Same ~dozen factors:

2009-2014 - 41% return

2014-today -1% AR

value.pdf (225 KB)

As a baseline, the Russell 3000 universe < $1M mktcap gained 25% a year from 2009-14, and 6% a year from 2014-now.

So, what’s up size?

P123 backbone is small cap and value stocks.

Many experts in P123 enjoy the small cap value stock ride from 2004-2013. Now those community models looks not working.

Big companies buying successful small companies.

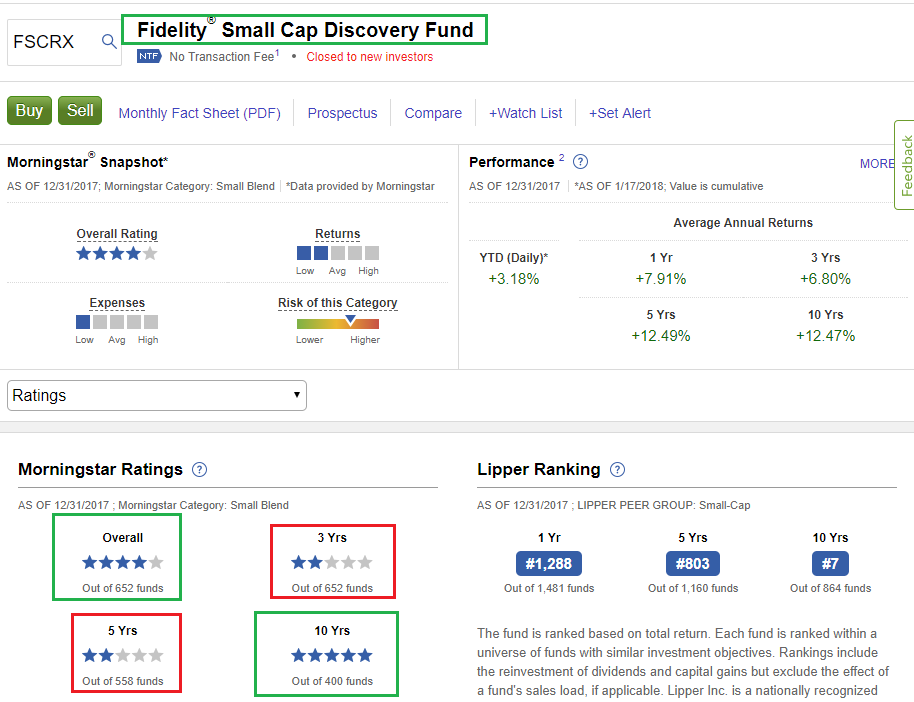

small cap discovery fidelity fund under perform sp500 for last 4 years in a row.

Jan 2016 was strong bearish for small cap Russel 2000, TNA was more than 50% down from 2014 all time high.

Smallcap value still in recovery phase,

Jesse Livermore said nothing new in the stock market, if market start to flow money in smallcap, P123 user will be happy again for 10 more years as did 2004-2013.

![]() We have to be around with P123 when market favors smallcap value stock again.

We have to be around with P123 when market favors smallcap value stock again. ![]()

Need to have patience market rotate now large cap growth stocks are in song, so IBD50 is.

Thanks

Kumar ![]()

90% success in investment depends on asset allocation.

Thanks

Kumar

Could also be that the market is becoming more efficient due to proliferation of quality data…

Fidelity SmallCap fund 10 years avg 12.47 pct and 3 years avg return 6.8 pct -

If fidelity full-time knowledgeable manager (smallcap xpert) can’t do, others hard to do in smallcap arena.

For last 3 years, the market is not home ground for smallcap and value stocks.

Thanks

Kumar

Aargh. This all seems like absolute nonsense to me. Value disappearing? Small caps not doing well? How have I maintained a CAGR of over 50% for the last 25 months by investing in low-priced small caps and microcaps?

Here’s what’s actually going on: absolutely nothing has changed.

If you define “value” as low price-to-book or low P/E, you’re defining value wrong. Read Graham and Dodd–even back in 1934 they knew that low price-to-book and low P/E were not enough. The holy grail of value investing is DCF analysis, and it has been for over fifty years. If you define value accordingly, it works just as well now as it always has. Ditto if you combine comparative equity-based valuation measures with enterprise-value-based measures. All it takes is a little sophistication.

The difference between small caps and large caps is very simple, and consists of two things. First, large caps are more stable, they’re safer, they’re solid, they don’t jump around like mad. Second, almost all sensibly built (i.e. top decile a lot better than bottom decile) ranking systems based on fundamentals (value and quality) will perform better (i.e. larger difference between top and bottom decile) in a small-cap or microcap universe than in a large-cap universe. Just compare the performance of the QVG ranking system between the S&P 500 and the Russell 2000.

I know I’m committing heresy here. But all these factor-indexed ETFs are based on idiocy. I can’t understand why anyone would want to invest in, say, SLYV (S&P 600 small-cap value). This is an ETF that rebalances annually (exactly the wrong approach for small-cap value, though it makes sense for large-cap value), defines small-cap as less than $2.1 billion (thus including a huge number of mid-caps), and defines “value” by looking only at equity measures and ignoring all enterprise-value-based measures, as well as ignoring all QUALITY measures. That’s not what value investing is. Well, I guess it is now, but it never was until the rise of all these senseless indexes. Value investing involves serious consideration of a LOT of fundamentals, not just three common equity-based measures.

Sorry to lose my cool here, but there’s just so much nonsense out there. Small-cap value investing works, always has worked, and always will work. You just have to work extremely hard at it rather than relying on an index.

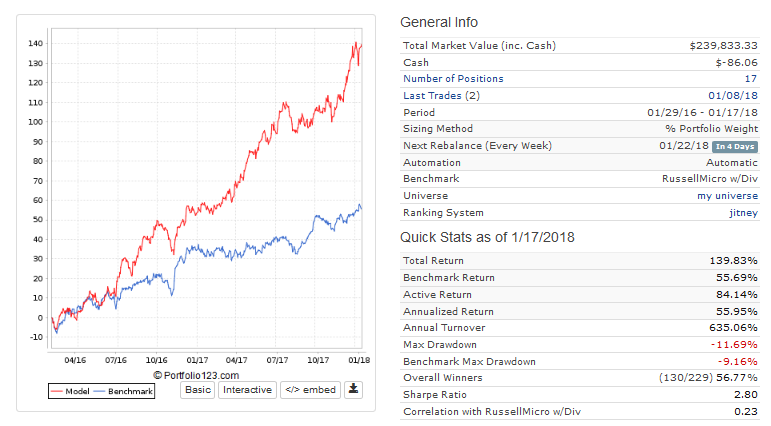

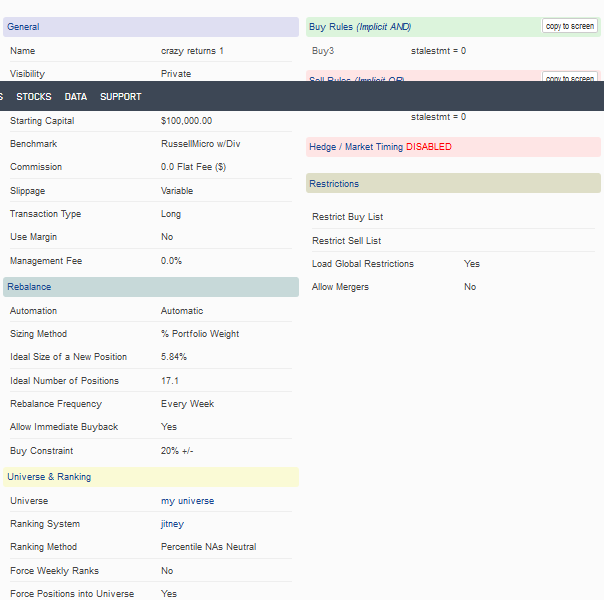

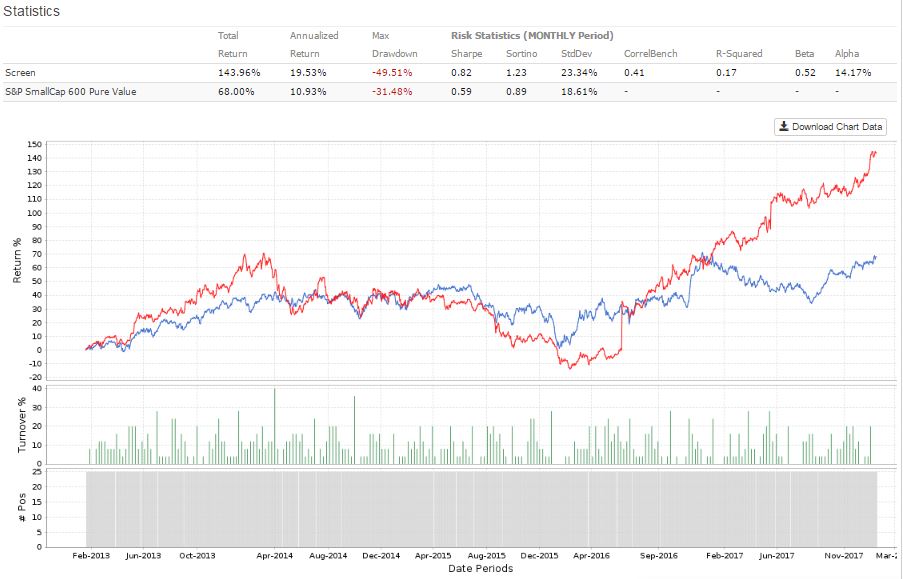

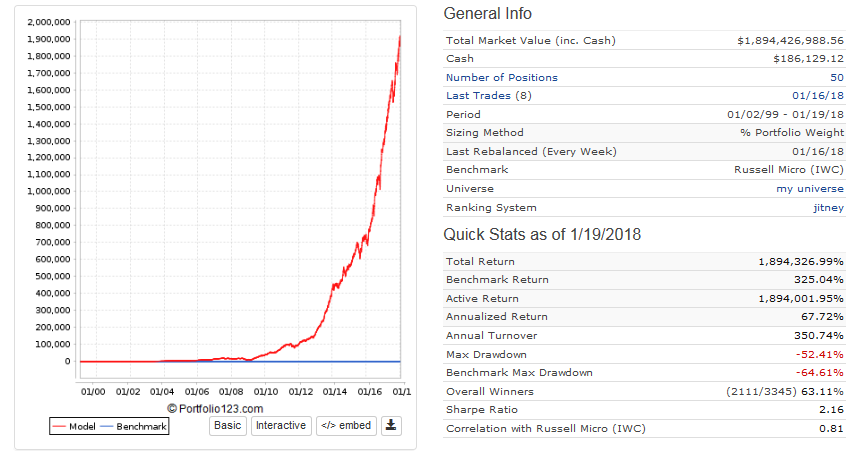

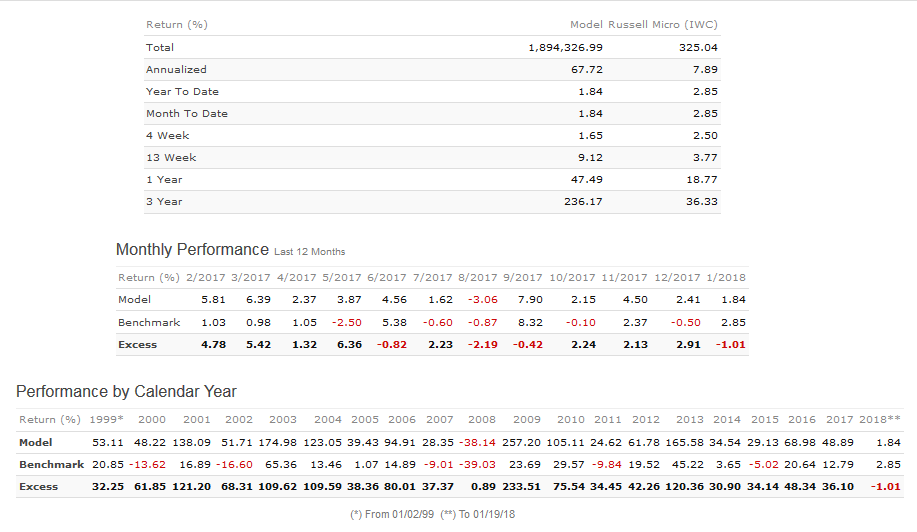

Just to prove my point here are screenshots from a microcap and small-cap value live port I started about two years ago. It has always used variable slippage and has never used margin; holdings have never been fewer than 15 stocks; and the main ranking factors have been related to value, quality, and growth.

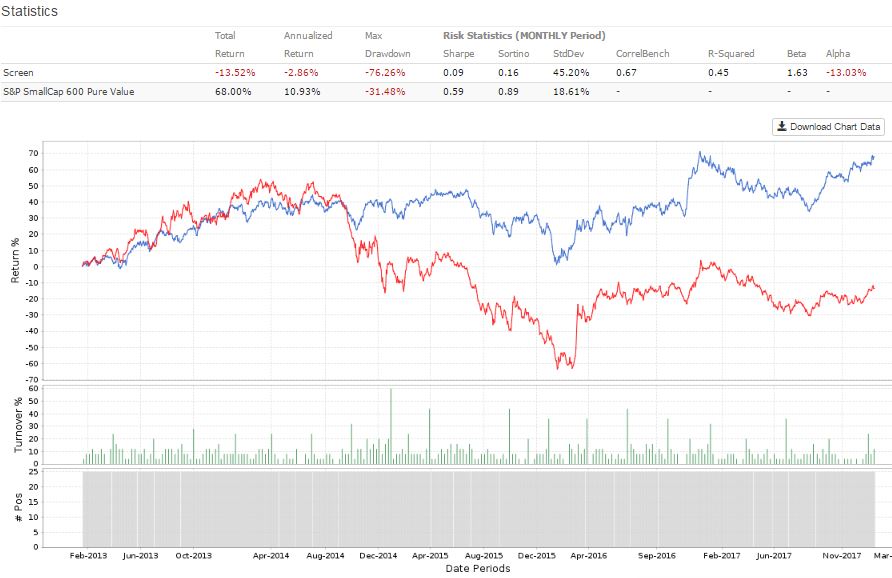

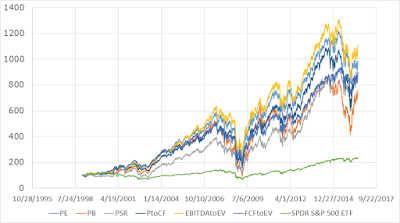

I agree with yuval. The problem is how you’re defining “value.” Since price to book was singled out by Fama/French, it’s been picked up by Russell and others as the way to define value and is now tracked by 100s of billions in “value” ETFs. The tilt toward price to book eroded its alpha (see orange line).

I ran two simple screens, one with price to book and one with another value factor.

More great reading on this topic by Pat O’Shaughnessy: price to book investor's field guide - Google Search

agree also with yuvaltaylor, my small cap value port is up 100% since 2016, though I have a 25% momentum weight on it too… (75% value)…

Yuval and Judgetrade,

You are good with microcap investing for your personnel account; with 20,000 to 300, 000 avg volume.

the volume ignored by institution and wealthy investors.

If your model is worthy to share to others; can you take the challenge and make make your model private model as designer model ?

your private model involves countless hours of hard work and only allowed for 1 person with limited capital. It is not example for others to follow, believe and execute.

(Private and MicroCap with low volume) Exceptions are not Example.

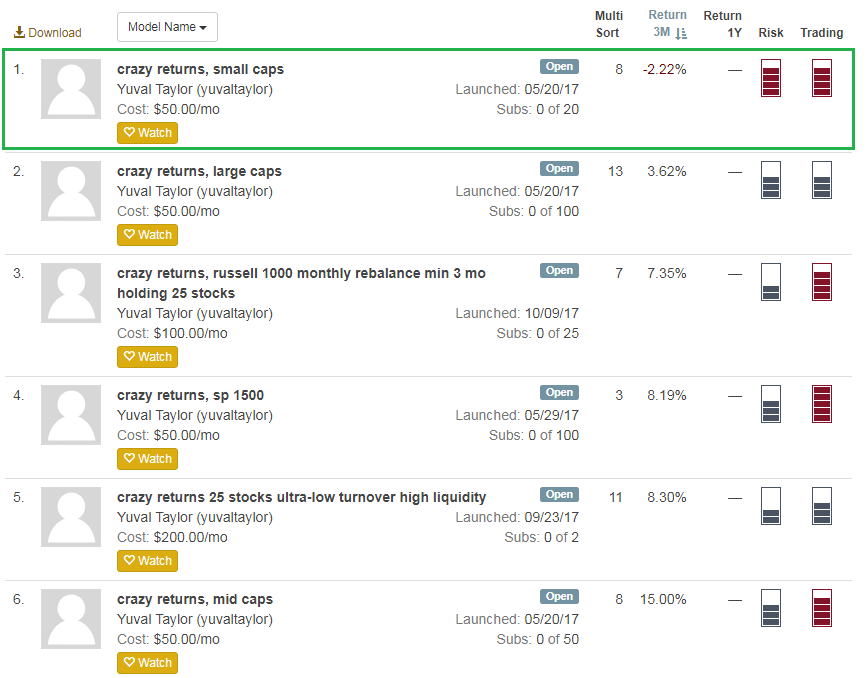

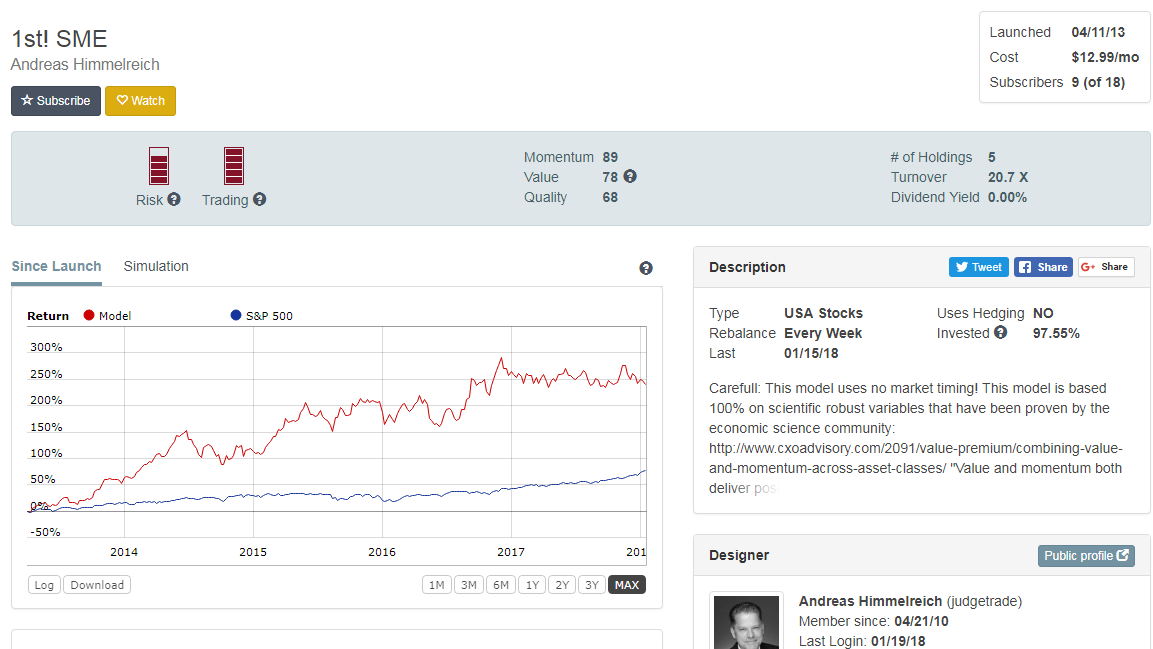

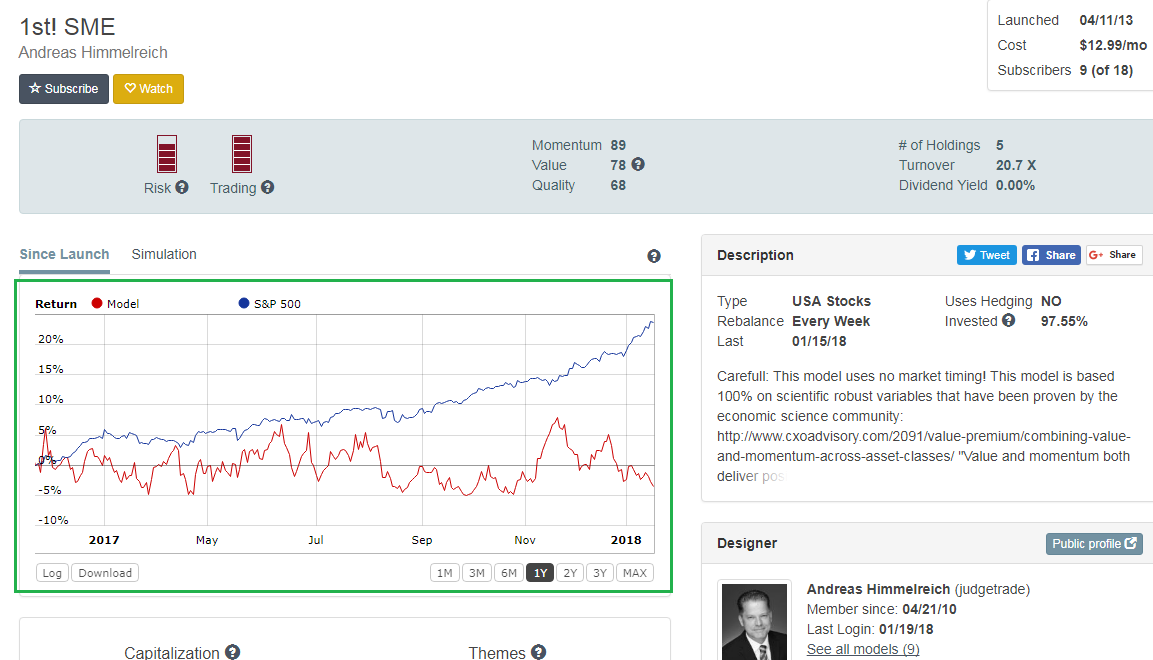

here, i am attaching your designer models for last 3 months performance(Yuval) and JudgeTrade’s very successful model turned to flat for last 1 year.

Here, I am happy about your success with P123, but more than 50% designer lost confident and left P123.

My message is for them; they have already put 90% of hard work to design the model; they came thru long way and given-up. need to put 10% hard work to become successful.

All of my deisgner model, initially was 60% win rate as others model; I have attended many AAII seminars and few successful investors seminar; now all of my model with 67% success rate, (10% improvement). my model has liquidity. What i have heard from successful investors;

the secret in investmet is, if you educate others; you can become better at your investment.

so, i kept all of my findings in my model. my best performing model become designer model. I am still in learning phase until i get 75% success rate model; (may take many years, but it is possible). ![]()

As both of you very successful in your private account and more honest on this forum,

The wind and the waves are always on the side of the ablest navigator (Yuval and JudgeTrade and very few successful p123 users).

believe you don’t mind posting screen shot of your model;

my message is p123 designers and users need to wait with patience, small cap days yet to come for average navigator.

Thanks

Kumar ![]()

Yuval,

I am curious as to what those results would look like with a 50 stock port. Is this something you can show a backtest for. While your realtime performance is impressive, a high performing 15 stock portfolio with an overall market tailwind is not really statistically significant. Congrats on the real world results, but I am skeptical of results going forward in the microcap space, if this market ever slows down.

Andreas’ real world performance with his 100 stock port and relatively low turnover is very interesting. It seems in reading his past posts, that the secret is in the buy and sell rules, as his robustness testing showed decent performance with very mediocre public ranking systems.

Kumar -

Because I sometimes buy as much as half of the average daily dollar volume of a stock, I’m not going to make my private model public. Imagine what would happen if someone else were to try to buy or sell $100,000 worth of a stock with an average daily dollar volume of $40,000. The price I’d pay would go soaring. It’s not worth the risk.

I admit my small-cap designer model has done very badly over the last three months. I’m pretty confident that in the long run it’ll outperform the market. It’s a very low-beta model, so maybe it underperforms when the stock market is moving sharply upward. That’s just a wild guess . . .

Below are screenshots of the same system but with fifty stocks.

Andreas’s performance is boosted by his use of margin. I think he’s a brilliant investor, but I’m doing something quite different: no margin, no buy or sell rules except rankpos, everything dependent on a ranking system that attempts to evaluate every stock as thoroughly as possible from as many different angles as I can come up with.

These are good, sensible statements.

Sometimes, I think Fama French did more damage than good by persuading a generation that factors, in isolation, have meaning. That’s not at all true and never has been true.

Yuval is absolutely right, for example, in what he says about value. As explained in the on-line course, ideal P/E is E/(R - G) where R is rate of return (on a company-specific basis, that’s driven by risk-quality) and growth. And the +/- signs tell you that as G rises, so too, does fair P/E, and as R falls, so, too, does fair P/e. So depending on how E/(R - G) falls out, a high P/E stock might, and often is, a better value than a low P/E dog (the well known “value trap”).

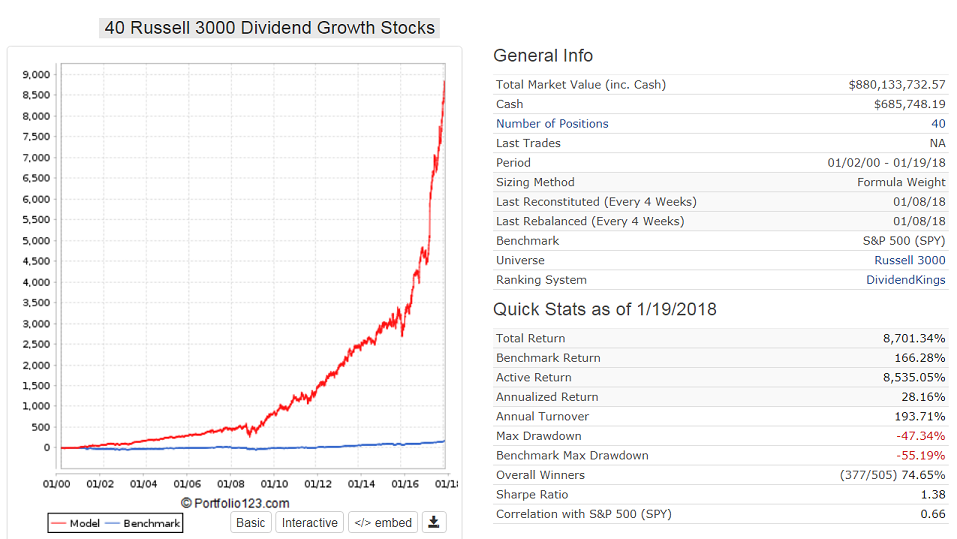

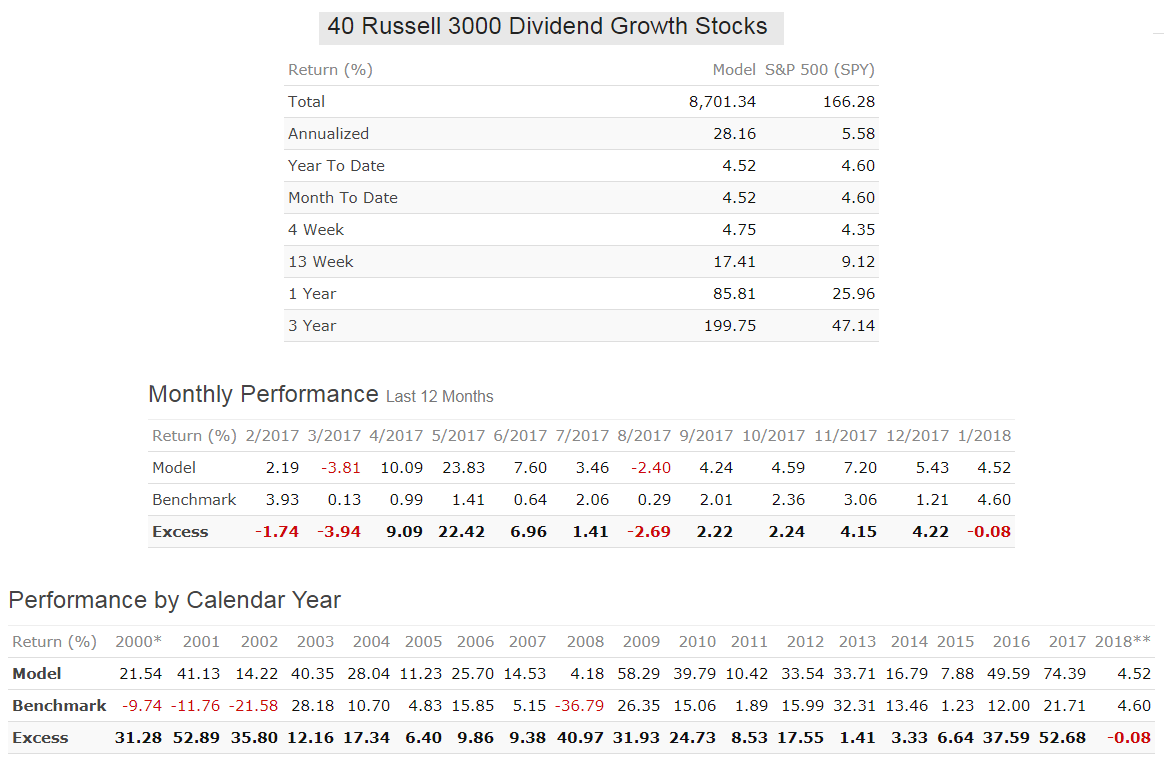

You don’t have to concentrate on the small caps. Here is a 40 position model, low turnover of 190%, annualized return= 28%, and no market timing, with the smallest MktCap of a position > 1-Billion.

Never made a loss over a calendar year.

Having been at this a while, and having greatly underestimated the slippage and volatility of small / micro caps, I have been focused much more on the mid-cap space. It seems that a great backtesting larger cap model, like Geov’s, will at worst market perform out of sample, while a great backtesting small/micro model could completely blow up out of sample.

My other source of confusion, is the desire to go so small that institutions are not interested. I would think you would want to find stocks where institutions can play, as they are the major drivers of price. Being a small fish, you can get in and out of stocks where institutions play without impacting price, as opposed to stocks, where institutions can’t play and are much more subject to volatility and even manipulation.

Here’s an article from Seeking Alpha this morning. By their analysis, price-to-book was the best value factor in 2017.

https://seekingalpha.com/article/4138638-value-2017-worked-wall-street

It all depends on how thoroughly the model has been tested, in addition to a very large number of other factors. Mid-cap and large-cap models can fail too.

But institutions ARE interested. Almost all the stocks I invest in have institutional ownership percentages greater than 25%, and a number of them are greater than 80%. OK, I do own shares of some companies like GSL and BASI, with institutional ownership only 5%. But I also own lots of shares in NWY and FWP, with institutional ownership near 90% to 95%.

By the way, what kind of “manipulation” do you see happening in the microcap space? I haven’t come across any myself, but maybe I’m not looking hard enough.

The post on NHLD come to mind the other day. The stock shot up like 60% then came crashing back down. It doesn’t take much to send a thin stock flying around for seemingly no good reason. To each his own. My small cap experience has not been good, and one key to investing success is knowing your personality and what fits it. I wouldn’t rule out a microcap model, but it wouldn’t be more than 20% to 30% of my overall equity exposure.

The other question is how much effort is required for good performance.

Yuval’s small-cap model shows 3,345 trades and weekly rebalancing.

My model above is rebalanced and reconstituted every 4 weeks and shows only 505 trades. If this model is only rebalanced and reconstituted every 8 weeks, then annualized return = 26%, not much different to the 28% of the 4 week rebalanced model . This would indicate that the model is fairly robust, and does not depend on accurate signal execution.