Beginning August 31, S&P is going to be limiting the constituents of these indexes to people who pay them for their use. Portfolio123 is considering whether or not it’s worthwhile to do so. We believe that we can create our own, similar indices and offer those on our website. Alternatively, we could continue to offer them but charge members a little bit more to cover the expense (it’s not cheap).

How important are these indexes and their constituents to you? Would a substitute work for you? If not, would you be willing to pay a little extra for their continued use?

That the "benchmark’ for a sim be the average of the returns (equally weighted) for every stock in the universe.

Would that be computer intensive? The average would have to be computed for each rebalance period to be useful, I think. I would use this over the benchmark in any/all sims, I think.

I would call it an improvement then, whether we ended up paying more or not having the official index.

Same as wwasilev (depending on how much is “little extra”): SP500 and -possibly- SP1500

The free “our own similar indices” should still be there by default. Those who want the real deal can pay extra as needed.

By the way, what would it cost to have the real constituents of the R1000?

edit - delete. I just reread your post, and I think I initially misunderstood or didn’t properly register your comment about “constituents”. I’m fine with P123 produced index constituents. Something mirroring SP500 would be most valuable to me as I think SP500 companies do backtest differently than other large non-SP500 companies.

edit2: I wonder if a company like Vanguard might have an automated way to share their index ETF compositions/holdings?

I do not currently use the constituent lists, since I don’t use sublists from them or consider if a company is in them. However, I assume that factors such as S&P earnings and yield will continue to be available, and the related indexes. Those I do currently make use of.

Yuval,

What does this actually mean. Is S&P going to keep the names of the companies in these indexes a secret, and only available to people who pay? Good luck with that.

If nobody pays then those indexes will disappear to be relevant. I think P123 can clone those indexes, similar to the PRussell’s. I would not pay extra for the S&P info.

What an extremely odd business decision by S&P. They’re getting basically unlimited brand and marketing promotion having their name affiliated with something that’s really not that difficult to replicate. Why mess with a good thing?

I don’t think it’s uncommon for a company to license it’s index data - especially for commercial use. And it has nothing to do with keeping anything secret. Use their data, pay for their data. I do want to keep the S&P500 historical data and I don’t think it’s possible to reconstruct the index programmatically. Even the S&P 500 has an Index Committee that has some discretion in selecting stocks or responding to market events.

Can we use etf’s as benchmarks (Vanguard was mentioned, e.g. VOO, VTI, etc.) And for universes do an approximation to the SP500 (i.e. starting with the 500 largest firms on the NYSE or whatever). If we used the ETF’s for constituents, there would be a time lag. I think I’d prefer to roll my own universe than pay S&P, unless the cost was trivial.

Perhaps it is time to start our own index.

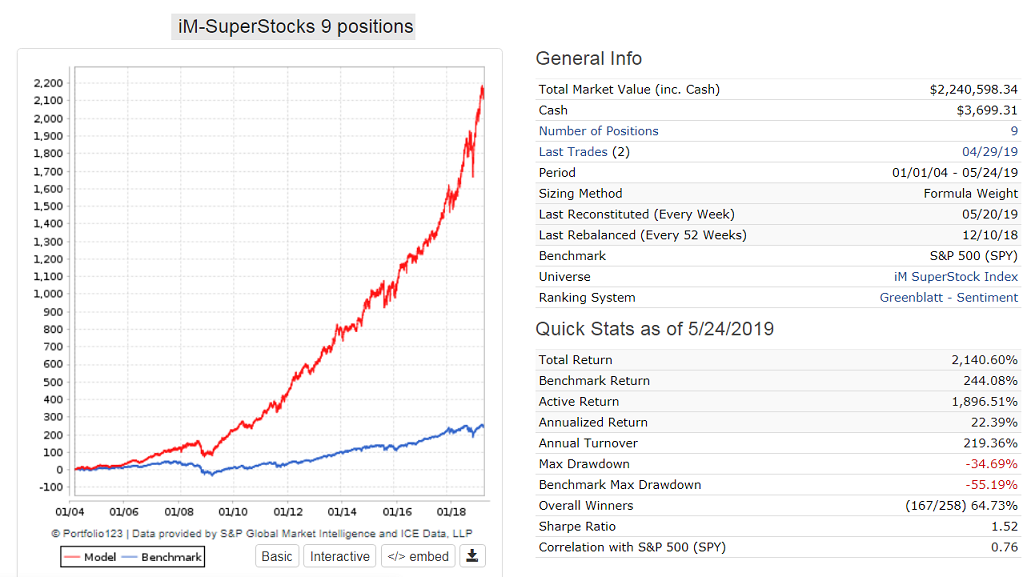

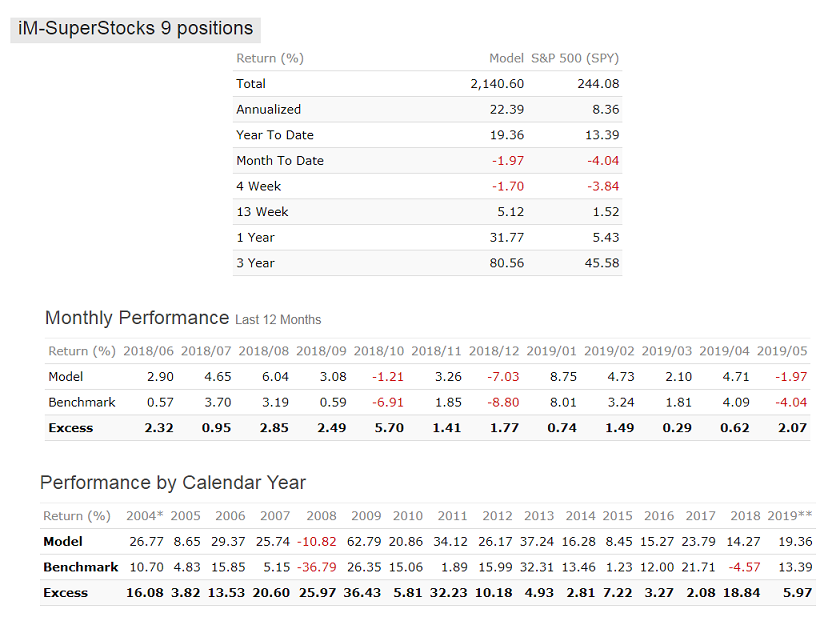

Here is a sim with 9 stocks from the large-cap iM SuperStock Index. Perhaps I should sell the constituents as well. I could charge much more than S&P because my model beats SPY every year, and also every month for the past 12 months.

As far as “reproducing” the SP500 universe with rules we got around 93% match (the key factor turnout to be a rank of the #Institutions that own the stock). 10 years ago it’s around 89% match. This technique did not work well for the 400,600 and 1500. I don’t think we’re going to do this.

Worst case scenario we will only provide these SP universe for the present so that live strategies that use them are not affected. The universe management will be done manually. Simulations that use them will suffer from survivorship bias.

The money they are asking seems excessive , specially since we only expose 4 of them. It’s about 20% of our entire data costs (prices, financials, estimates, gics) !

These indices are probably more valuable to our professionals and universities. We’ll reach out to them to see what they think.

One last funny note. We run an SP500 screen on Yuval’s Fidelity account and it returned 506 stocks. So obviously they are not paying for the data, they don’t care too much to fix it, and their users don’t mind either.