Hi all,

I have been worried about Slippage and Market impact. But a complete look at trading costs looks at more than slippage and market impact.

I have been reading “The Science of Algorithmic Trading and Portfolio Management” by Robert Kissel Ph.D.

If I am worried just about slippage I should consider a VWAP order according to the book. But can I do more?

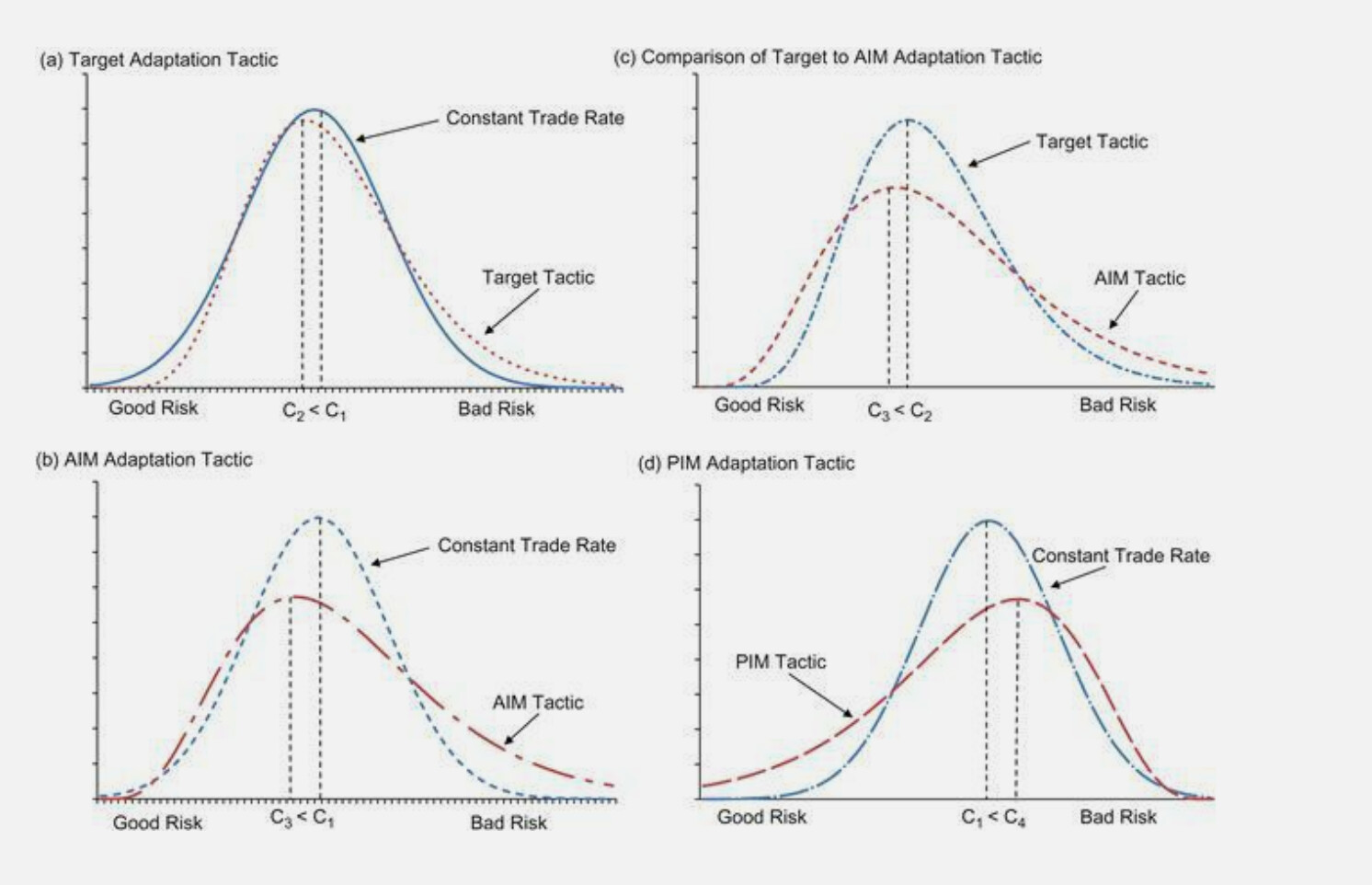

These graphs from the book show that I probably want to increase the rate of purchase when the stock price goes down during the day and slow the rate of purchase as the price goes up (for buy orders). This strategy of slowing the purchases as the price increases has risks however. If the price keep going up while I slow my purchases I end having a lot stocks to buy (with a high price) at the end of the day. I can stop buying stocks at this expensive level but that leads to an opportunity cost or maybe I just wish I hadn’t used this algorithm in the first place.

Here are several strategies that adjust the “trade rate” to the market conditions. “AIM” (the one I am most interested in) leads to an improvement in price (C3 < C1 first image) while PIM prevents the expensive outliers by speeding up purchases as prices rise. But AIM leads to outliers and a skewed distribution—those stocks whose price keep rising during the day with a slowed purchase rate (with the algorithm completing the purchases at the higher price).

And the slippage and market impact will be a little higher than a simple VWAP order. And there will be more commissions. Maybe this is just a little too cute: more worries than it is worth and actually causing problems much of the time.

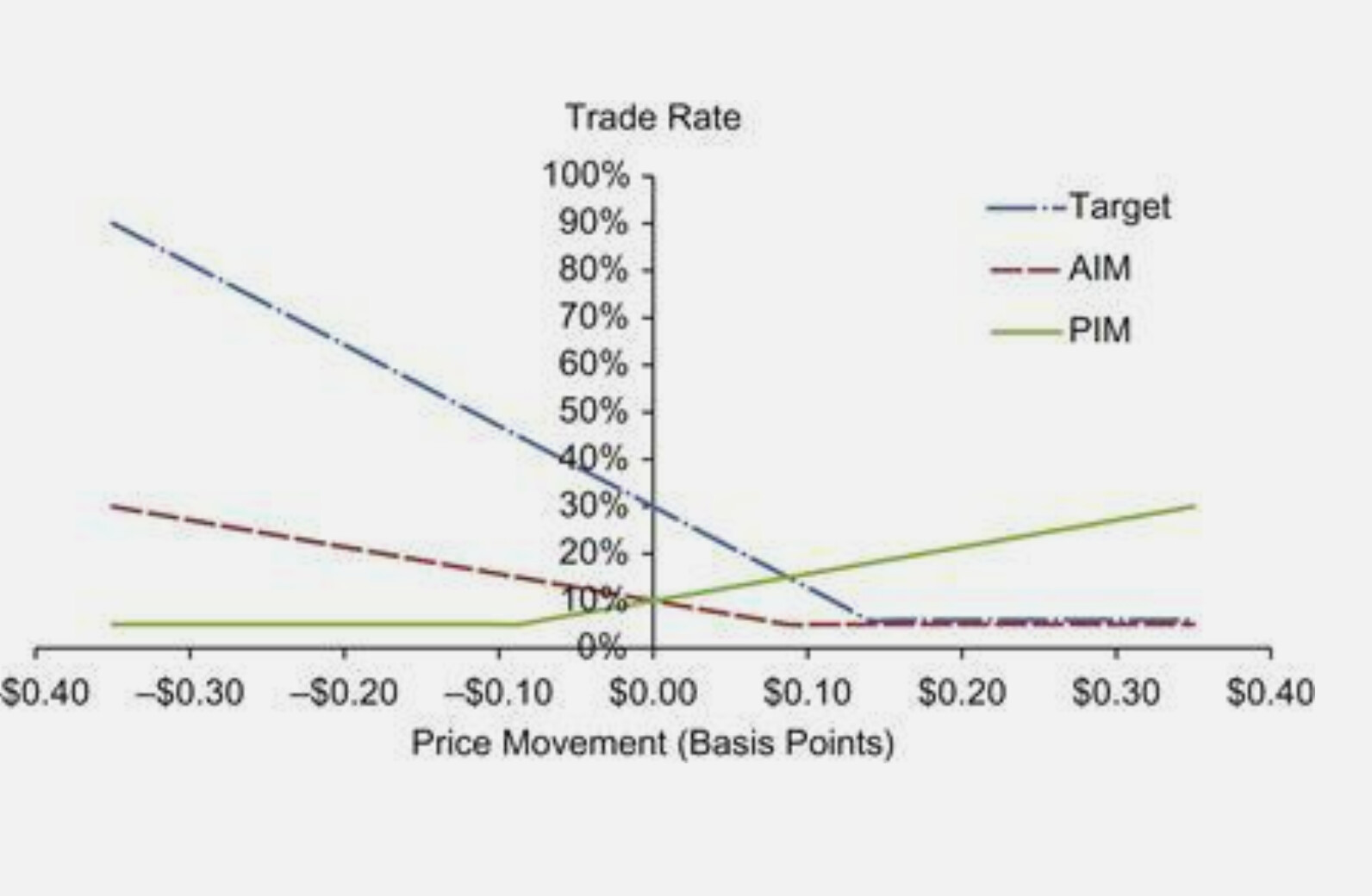

I cannot use some of the algorithms in the book. But I could use a VWAP order along with one or more Limit Percent of Volume orders that increases the rate of purchases when the price is more favorable and slow the purchases when the price is high (buy orders): coming closer to the algorithm (trade rate) in the second image. You could probably think of some other algorithms including placing some “plain vanilla” limit orders at favorable prices.

Worth the trouble? Worth the risk of those outliers and skew? Would it even work?

I have not tried to calculate the magnitude of the improvement yet. I was not actually sure that this type of algorithm could improve the expected (average) fill price until I read the book. But I will probably take some simple steps to increase the trading rate when prices are favorable-even if it is as simple a cancelling an order and changing it to a faster or slower purchase rate as prices change during the day. Then again, maybe it is more trouble than it is worth.

Ideas welcome.

-Jim