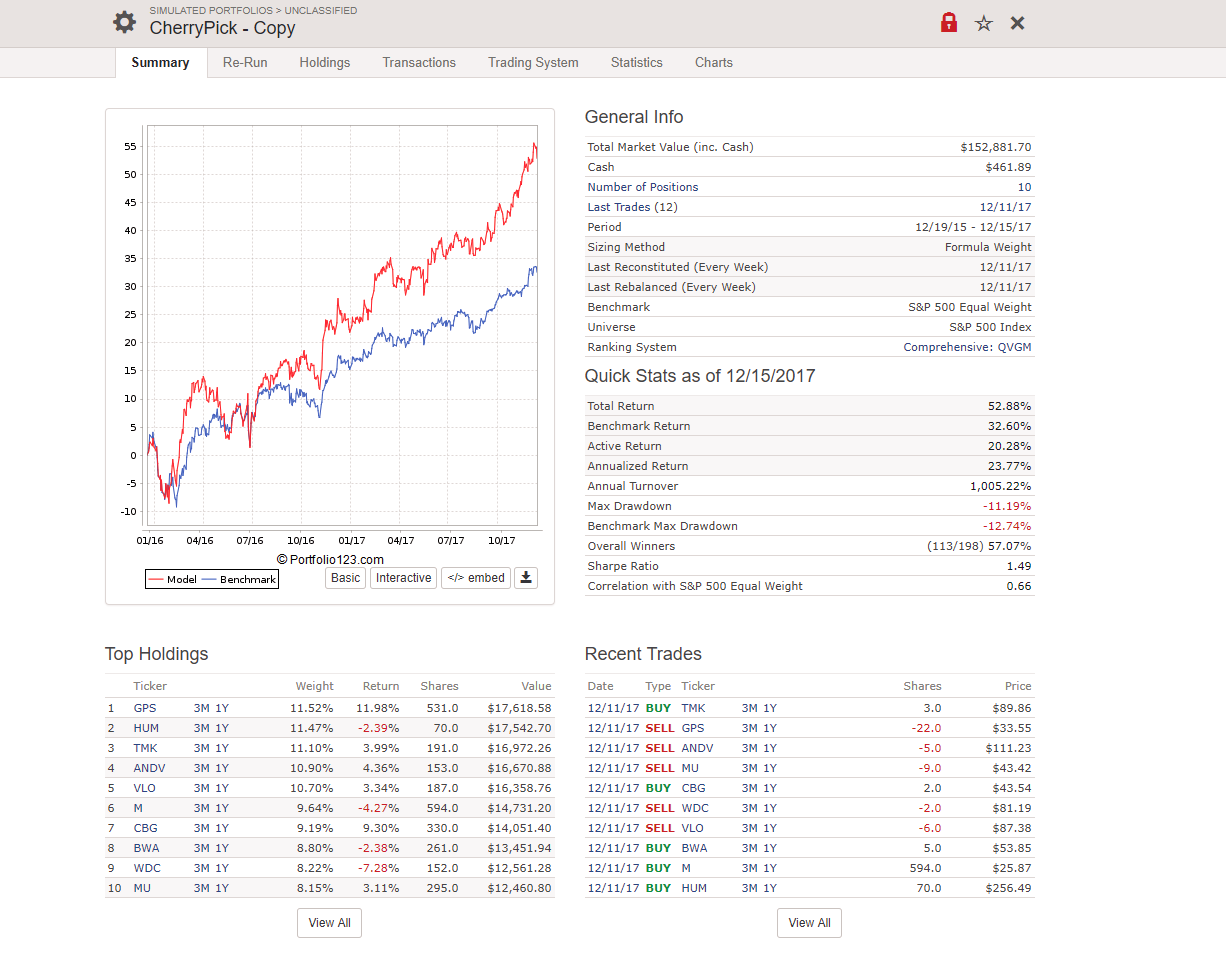

I’m trying to recreate the Cherrypicking the Blue Chips - Folio designer model using Marc Gerstein’s paper describing the rules. I’m using the new formula weighting option, incorporating beta and rank in an attempt to reduce the standard deviation of the model. However, I can’t get the top holdings to match up exactly. A portion of the holdings are the same as the designer model holdings but some are different. Does anyone know what I am doing wrong?

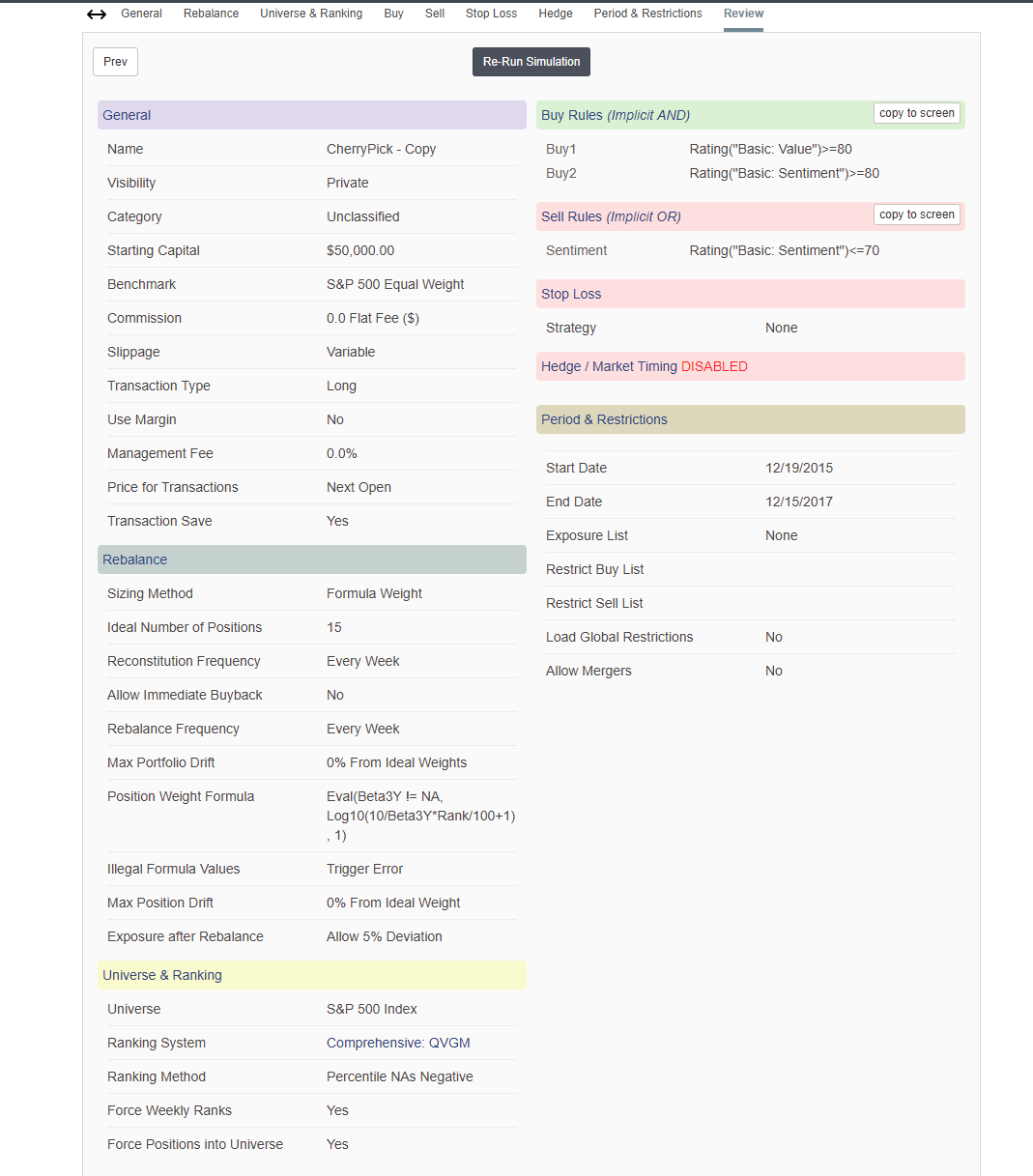

I was checking various permutations to see if I could get the positions to match, and chose every day as one of the settings. The settings in the screenshots are my intended settings.

Thank you for the suggestion about the launch date. I will rerun the simulation with a launch date in 2013.

I reran the simulation with the exact launch date of the official model but the positions and statistics still don’t match up. I was unable to run a simulation starting from the pre-launch date of 1/2/99 shown in the whitepaper due to the limitations of my account type.

Comparing transactions in the official model to the copied model, I can see that the official model trades much more frequently. The whitepaper is referring to the non-Folio version of the model and I may need to try some adjustments in the buy and sell rules to make it trade more frequently.

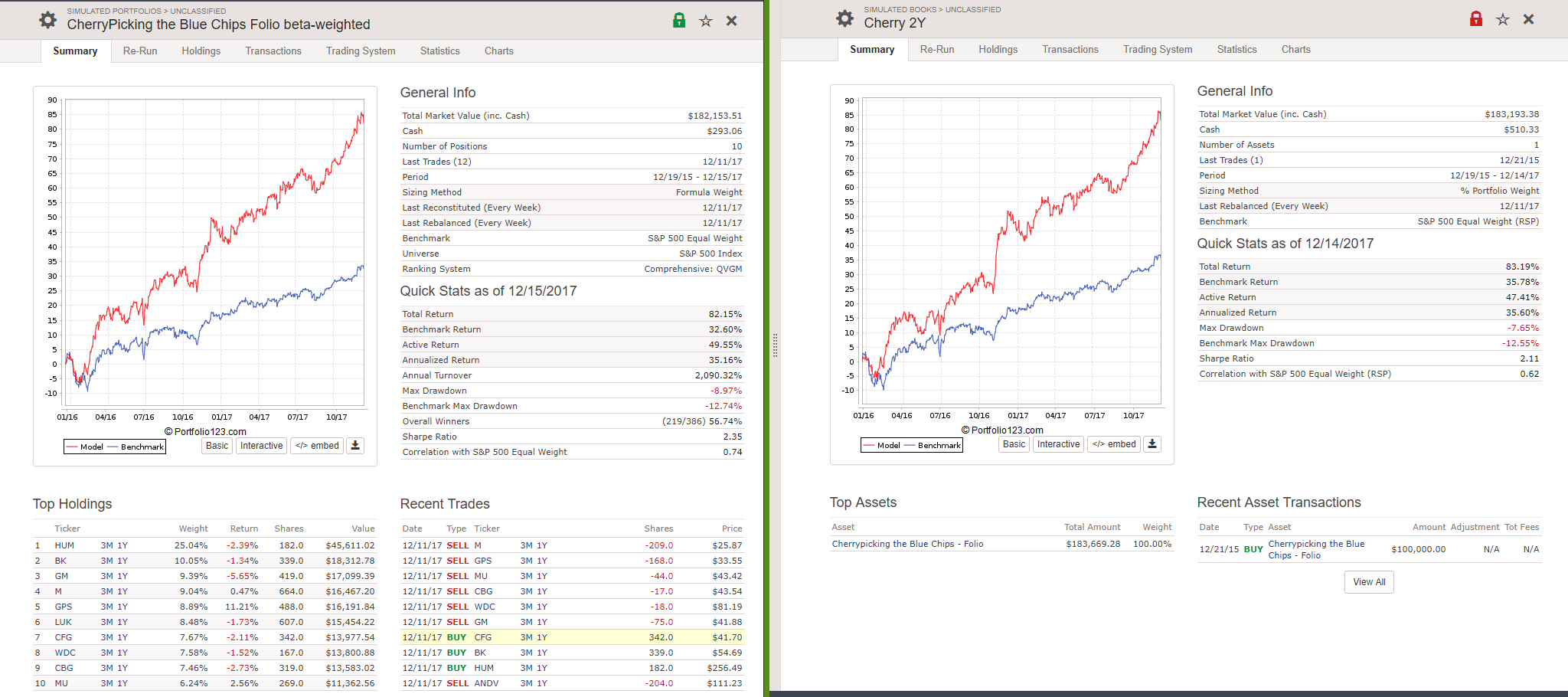

I’ve confirmed that the positions in the copied model match the ones in the standard official model. Looking at the description of the standard model, it says: “you may want to check the companion “Cherrypicking the Blue Chips - Folio” strategy, which uses stricter sell rules and re-balances weights to equal each week.”

This brings the copied model close to the official model. I believe there is one more sell rule that reduces max drawdown. It appears to have something to do with the “Final Stmt” column in the ranking. KSS sells on 9/4/2017 despite not meeting the above sell conditions. However, the N from the previous week displayed as a Y on 9/4, showing that the final statement became available. Are there any drawdown reducing sell rules that occur when earnings are released?

Unfortunately I was not able to figure out the missing rule. Hopefully Marc would be able to help out. However, the beta-weighting and some additional buy rules limiting sector and industry concentrations were able to increase the Sharpe Ratio and lower the standard deviation of the model.