Hi all.

I’ve been working a little with the ranking systems P123 have in their system, the 34 of them, and I am a little bit concern about some facts I would like to comment with you.

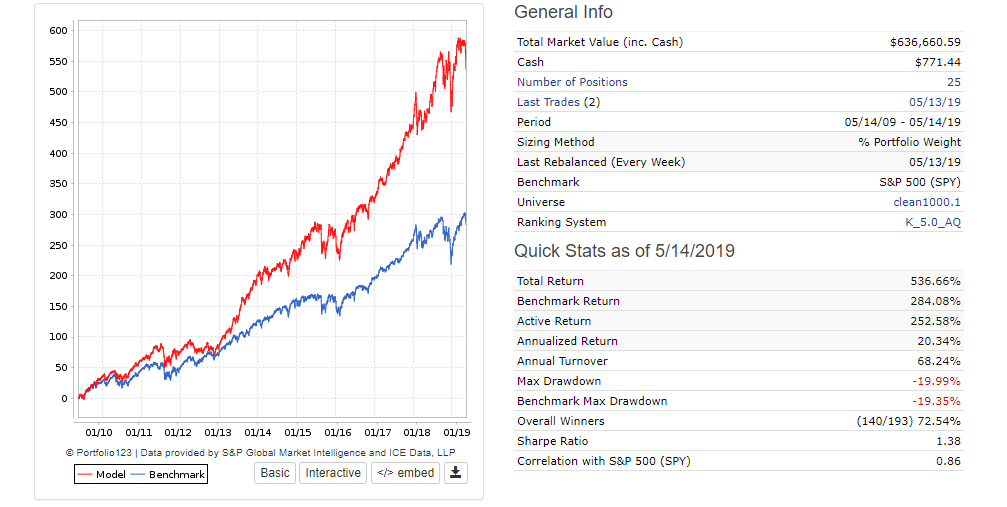

First of all I created one sim, and then I just changed the ranking system and see what happeds in different periods of time, and in different rebalancing periods. The idea behind my “movement” was to see which ranking performs better.

The surprise where that while almost ALL of them work pretty well before 2008, ALL of them underperfom the market from 2008 and ahead.

The benchmark (market) in my sim, is the S&P500, and for my first test I pick the stocks (Universe) in all the US stocks except in the OTC market.

Only one buy rule;

Price > 1 & AvgVol(20) > 50000

And one sell rule;

rank <90.

That’s it.

First I did it with 100 stocks, then with 20.

Then, I keep the benchmark, but I pick the stocks from the S&P500 itself, just to know if the rankings of P123 have some edge over the benchmark.

The answer was NO (talking about 2008 and ahead). And it’s very surprising to me. Almost all of the P123 rankings underperform the S&P500, or went clearly under the benchmark.

It looks like the market conditions changed a lot, to 2008 from now, and we are just digging with the wrong tool, a one that used to work pretty well, but nowadays don’t.

And, of course, if I add some extra buy rules, to the sim, the performance improve, but I’m little bit confuse about it and I do not know what to think about.

Did you experience the same?

What happened here? Any ideas?

It’s time for P123 to create new ranking systems?