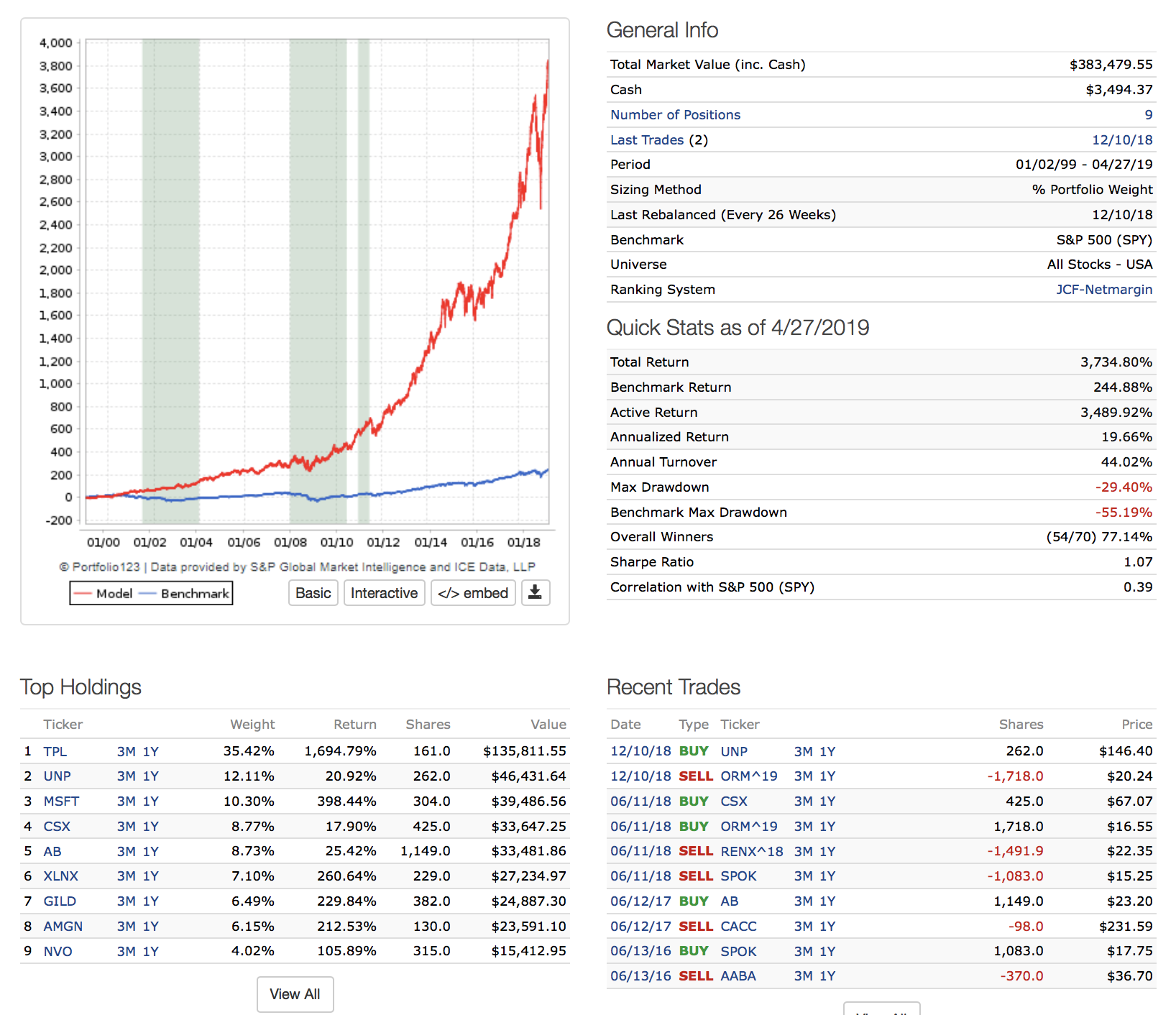

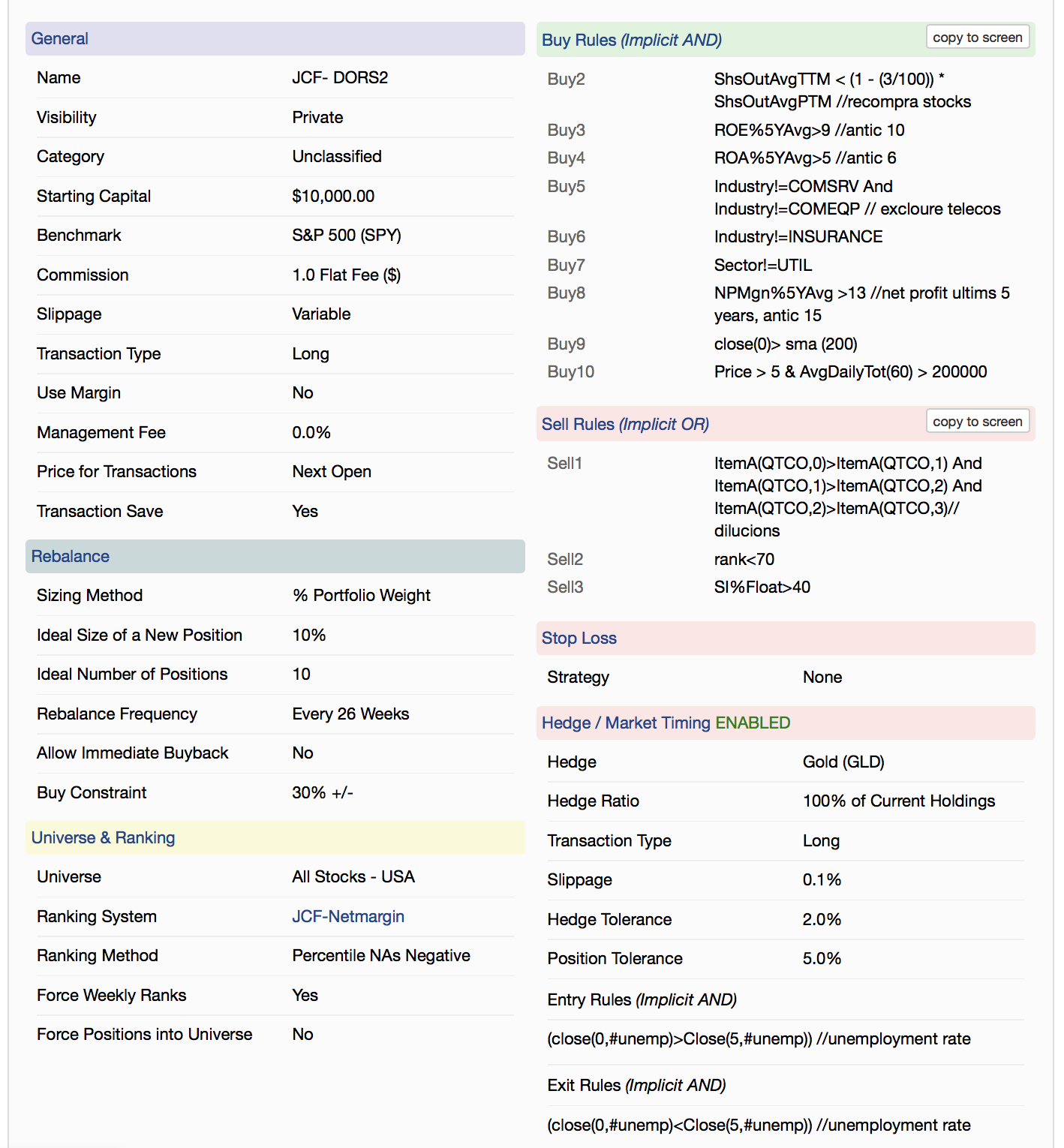

I do not want to be a pain, but I will aprecciate some feedbacks about my sim. It’s an improvent of the last sim I commented here. Just I add some rules more, and a hedge, one based on unemployement rate.

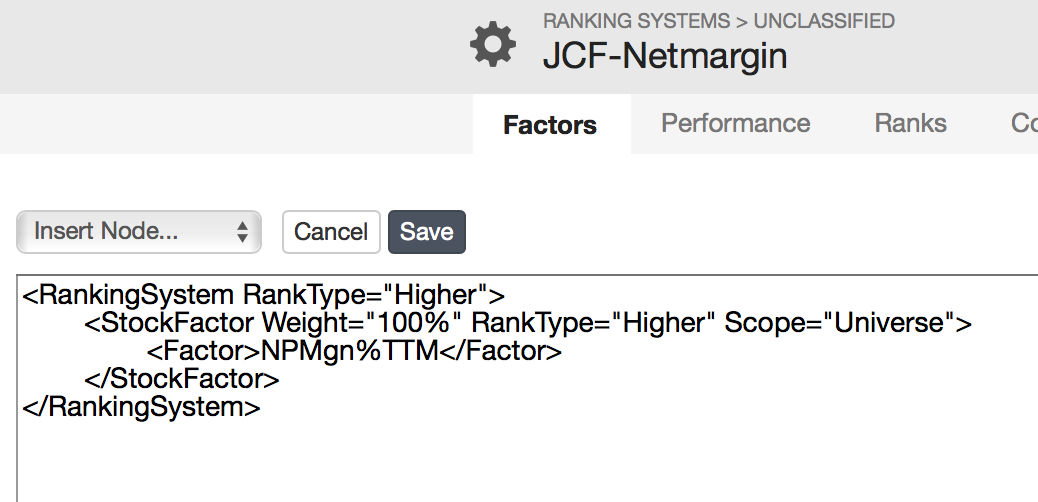

I experimented with a lot of ranking systems, and more or less works the same, I do not understand why.

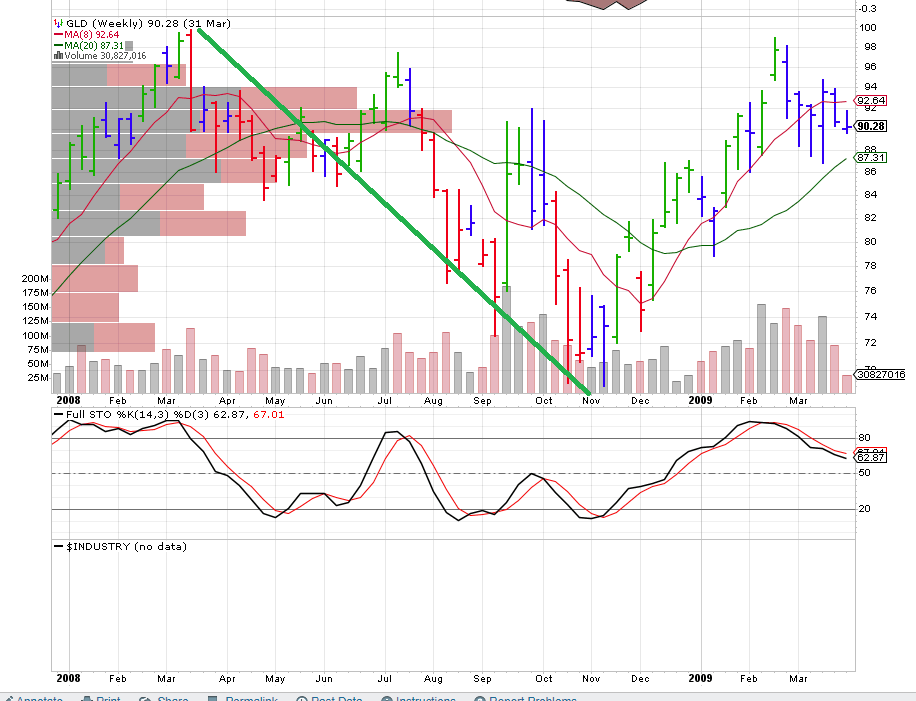

Pleasae, also post hedge by cash. Gold is material it trade differently decades to decades, because of last recession gold was safe heaven it does not mean it is wise to invest 100% without any diversification into Gold. (Note: in 2008 GLD went down to 30% at peak of recession).

Any reason why to disclude industry and util; if it is for improve performance, few years from now different industry will perform worst; can’t keep adding buy rule to ignore the industry which is underperformed in the past without sound reason.

as some people will ignore energy sector and real estates, as it is controlled OPEC decision and interest rate based on FED decision and comment which impact more than profit and earnings of a company. it will be considered as sound reason from them.

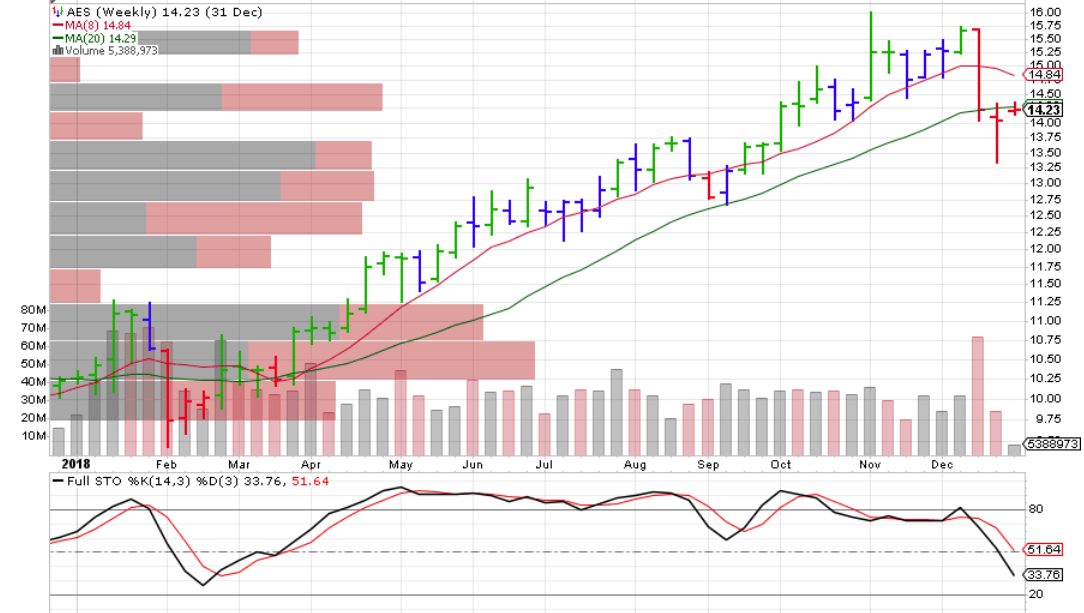

AES belongs to UTIL sector which performed best in 2018 with 40 pct return.

Please, send personnel email to Mgerstein p123 to review your sim. you will get more positive feedback 1 to 1.

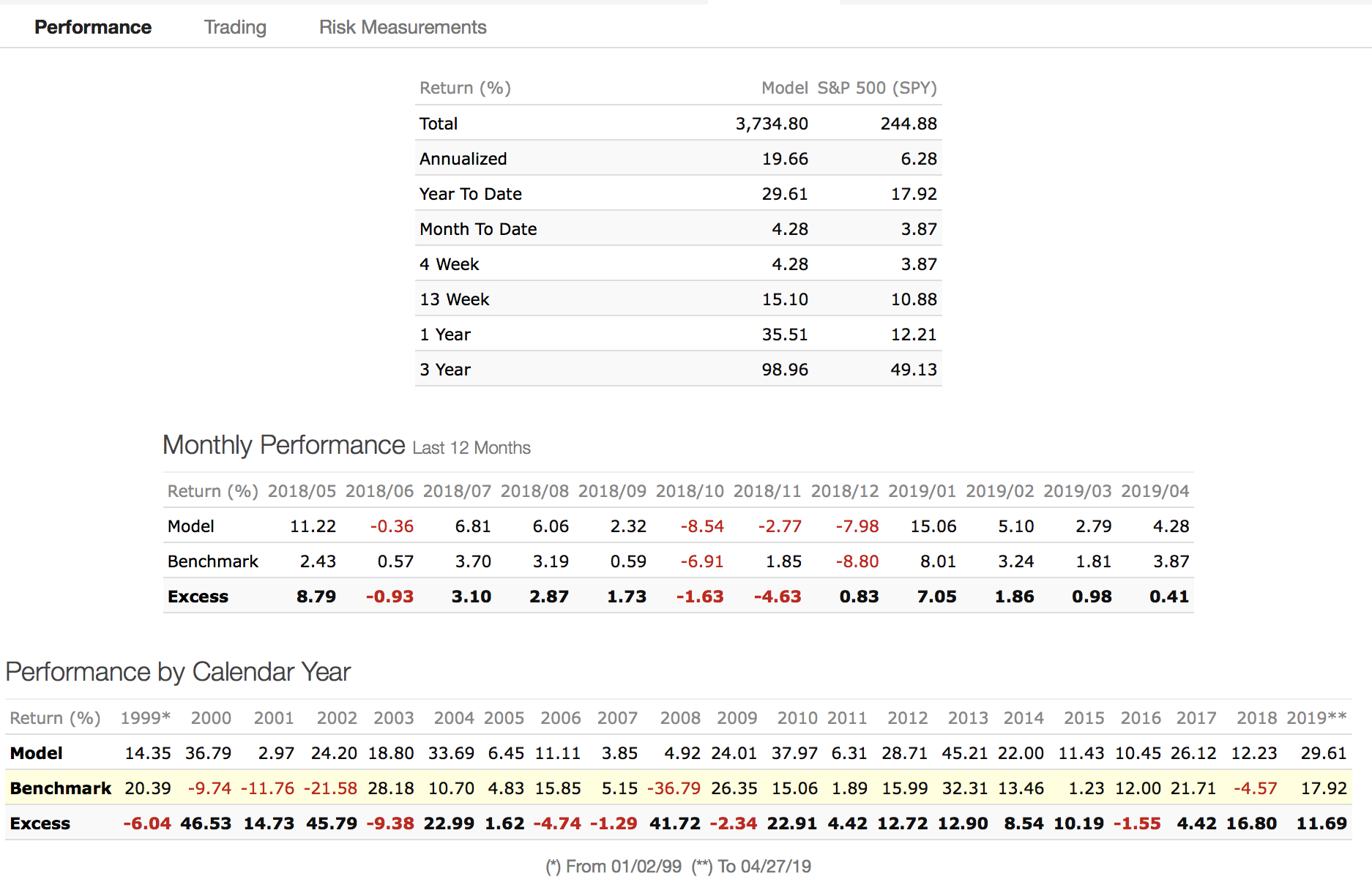

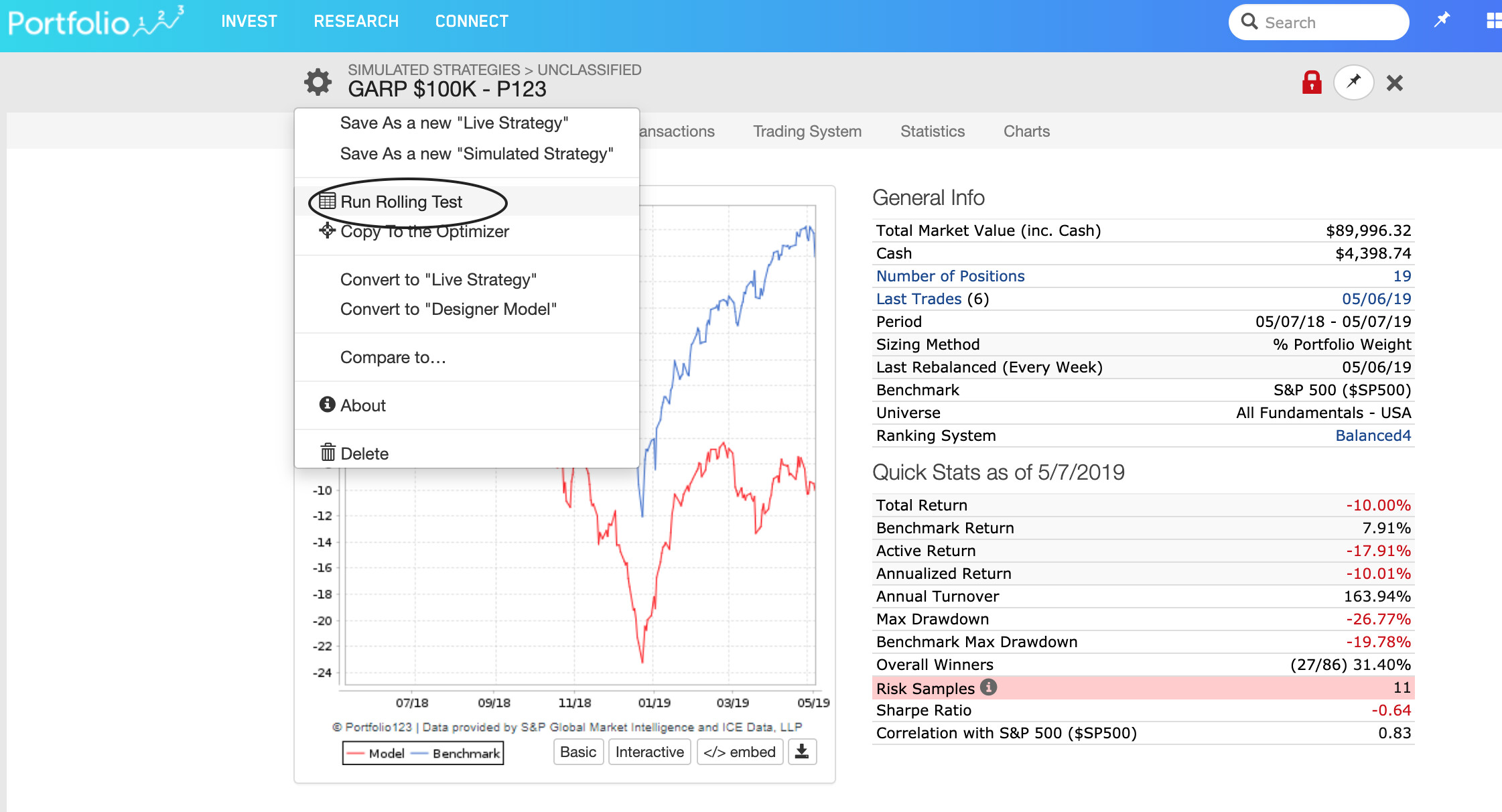

The biggest thing I would do at this point is run a rolling test. It is such low turnover with only one ranking rule that there is a high chance that this is overly fit with Jan 1 1999 as your starting point. Rolling returns is a great too. Run it as a weekly offset and a one year holding period between 1999 and today. Then capture a screenshot of that and post it. Is the average 1 year return still nearly 20%? How much variance in the 1 year return is there with weekly offsets? How often does a one year period out-perform the market and by how much?

I would say that this definitely should be your second step. If it holds up to that…fantastic. If not, you may have to re-jig a few things.

1- Yes, you right. Just I choose gold because it performs well on the sim, but I’m sure in real live I wouldn’t go all in in gold.

2- I have nothing personal against any sector, but the sim it’s just an idea that comes from a book, and the author say that sectors are not good, then I exclude them in the sim. There is no other reason.

3- Is that normal here? Can I send a message to Mgerstein to discuss about my sim??? You do that?

When you’re in the screen view, adjacent to the “backtest” tab is a “rolling backtest” tab. It will automatically vary the starting dates and holding periods for you over a range of time. (For example can run stats for every 3 month holding window starting every rolling 4 weeks)

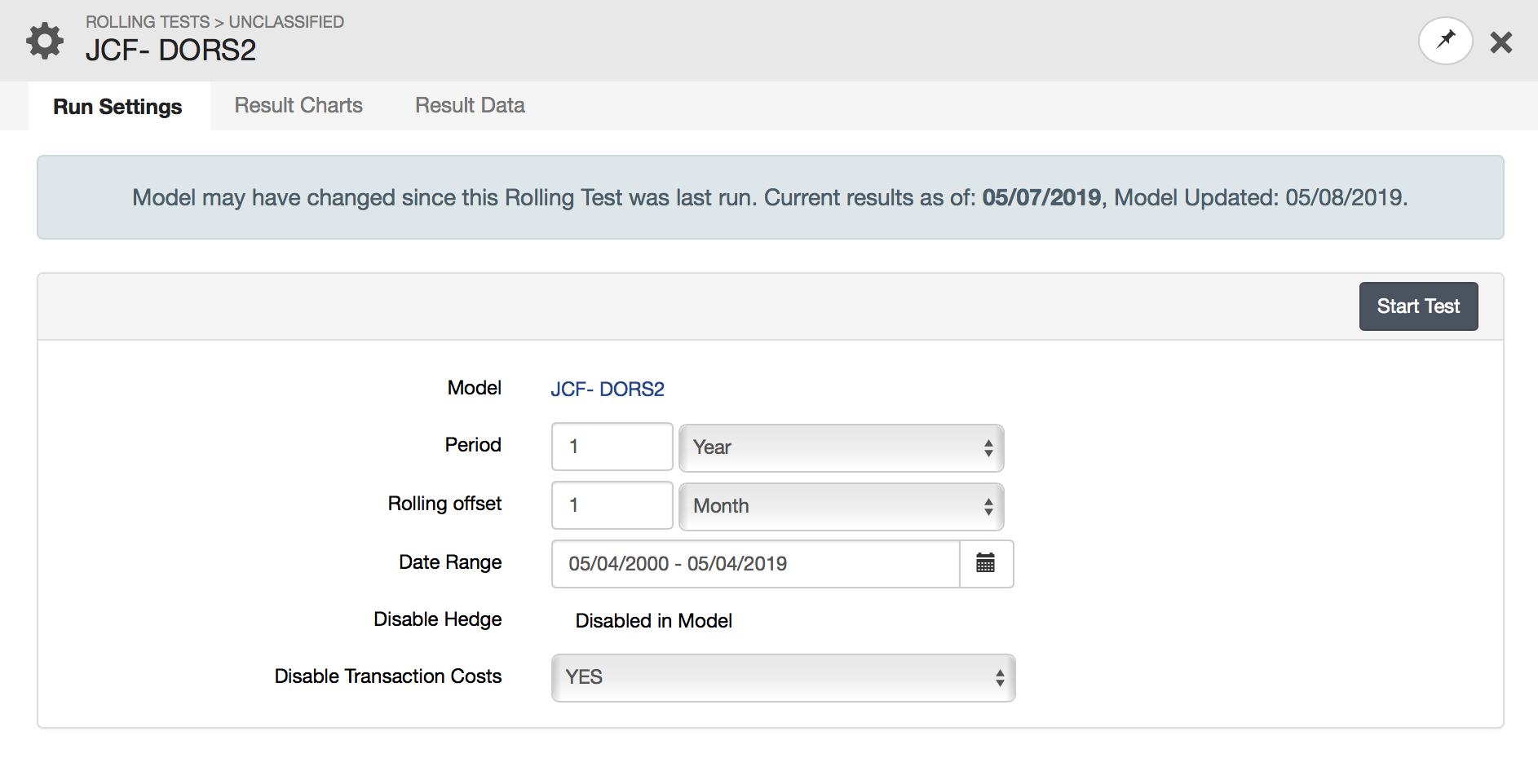

Use one year periods with one week offset. This will give you almost 1000 different simulations from 1999 to present, each one year long and each starting one week after the previous one.

The rolling test in the Screens was new to me, so I took a look. From what I see, it’s not quite the same thing as the portfolio simulation as it doesn’t execute buy and sell rules, but creates the portfolio with the top-ranking stocks then holds these for the specified period. The period should therefore match what you have specified as the rebalanace frequency (26 weeks).

Therefore I’d suggest to assess rolling performance, either view the performance graphs on a log scale and see where the lines are diverging (indicating outperformance). Or better still, download the simulation results and plot Total.Equity/Benchmark. Whenever this line is increasing you are outperforming the benchmark.

Smaug…you are right. All this time I assumed that it executed the sell rules. But you are correct - it just buys and holds. Shoot! How did I miss that?

It is still useful…particularly if you sync up the holding period to your rebalance period. That way you find out if there is a lot of variance based on your start date. There are 26 different starting points and you could always just run your master simulation 26 times by nudging it forward one week to compare the differences. If all are within a reasonable range - great. But if 2 out of 26 are great and 24 are bad - I would look at variables that are curve-fit.

I didn’t read any docs - I’m just going by what information is entered. I did not see any space for buy and sell rules, just a screen, ranking system and the number of stocks to hold.

Both screens and simulations have rolling tests available. I like to run a rolling test on any seriously considered model that rebalances or reconstitutes on anything more than a weekly basis, with and without any timing rules.

I have assumed that rolling test starts should be offset by one week and the holding period should be one or more rebalancing / reconstituting periods. My goal is to be certain that the rules hold up regardless of when the model begins.