Hi all!!

I would like to comment something with you and get some feedback because I’m not sure about what to think.

Recently I tried another plattaform, very similar to Portofio 123, but little bit simplier. The staff from the plattaform send some systems to the users. One I recibed shows a very good performance, around 30% a year, then I translated that system to the Portfolio123 just to check if the results are the same, and… surprise, the sim goes to ruin in just few years.

*I’m not going to write down here the name of that platform, if anyone is interested ask me by private email and I will send you the adress.

I asked to the guys who run the plattaform about that difference in results. And they answer the following:

“The key difference I found where the two systems are different is that P123 generally takes a standard universe of all stocks, ranks it and then applies your buy rules, whereas “X” applies the universe rules, then ranks, then applies any buy rules. This is a much bigger difference than it sounds, as ranks act very differently with different numbers of securities in a universe. If you look at your Value strategy and click the Rank Screener option you can see that it includes just 922 securities in your list, whereas P123 will be ranking on approximately 4,500. Even a difference of 10-20 strategies at that level can have a significant effect on which companies appear at which rank.

The second key area I found was that the data between the two systems is slightly different. Both Thomson Reuters (who I think P123 use) and Factset (our providers) normalize certain data points to their own definitions – this includes often used numbers such as EPS and Cash flows. I have gone through this with Factset a number of times and what they do makes sense, as I’m sure Reuters do – they are normalizing the data for us so that we can compare companies without some of the “financial games” that CFOs like to play getting in the way. This again makes comparing the same system on the two platforms very problematic (I had about 10 that I liked on P123, and only a couple were even partly successful on IE). Our view is that as long as these changes are applied consistently then we’re happy to use them. As an interesting note, we found that Factset were generally a lot closer to the SEC submissions than Reuters were, especially with smaller companies.”

In resume: I am not comparing identical processes to filtering the stocks and therefor will not get similar results.

I understand the point, but if we are talking about the real world, I think the same system must retorn the same results in the backtester, if not… how can I trust in that system? What is the better way to proceed? Should I trust in the sim one or in the sim two? Where should I place my money?

Well, your turn.: What do you think about that?

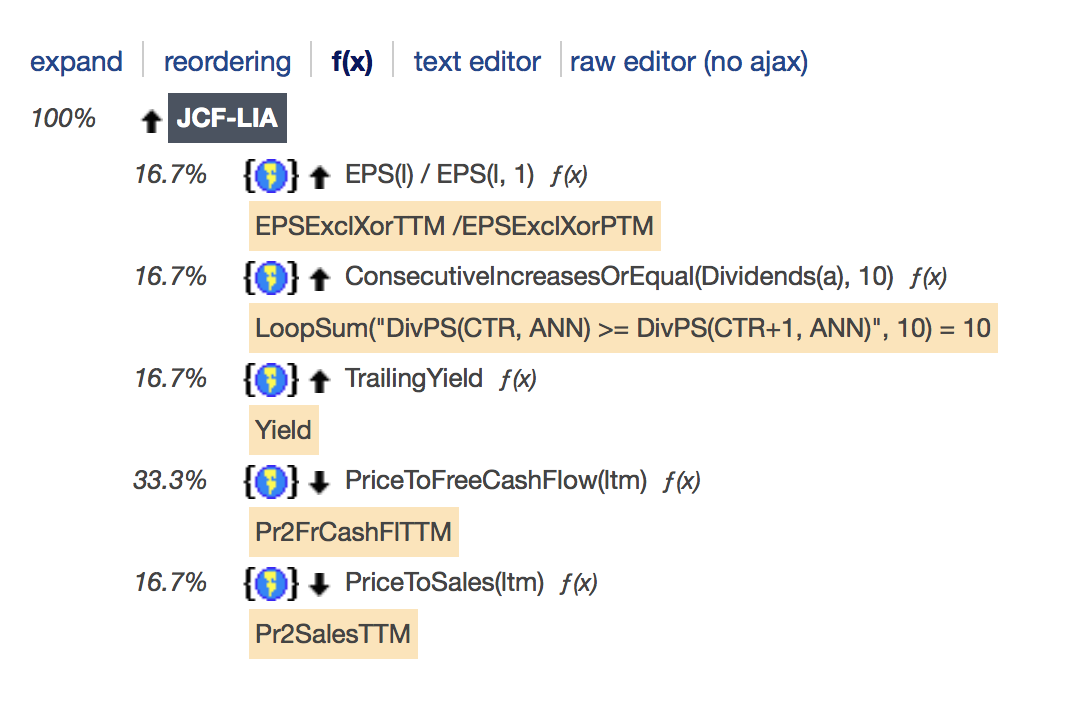

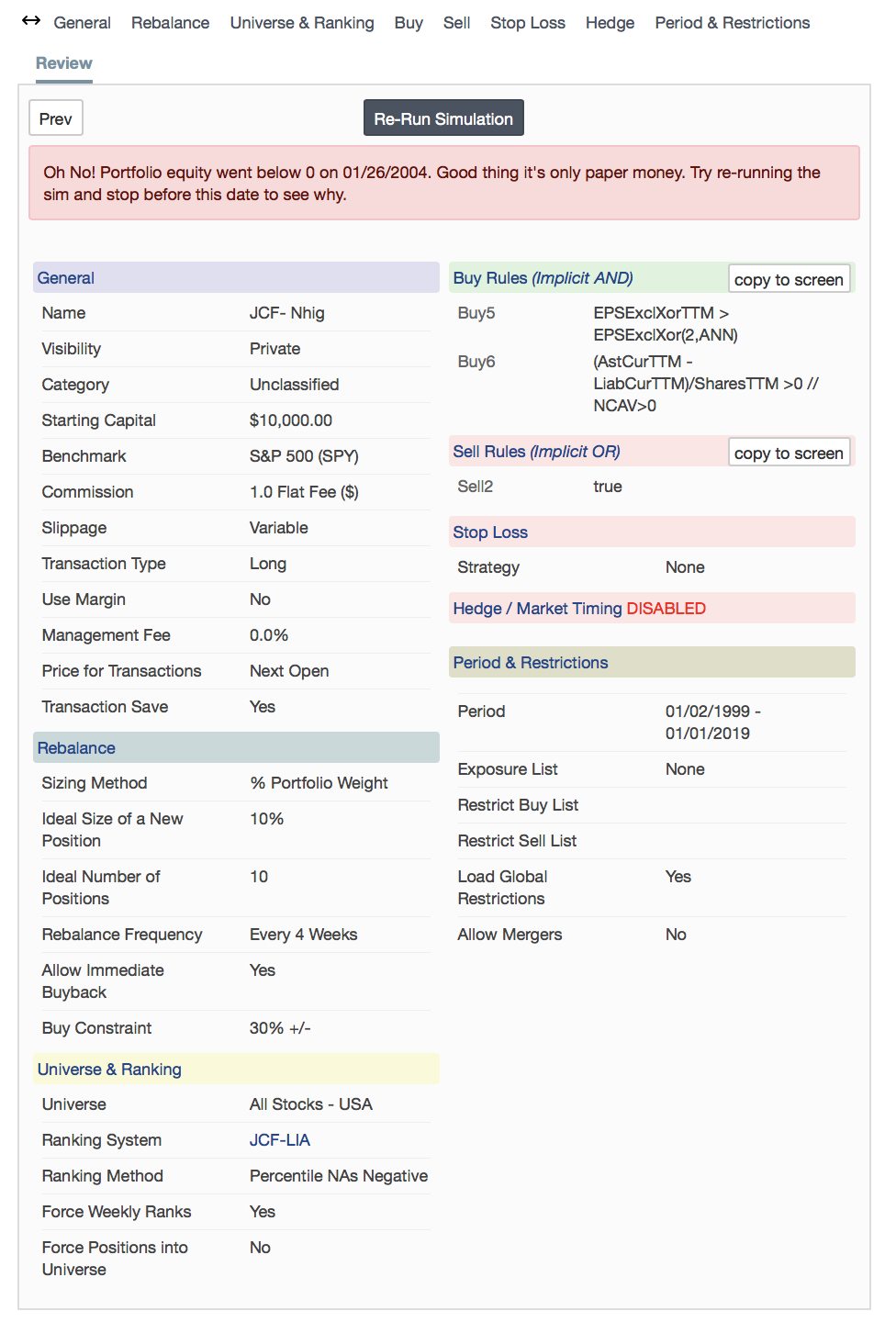

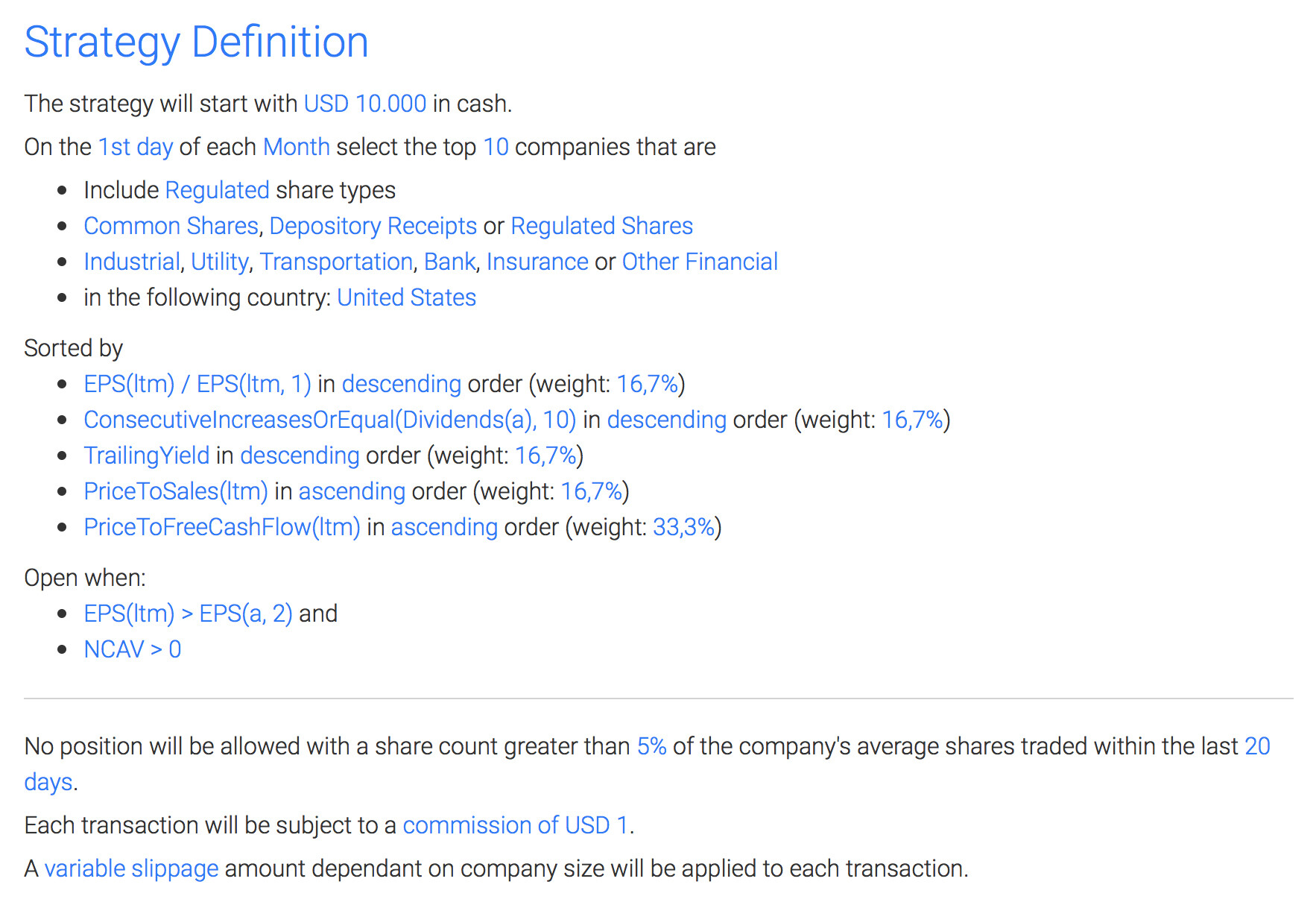

I attached few screen captures from the original system from the web x and what I translated to P123.