Hi guys,

I’m wondering if short term mean reversion (1-5 day frame) still work for overbought and oversold stocks? Anyone have any models showing they still work or don’t work?

Hi guys,

I’m wondering if short term mean reversion (1-5 day frame) still work for overbought and oversold stocks? Anyone have any models showing they still work or don’t work?

I think it does but it adds a tremendous burden in slippage costs. I use one-month rather than one-week mean reversion myself, but it makes up only a tiny fraction of my ranking system.

Yes, it still works very well. I would recommend using it on super liquid stocks though. Only those with $100mm trading per day minimum. I am about to start live testing a beta-neutral product with up to 20 stocks per side. I know a guy running a similar type model long-only. Between his 2 models, it can handle nearly billion in capital he figures and so far has an average price (commissions and slippage) only a couple pennies above VWAP. With $30 average share price - cost to run is low. And he figures he can get trading costs lower yet by using a trading desk.

Back-tested returns for my beta-neutral model are between 20 - 25%. I sure there are all sorts of things I am overlooking which is why I want to take it live for a bit to work out the kinks.

As for research…short-term reversion is the strongest generator of alpha in all markets (Europe, Asia and N. America) when tested in WorldQuant. But as Yuval pointed out, you really need to be careful about slippage. I find that this approach works best long/short instead of long-only. Decent short alpha present.

You can look at the ETF UTRN to see their take on one week mean reversion.

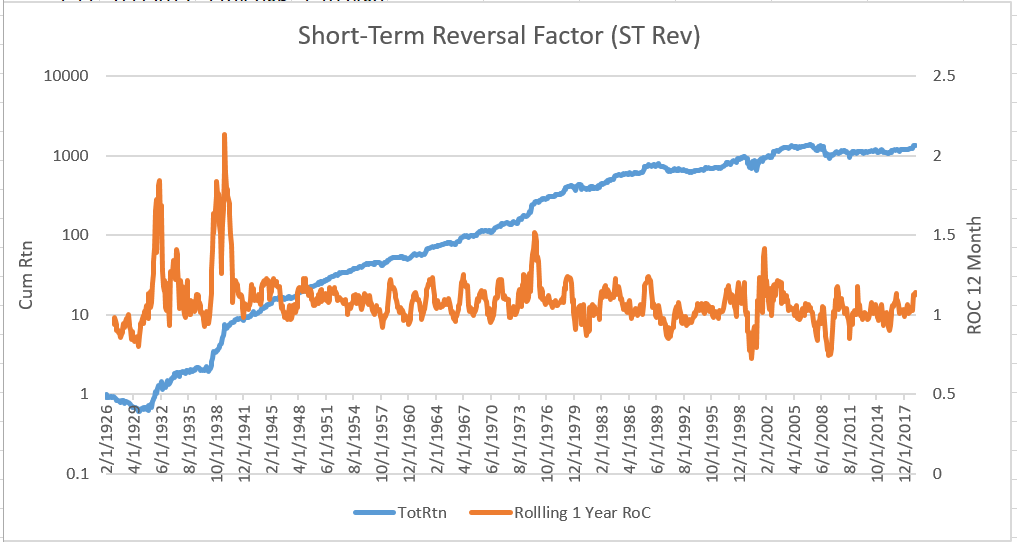

I recommend you play with data under “Short-Term Reversal Factor (ST Rev)” on Fama-French’s data library: Kenneth R. French - Data Library

The gist is that it has been decaying since its discovery.

This doesn’t mean it’s gone, but rather that past performance was likely better than future performance will be. As a workaround, I use more complex methods of measuring reversals (i.e., deviations) that a) have a rational basis, and b) are difficult to replicate.

As they say, the future ain’t what it used to be.

I use both shorter term and longer term mean reversion elements. Shorter term elements can jostle the rankings quite a bit from week to week, so turnover is increased. I haven’t figured out how to specify this properly, but I suspect there’s a difference to mean reversion when the entire market is going down vs. when the entire market is going up, and suspect it may work differently in some sectors than others - defensives vs. cyclicals in particular come to mind. And it might just depend upon the end model used as mean reversion makes it more difficult to ride long uptrends if that is your approach, as it will often advocate for selling winners.

But I guess short answer is yes. After you’ve built a model try putting in short-term reversion factor on timeframes of 5-20 days. For me it tends to improve the model, keeping in mind turnover. Caveats above apply though. Behaviorally it could be problematic.