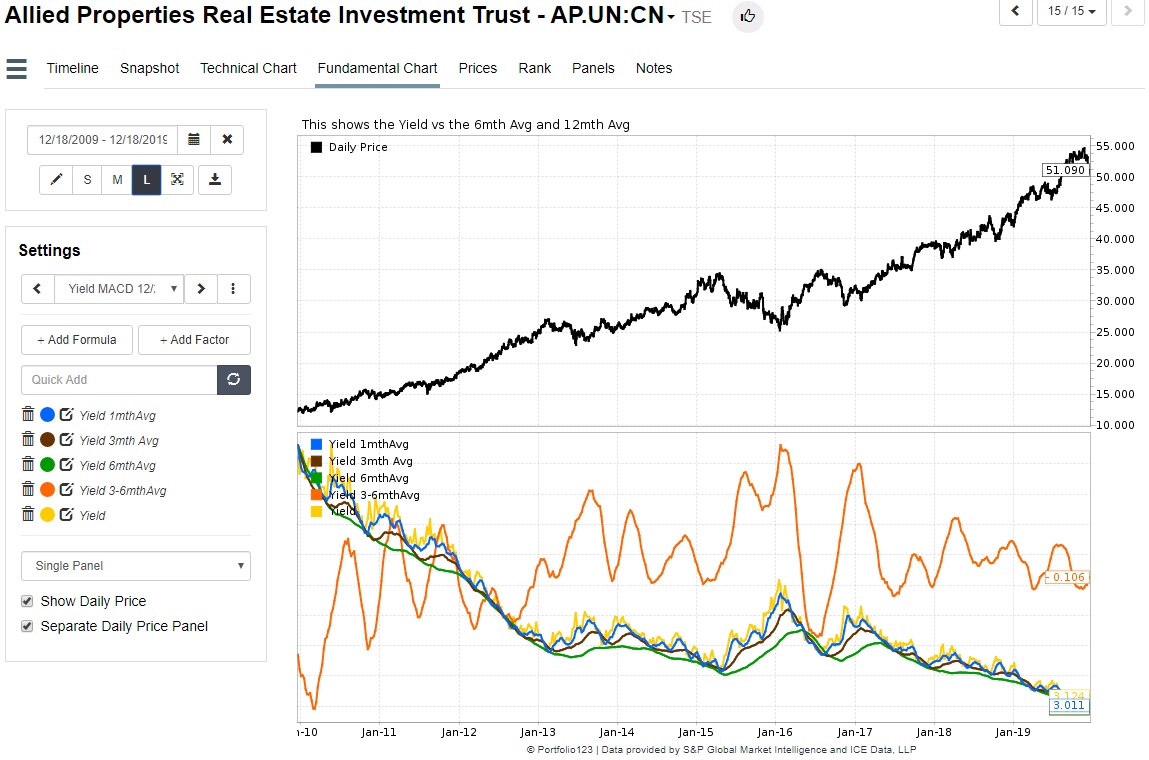

By the way it would be really nice if Fundamental Charts had an interactive vertical value line so we could scroll though the timeline with better accuracy. The grid lines just aren’t enough IMO.

Also it would be great if we could turn factors on and off in the list. It can get pretty messy when doing a study and I hate deleting formulas that you may want to add back in.