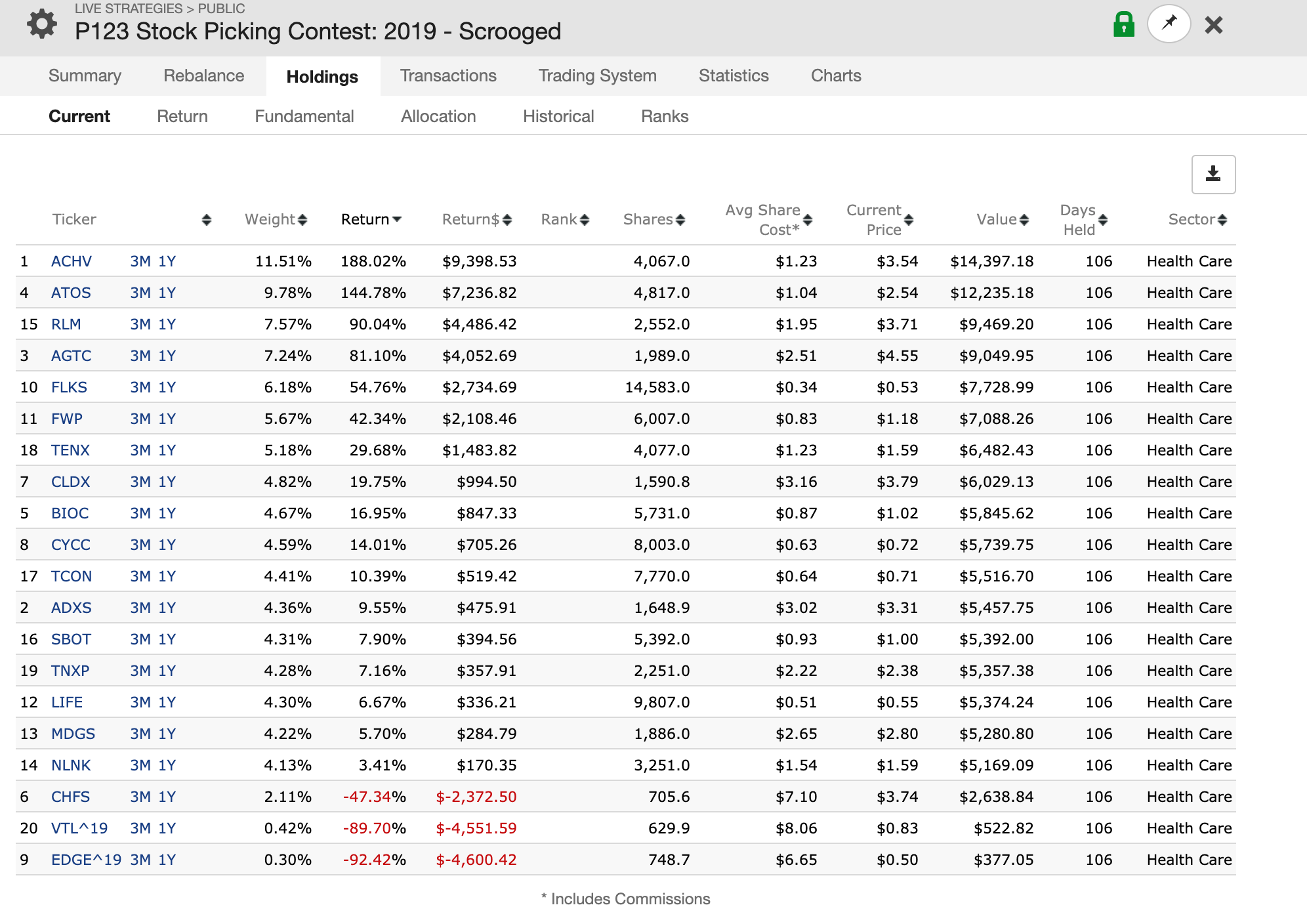

I have these two tickers in a Live Strategy. In particular the 2019 public stock picking contest. They are showing -89-95% returns when in fact the returns are quite positive.

edge^19

vtl^19

vtl should be roughly plus 297%

and edge plus 40%. At least that is what the backtest through the screener reports.

Both edge^19 vtl^19 did a reverse split and name change. EDGE^19 became PDS Biotech PDSB, VTL^19 became Immunic IMUX. Compustat created two new companies. Furthermore Compustat records the reverse splits after the stock price history ends.

I think the screener is more “correct” because it’s applying the splits even though they happen after the prices end.

We’ll report to Compustat to see why they did it this way.

Obviously we want to try to replicate what would happen in a real $ account. In a real account your old shares would have been replaced by the new shares whilst undergoing a reverse split.

However to properly handle the many flavors of mergers , reverse mergers, etc, is a big undertaking and we do not have the proper data, so it’s something we will not do soon. This is why we recommend selling before a major corporate action which works well for simulations as well as live strategies.

In this case the problem is the split in no-man’s land (in the future of a price series that died). Compustat will leave it as is , so we need a work-around/fixes.

To fix your problem can you sell the two stocks for a total of : last price * #shares pre-split

To fix this problem in the future we will not process splits if they occur after a price series has stopped.

I realize this was hairy and I hit you with it almost the day it happened.

It seems like, though, that compustat would not end a price series of an ended ticker with a price that implies that the stock went down (in this case over the prior 90 days or so) when in fact it went up (all merger, split, adjusted in). I mean why not just end the ticker price series with the last traded price, or the takeout price in the case of a merger? Perhaps, CapIQ fixes this sort of thing when the legal dust of a merger settles. If Compustat did it this way, then P123 could get the data on merger terms and continue the pick in the live port (always selecting for shares in the acquirer). This would just be another feather in your cap as the best backtest engine.

I guess my question wasn’t so much about CapIQ though, but why the screener vs the live port are different. It seems they should each, at least, have the same handling, even if this hairy reverse merger might reflect a CapIQ error. I’ll do some math and Edgar reading and figure out what the screener and the live port should say… exactly.

As far as changing the sales in the live port - I don’t think my compatriots in the 2019 stock competition would smile to kindly on me entering magical sales prices

Best,

Ebenezer

The screener operates with fully adjusted price series for divs & splits to make things simple, and reverses out future splits for whatever point in time it’s processing.

The screener is ignoring the splits since they cannot be applied to the price series

In strategies ,live & sims, the splits are applied to the holdings

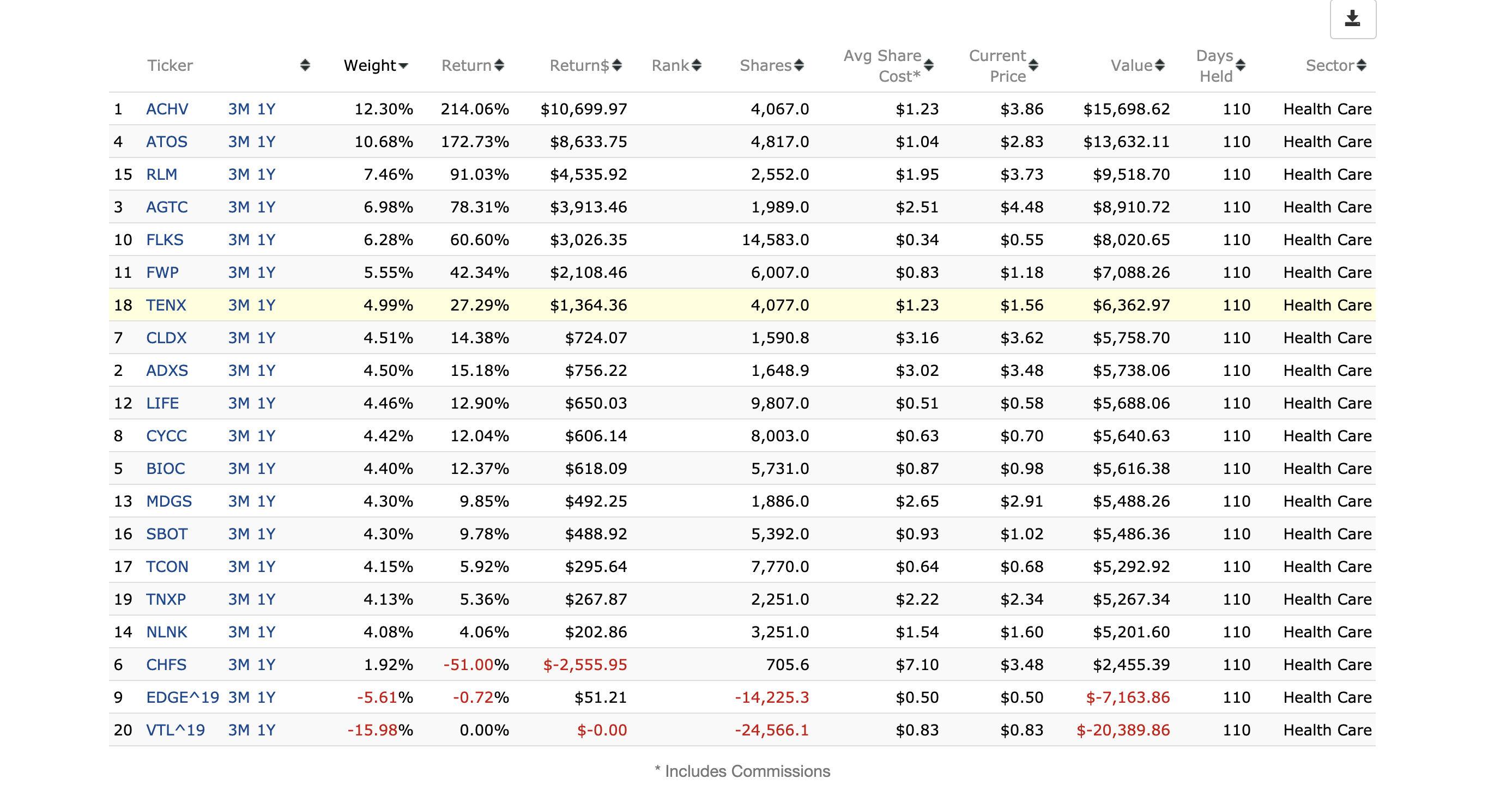

Okay. Interesting things happened.

Entering a manual transaction with: “shares pre split * last price” didn’t do the trick because it created a short position. See attached.

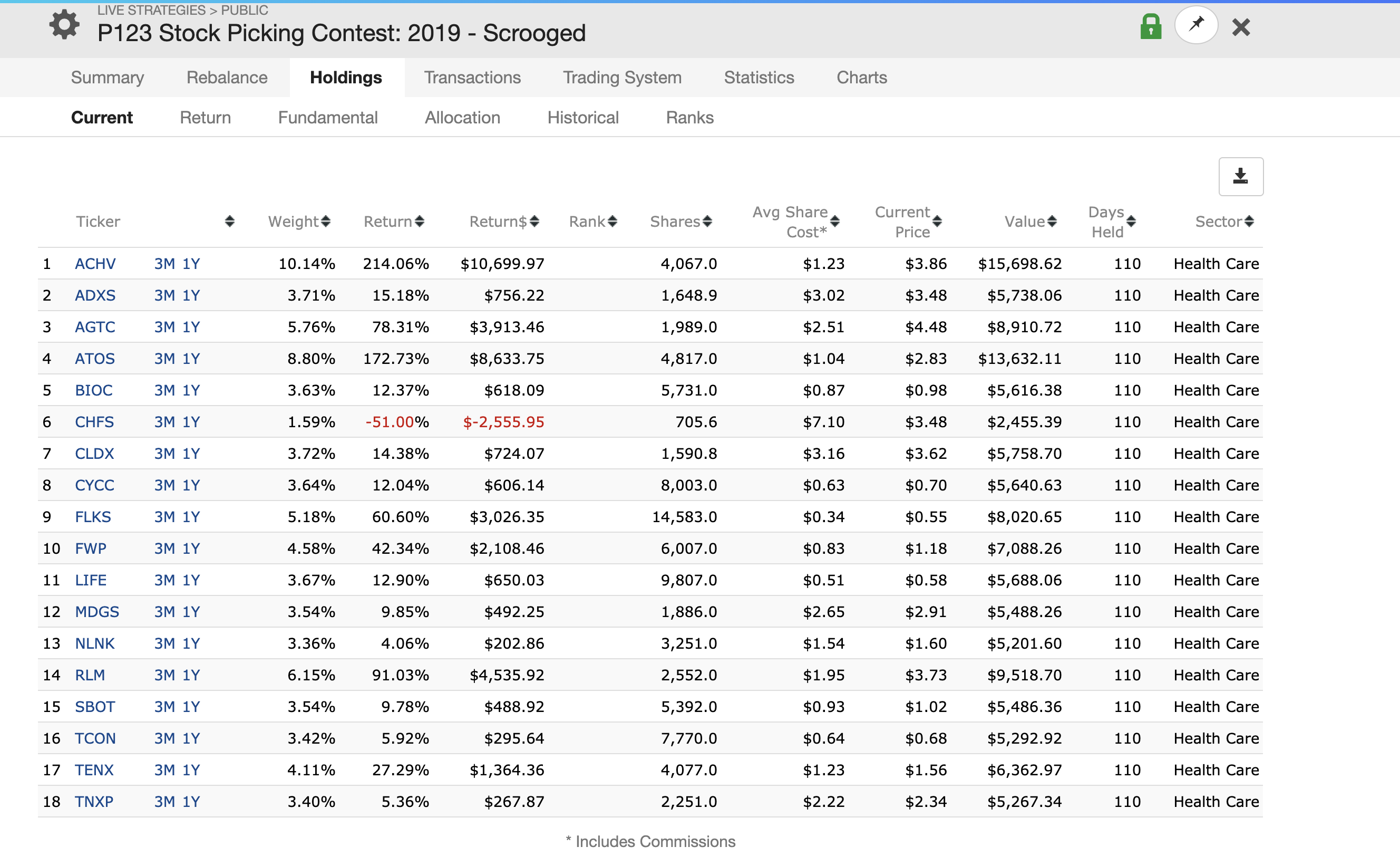

Entering a manual transaction with: shares post split in live port * last price from last day ticker existed in screener seems to have worked better. See second attached.

I’ll check back to see how the manual transaction changes the live port chart and return calculations. I imagine it will suddenly jump up while the risk/draw down statistics will remain compromised.