One of the issue with designing model as individual investor; most of us working for few months and give-up.

If the model did not works; we don’t have find time to review periodically and learn knowledge and keep improve on;

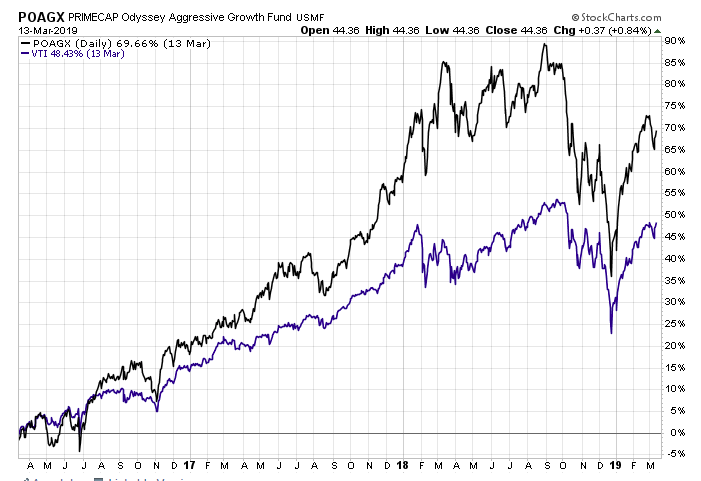

where as POAGX mutual fund manager; they are making living out of their model/idea/mutual funds; it is managed by team of top class MBAs (Standford, Hardvard) with decades of full-time experience. their full-time job is find good investment and keep investing; another team get funds to invest.

POAGX initial years; it is under-performed bench mark; now it is doing great.

Thinking of how to improve my designer model similar to POAGX.

Most of my designer model outperform the bench mark initial 3 to 6 months nicely. then it under perform.

Mutual funds holding report every 3 months their current holdings.

My model has nice buy rules; those rule may no longer valid for already held stocks in current holdings in the model;

I am planning to revise all of my model;

every 3 months compulsorily sell all the current holdings and buy new.

so, we are assured all the current holdings satisfy my buy rules every quarter similar to mutual funds quarterly health check.

include some new find knowledge in ranks and buy rules over last 18 months.

I also planning for 5 stocks version of SP500 model.

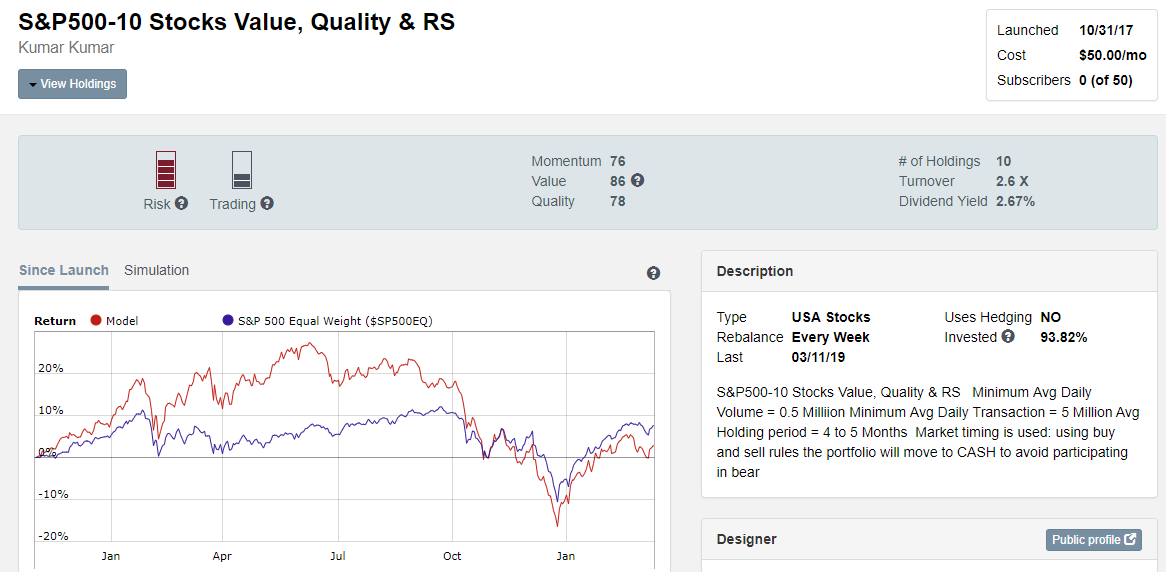

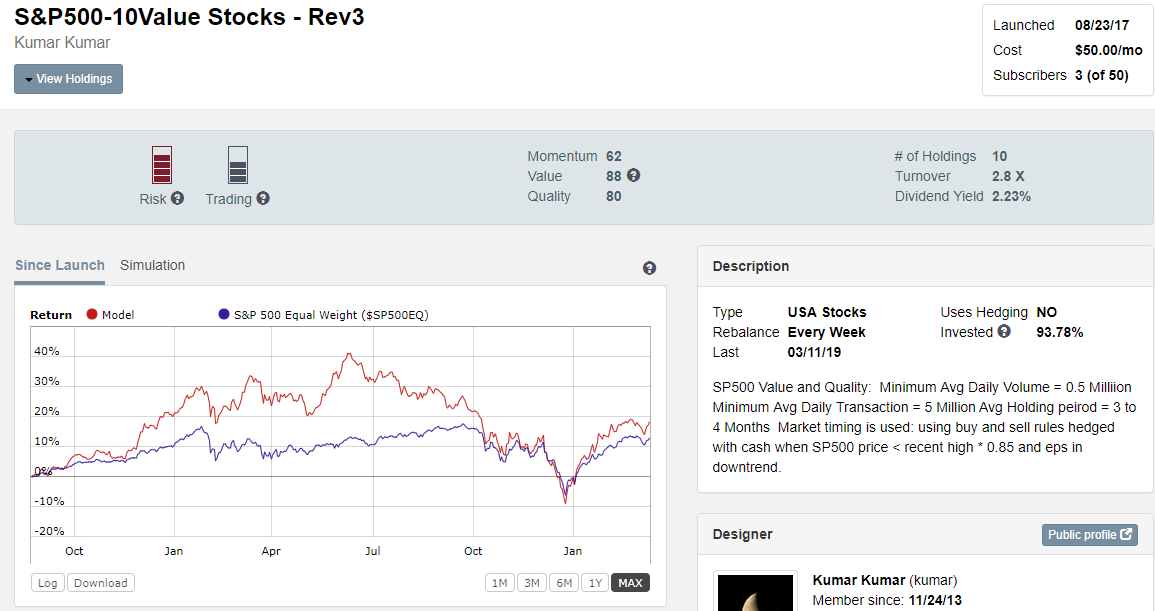

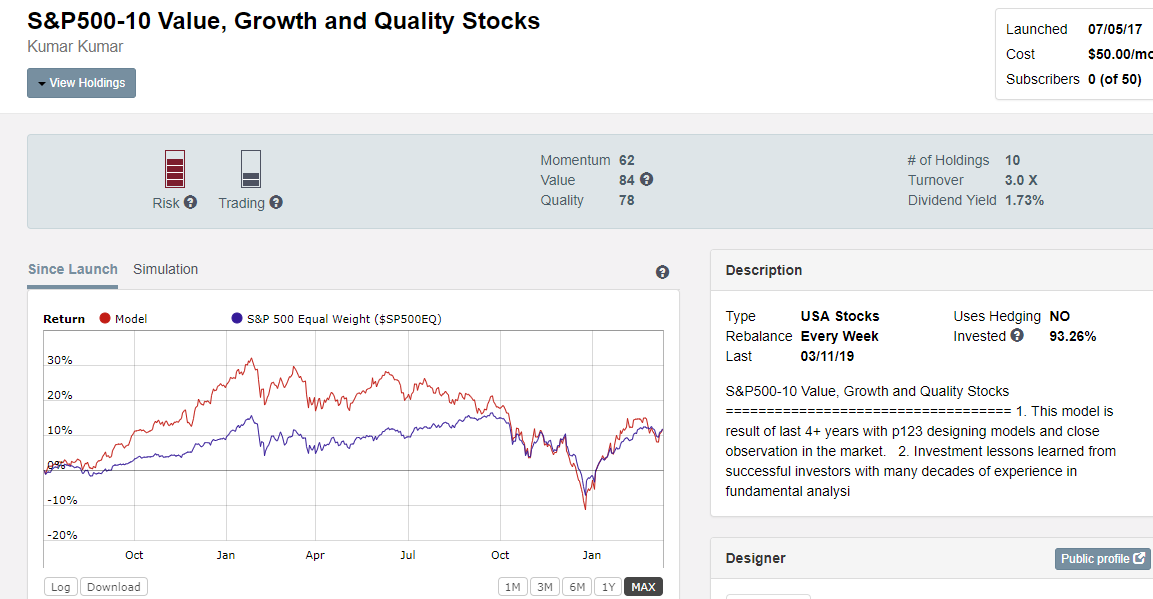

Any suggestion/feed back to improve my SP500 models will be appreciated.

kumar, While it’s difficult to say much without knowing what is going into the model, here are some ideas based on looking at the equity curve.

I bet alot of models underperformed from October to December. This might be perfectly normal and expected behavior for a model that is fine over the longer term.

In my experience, smaller cap in particular outperformed well up to about August and then started diving from Sept-Dec. If your model leans toward smaller capitalizations then this type of equity curve might be expected.

10 holdings is likely going to have a higher std deviation and beta than more holding. I’d suspect moving to 15 or maybe 20 holdings (I suspect 15 holdings might be enough to see a difference) might help with volatility during draw down periods.

You may be doing this already, but if you want to reduce volatility you can add factors that reward low volatility in equity selection. This might include “Beta” as a factor and/or some type of “low price volatility” factor that rewards lower price variance.

You may already be doing this also, but you can reward stability in the financial statements, like sales stability or earnings stability. More predictable companies will tend to hold up better during drawdowns.

Some sectors will usually hold up better during drawdowns than others.

There’s always a tradeoff when rewarding stability in the models, however. Your overall model raw performance may go down even if volatility adjusted performance (sharpe ratio) goes up. You might see better sharpe ratios, but lower returns. In the end this is a risk/reward decision the designer has to make. I don’t like big drawdowns, so try to do things that cushion them.

In the context of a book, mixing an allocation of a low risk portfolio with a higher risk portfolio might be better than a single all purpose model that targets highest total returns regardless of volatility. I’m still working out how I deal with this, but I’ve personally added a separate allocation to lower risk items like preferred shares, a little bit of bonds, and utilities to my overall mix to help offset drawdowns in the more aggressive parts of the portfolio. This to me seems to be a more effective way of balancing the risk/reward than trying to make it all happen inside of a single model. I expect that my higher return models will likely struggle during periods of market drawdown.

Anyhow, these are just random thoughts based on my limited experience. And I’m still working at it. But hopefully maybe some ideas are of help.

Thank you for your suggestion and feedback. I will take note of your points.

I also want to observe quarterly reporting of top mutual funds current holdings; to learn some more fundamental factors from their new position in the last quarter and sold position in the last quarter. believe, that is x-ray vision to understand their ideas.

it will take few more months time; definitely i will work on this challenge.

“build model to perform better than POAGX in out of sample.”

if any one interested can join in this competition; it will benefit you as individual investor in long run.