Some heuristic assumptions I use about the distribution of the data include:

Longitudinal/cross-sectional Prices: lognormal

Longitudinal/cross-sectional Log returns: normal

Longitudinal earnings: skew-normal

Longitudinal revenues: lognormal

Ratio distributions of traditional value ratios (e.g., P/E, P/S) are generally approximated with inverse Gaussian distributions. I believe yields (e.g., S/P, E/P) can be loosely defined by Cauchy distributions.

These assumptions convey how the data behaves in terms of expectations, extremes, asymptotes, and undefined values.

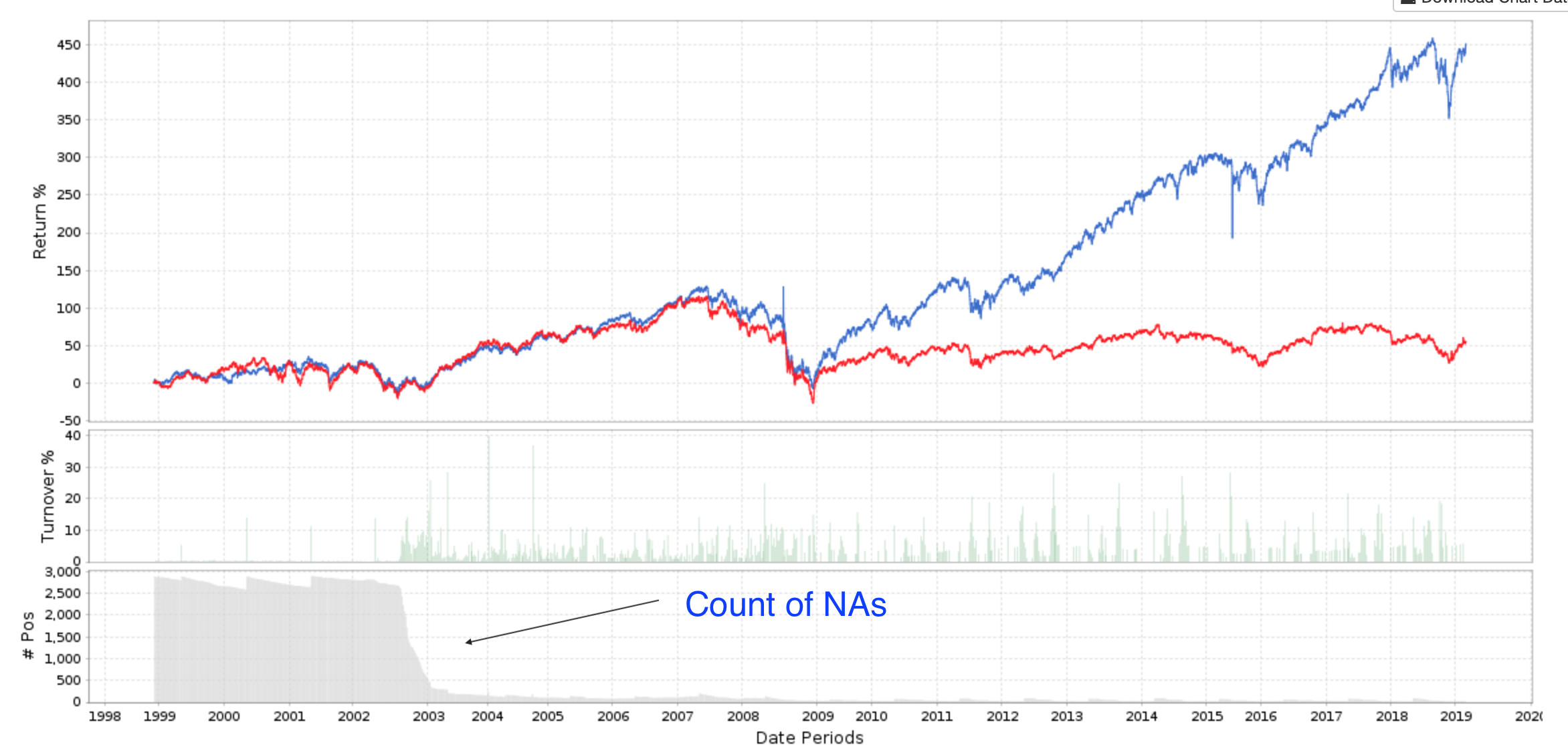

They do not say anything about NA or Null value handling

For the error handling discussion, I think you might benefit from spending some time in the CompuStat documentation. Most schools with business programs will provide access.

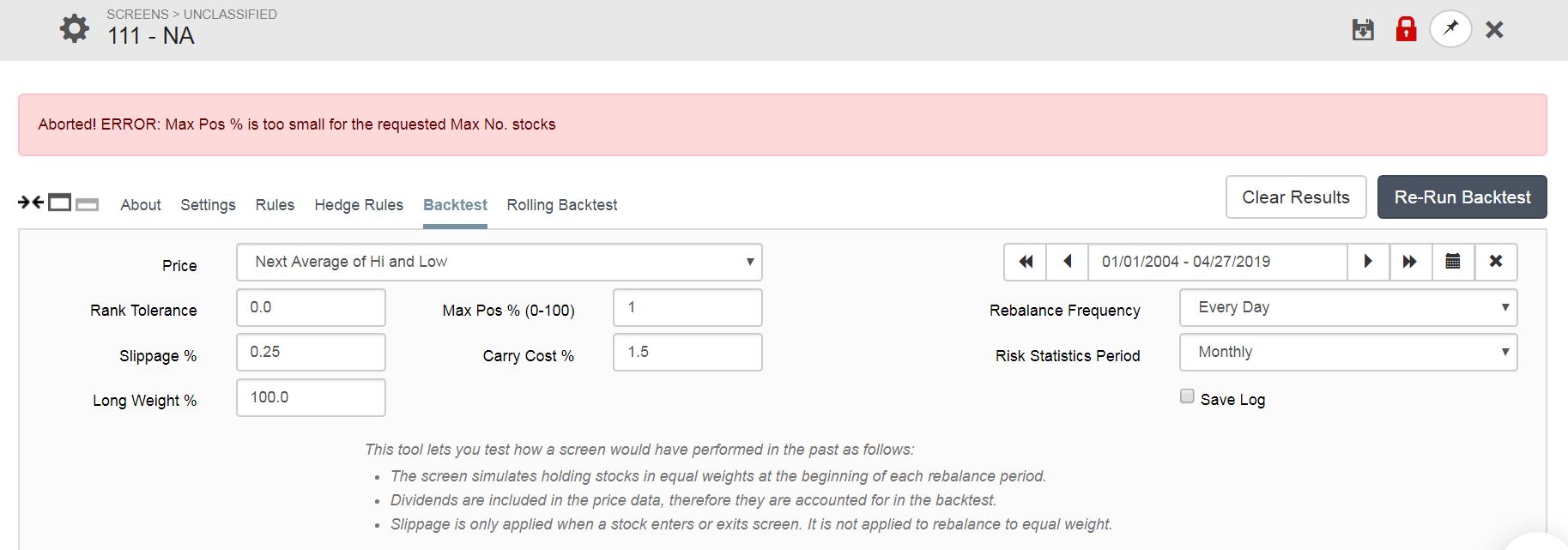

Once mastering CompuStat’s core logic, it gets a little trickier in P123. P123 is doing some additional interpolation of the data. This facilitates its use, but makes it more difficult to unwind the presentation of the data. Moreover, P123’s core logic relies on matching/manipulating based on dates; we are limited in how we can natively interact with dates through the front end.

Anyway, once I reached this point, the reason for P123’s back-end logic of falling back, keeping NA, and date-period matching made much more sense.