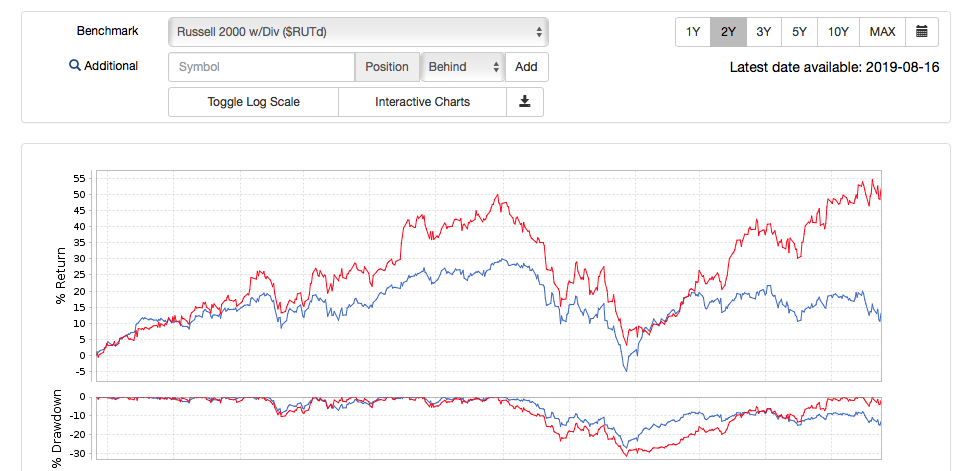

In the last few weeks the one-year underperformance of the microcap ETF IWC and the small-cap ETF IWM versus SPY has reached epic levels: -12% to -17% for small caps and -19% to -25% for microcaps. I only have data going back to 1999, but looking at this data, never before have microcaps or small caps underperformed the S&P 500 by such a huge amount. The closest they came was in 2007 for microcaps and 2015 for small caps, but it wasn’t this bad.

In my opinion it’s because the investment strategies based on index funds. If not, maybe it’s because the people are afraid and they prefer to invest in big caps, than in small ones… I have no other explanation.

I think regression toward the mean is a force of nature (or a simple mathematical truth). The different concept of mean reversion is likely to be as important.

I do not know when, but things will reverse with some ports doing exceptionally well.

More simply, Louis Rukeyser used to say on Wall Street Week: “Trees don’t grow to the sky.” They cannot fall forever either.

Yes . . . Absolutely . . . What’s happening has been completely on script. Here’s a paste-in of what I just posted in the Momentum thread:

Low-price stocks are a double-edged sword. Institutions often can’t own them, and again, that can be good or bad. The good part is that these are often under-researched companies that present attractive opportunities if approached thoughtfully. The down side is that small size is a substantial fundamental risk factor, a huge one. (See this on my blog for further details: “Small-cap Value” Is Not Just Value With A Smaller Size Filter – Acti-quant ).

The challenge in this is understanding the way market risk-on and risk-off environments impact this group. As we would expect from basic Economics 101, excess supply means lower prices and hence opportunities for the weakest buyers to buy. This applies in the capital markets as well as all others. For most of the period covered by our backtest data, we have seeb huge and often dramatically excesses in the supply of capital (and lower costs of capital, including interest rates). That caused huge amounts of equity capital to flow to the lowest quality companies, many of which are in the under $10 group.

In the past, low-priced-nano-cap-low-liquidity stocks were in great favor among p123’s most active users who, unfortunately, gave too much credit to their modeling prowess and little or no credit to the Fed for the results they achieved. When we had even a teeny weenie bit of tightening back around 2013, just after the first incarnation of designer Models came out, things got every bit as ugly as economic theory suggests. Many of the early designer models came from these users and the implosion of those models remans, to this day, the primary source of the ills that plague that offering. The tightening didn’t last so the party resumed and even now, Trump persists in bullying the Fed into keeping the spigot open.

I mention this to make the current generation of bottom feeders aware of the potential outcomes if the monetary climate changes.

Whatever you do, it’s important to always challenge yourself: Am I really good, or just lucky? Back in the early 2010s, when I edited a low-priced stocks newsletter, I measured myself against a custom benchmark I manually built on p123 and with Excel processing that measured only the bottom-feeder part of the market, a segment for which there is no established benchmark.

That was more about the smallest part of the small end of the market, but it applies to small in general. Capital remains in oversupply so small caps have th potential to improve near term — subject to the unfolding Trump lunacy and concerns he’s toss the world into recession in which case the riskier segment of the market can be expected to fare much worse.

The universe of small companies has been shrinking for years. This cannot be good:

“Last fall, around the time Facebook announced it was buying WhatsApp for $19 billion, a flurry of studies offered a startling revelation: The U.S. startup rate has been falling for decades. The Kauffman Foundation, citing its own research and drawing on U.S. Census data, concluded that the number of companies less than a year old had declined as a share of all businesses by nearly 44 percent between 1978 and 2012. And those declines swept across industries, including tech. Meanwhile, the Brookings Institution, also using Census data, established that the number of new businesses is down across the country and that more businesses are dying than are being born.”

Microcaps have been capable of lagging for decades at a time during the 20th century.

One possibility is that decadal (de)conglomeration fads are at the core of the microcap vs large cap performance differential. I find this plausible since fads actually do drive investor behavior.

You know bridgeway capital? Its BRUSX fund (bridgeway ultra small company fund) was the best performing fund for a long period, focusing on very small value stocks. Same with Fidelity Low Price stock fund (FLPSX) run by Joel Tillignhast which was also one of the best performing mutual funds for quite a long time. These had amazing historical track records, even just a few years ago. Now look at them. The are getting crushed by the S&P 500.

I’m not quite sure what to make of it. My guess is a lot of people using this site are suffering big time because all the historical backtesting would show that small undervalued and quality companies outperform. They did, no doubt. Up until about last year. I’m quite frustrated with it, but i’m not changing. What am I going to invest in otherwise? Momentum stocks? lol that is the quite the dumbest strategy i’ve ever heard. Let me tell you these folks are going to be burned eventually just like all the bitcoin/beyond meat/netflix investors. What else, treasuries? lol inflation adjusted 0% returns, no thanks. S&P 500? That has been going up to no end. You’ve got these ultra big stalwarts that seemingly never go down. They will. I just can’t pull myself to buy a fund the weights expensive stocks more than cheaper stocks.

Tell you what. I’m going to keep buying these companies that are quality and undervalued and unloved. I don’t care if they go to 10 cents, i’m just going to keep buying them. I may be wrong, but if thats the case, we are going to have MUCH bigger things to worry about if all these non S&P100 companies all disappear.

If small/microcaps underperformance are the canary in the coalmine for risk off sentiment (not unlike an inverted yield curve), it seems to fall in line with continued pessimism for future earnings. People are preparing for pain.

The past is never a reference for the present or the future. If it was, there would be no evolution and no development.

The economy and capital allocations have changed in big ways over the last 40 years. Banks and pension funds hold much more capital than before and their preference is investment in large blue chips.

I am sure that they looked at mergers and acquisitions but this was not address in the article (or I missed it).

Seems this would affect the numbers with the good (small) companies disappearing—along with their profits. Or often the companies are bought before there is much profit—skewing the results in another way (maybe).

The profits of the small companies would then move to the big companies then wouldn’t they?

Who thinks a small drug company with a great new drug will still be here in even 3 years. Could be a good stock to buy before the merger.

Again, I am sure they thought of this. I wish I knew whether they found it to be a significant factor.

A lot of what they say relates one way or another to scale, which is standard stuff. I’m quite surprised though that the authors did not consider the spectacular and obvious impact of M&A.

Seems like they determined at the outset to conclude that investment in intangibles is where its at (a nice HBR-ish theme) and molded the data to fit the conclusions. Nut even with R&D, they don’t see, to have dug below the surface. If that’s the key to growth, then why is big pharma struggling? You can’t divorce R&D spending and productivity from the nature of the technological life cycles in different areas. Pharma seems to have shifted and it looks like the new paradigm will be in the biotech-genetic areas, so there, the mega caps of the next generation may more likely be today’s small companies rather than the Pfizers of the world . . . Unless the M&A folks stir the pot.I’m sure there are many p123 users involved in scientific areas who could speak a lot more eloquently on this angle.

There’s also the pace of technological development. It’s a lot faster today than it used to be, meaning the UBERs of the world don’t need to spend a lot of time as micro caps, small caps, mid caps, and then large caps. They go through all the stages, but some are so fast, they barely get noticed and are over and done with before the company even goes into the public markets.

There are also a lot more crappy small companies today; as I said in a prior post, it’s easy for lousy companies to get capital. When it’s harder to get capital, companies need more talent and better ideas than many have today.

I also think the HBR folks underestimate the impact of large firm bureaucracy. It’s there. But some companies are more talented than others at controlling it and speed/momentum/M&A helps them continue to run.