Hi all.

I would like to share a sim that I’m working on it, it’s based on a web page where they offer analysis focus on dividend investment (https://www.simplysafedividends.com), I’m a subscriber and after reading a few of their analysis I realized it’s all the same (more or less) and I can “extract” a system to invest focus on dividend investment just reading between lines.

The following are the points I departed from:

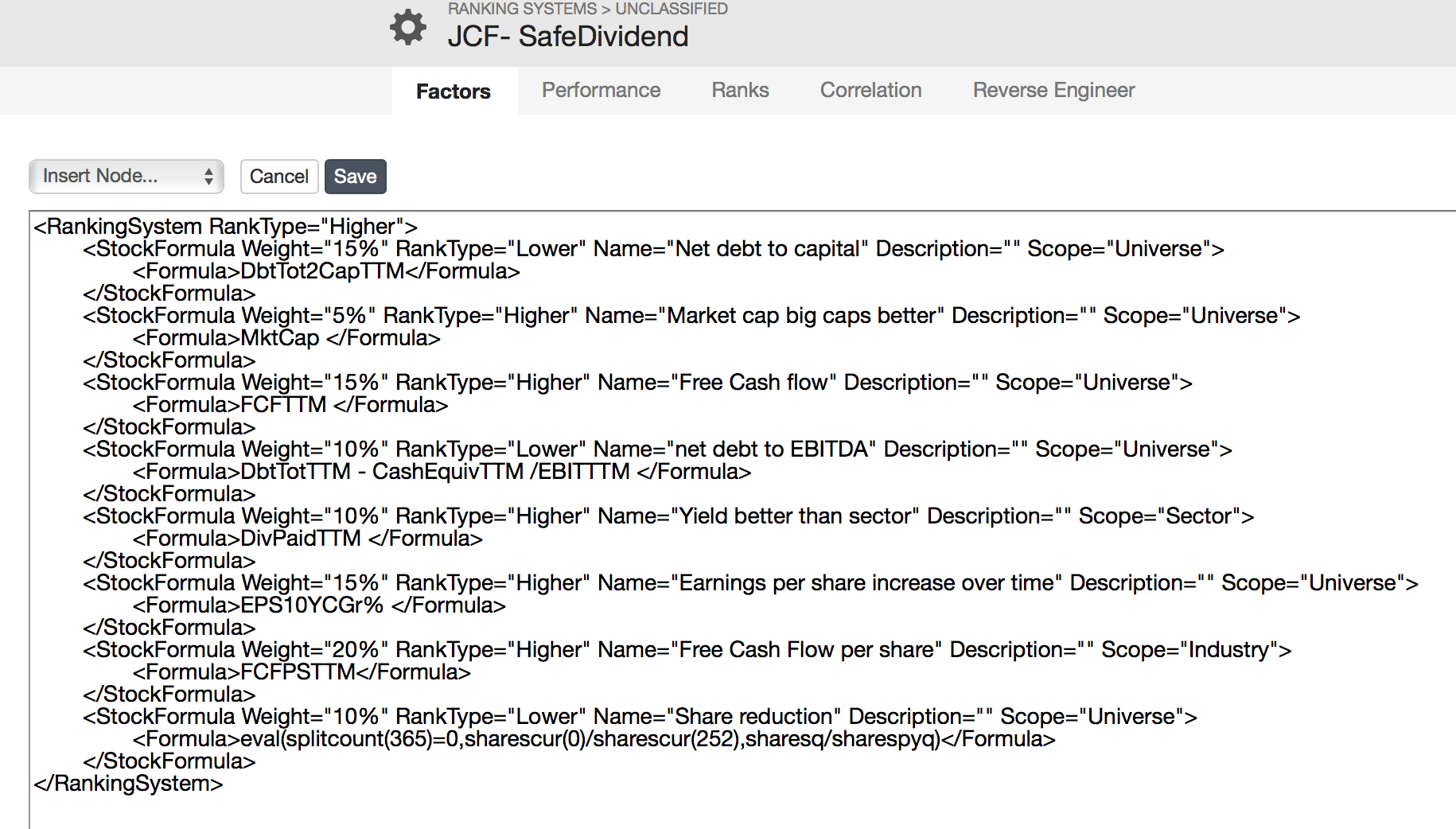

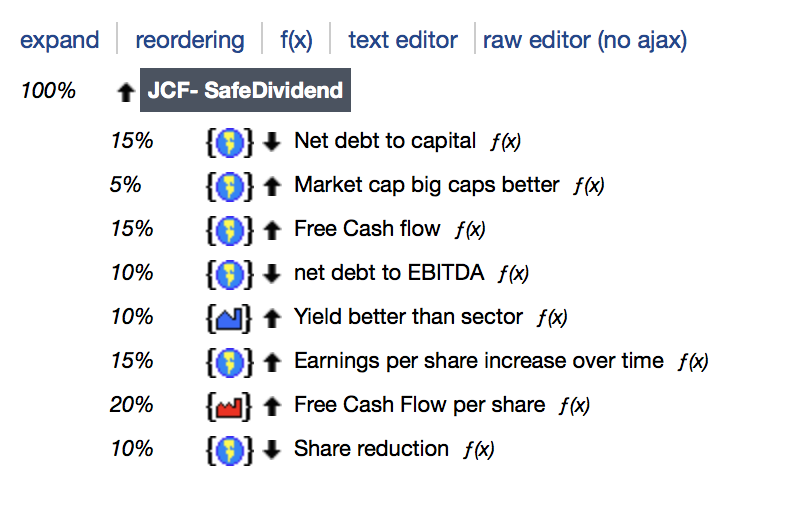

[i]net debt-to-capital- important.

net debt-to-EBITDA - (the lower, the better).

How long a company has paid uninterrupted dividends – important.

Larger businesses better.

free cash flow- important.

dividend yield better than industry

fordward p/E ratio better than industry

P/E ratio means that investors may have become pessimistic about prospects for growth.

Earnings Payout Ratio- below 60%

Free Cash Flow Payout Ratio- below 60%

Earnings Per Share- The best businesses will steadily increase their earning

Free Cash Flow Per Share- Advantaged businesses tend to generate stable, growing free cash flow over time.

Earnings Per Share Growth

Sales Growth- prefer steady, moderate growth (3-7%).

Shares Outstanding (Millions)- prefer a declining share count.

Total Sales (Billions)- prefer companies with fairly steady and moderately rising sales.

Return on Equity >10%

Return on Invested Capital >8%

Operating Margin >12%

Free Cash Flow Margin >5%

Net Debt to EBITDA <3%

Net Debt to Capital <0.4

Interest Coverage >8%

[/i]

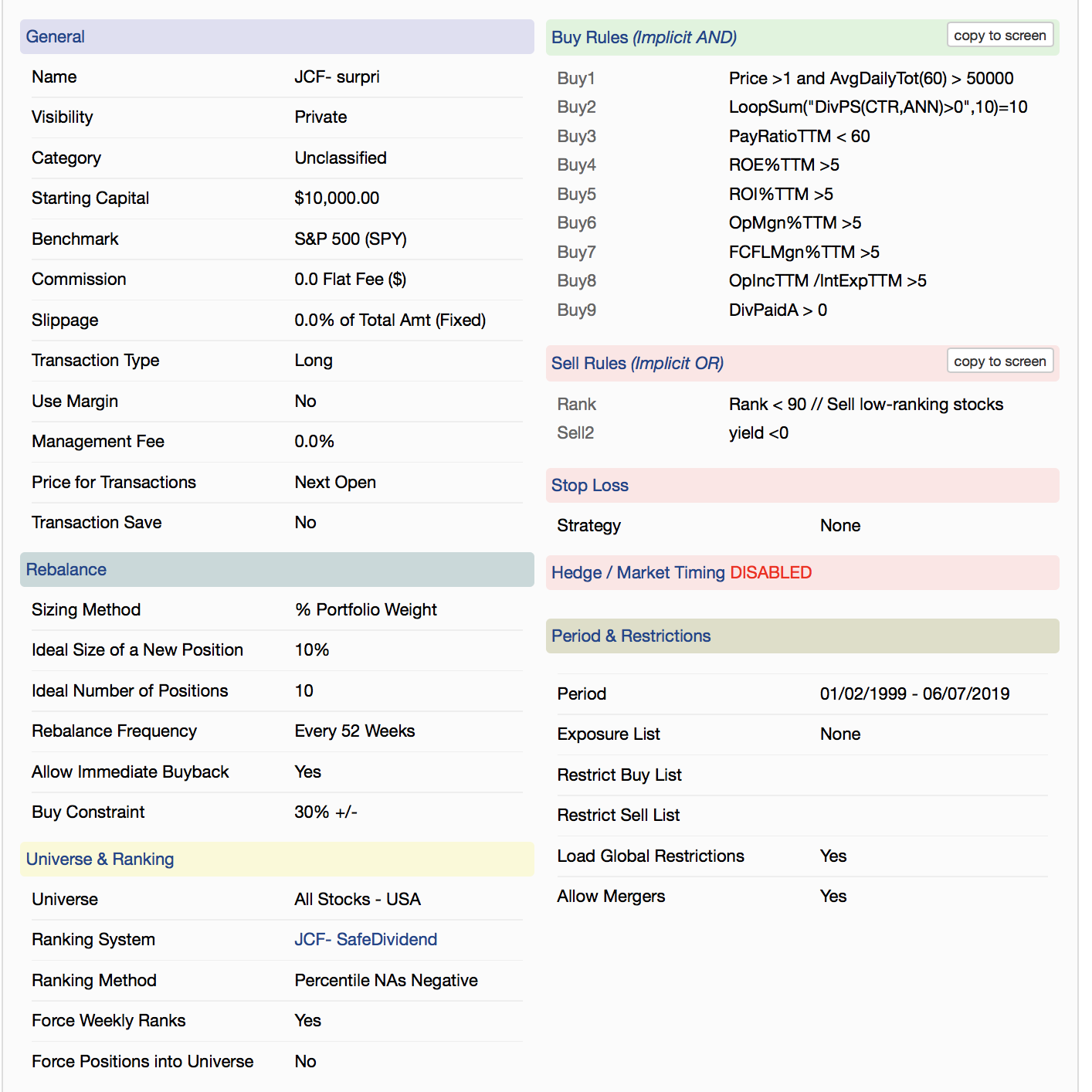

Then I created a ranking system for some factors, and I placed others in the buy and sell rules.

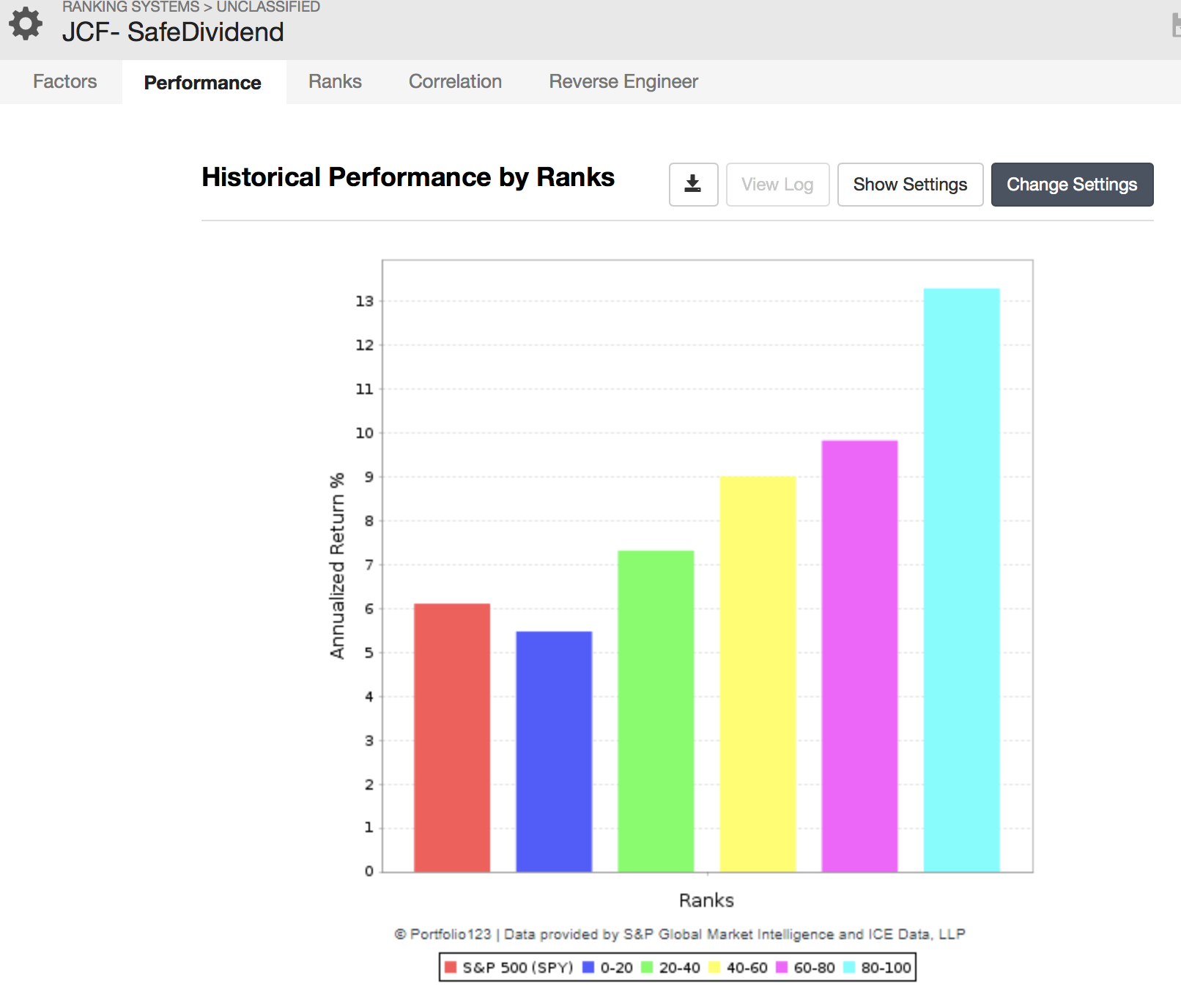

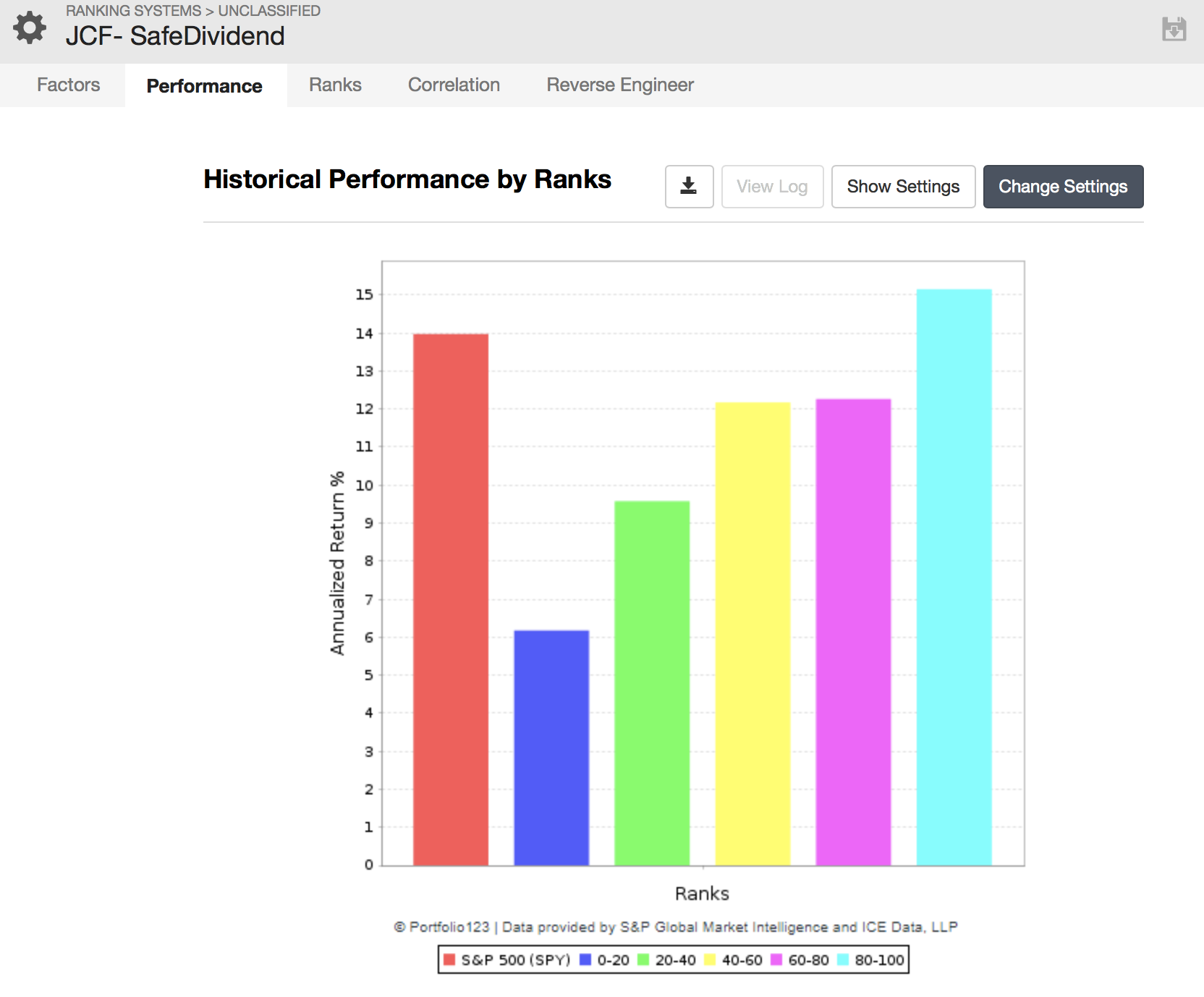

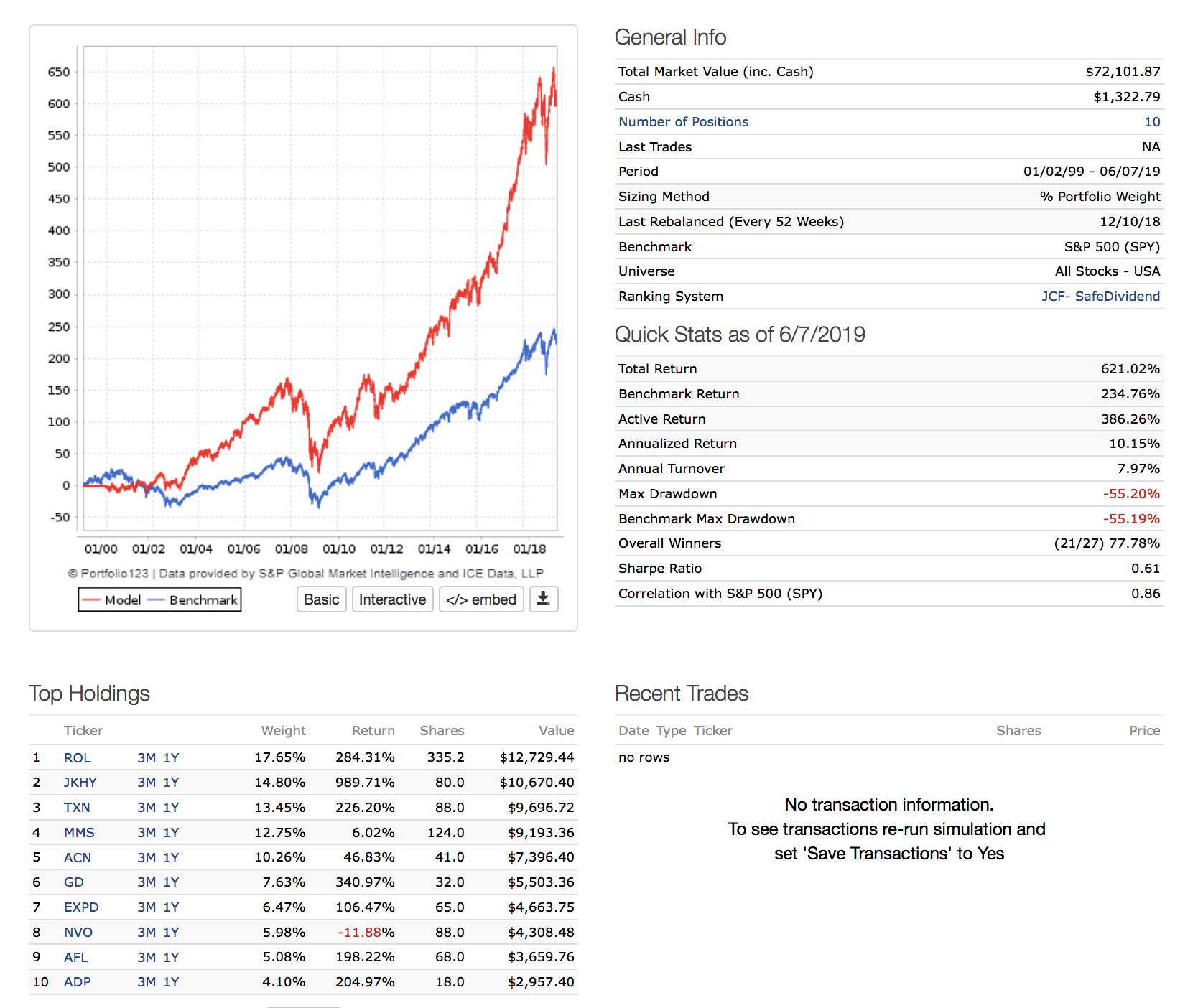

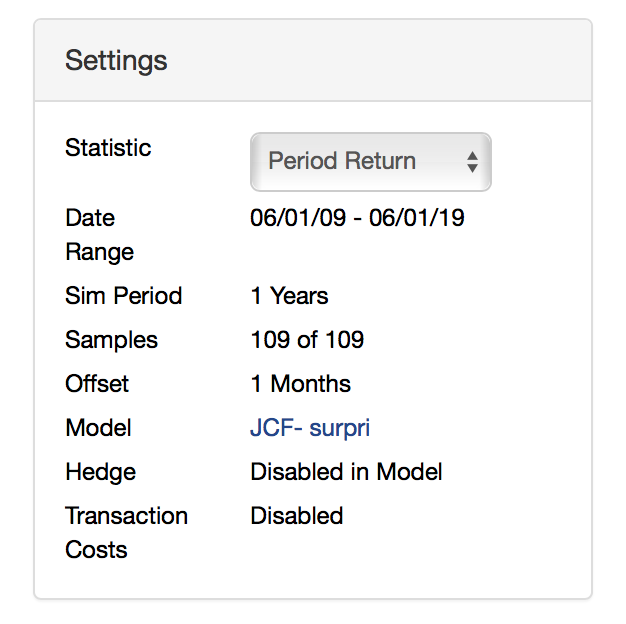

The ranking works very good in the last 20 years, but in the last 10 years not as good at it was.

And about the sim, if I follow the “rules”, the system it’s a disgrace, it underperforms the index a lot, I guess it’s because it’s too much demanding and there are no companies that matches the criteria, but if I relaxed the rules, and take out some of them, then it works more or less fine.

I would like to know your opinions about that sim and about the ranking.

Do you think it’s a good way to approach to the market?

Are the factors well distributed between the ranking and the buy and sell orders?

Thanks.