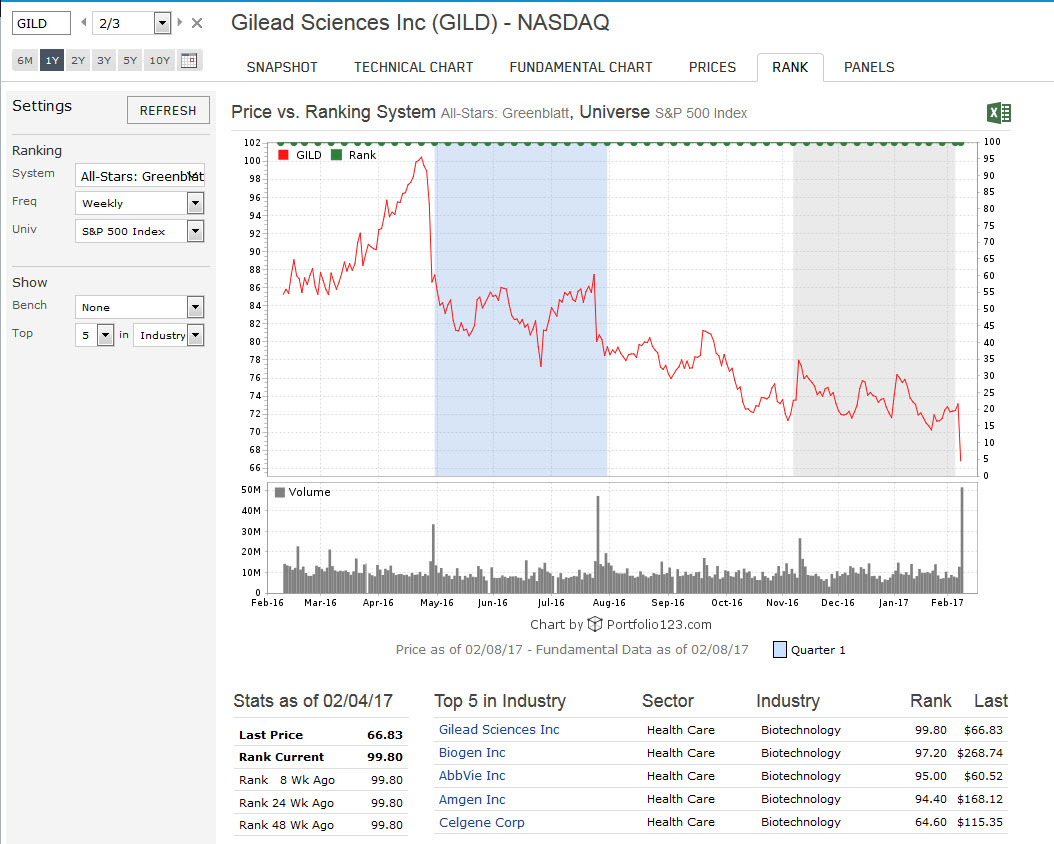

I am still long GILD but I understand why it scores highly on these ranking systems, whereas the share’s been declining for the past year or so.

The thing is… All these ranking systems have an implicit assumption in that the future will be reasonably similar to the past. What they are mostly angling for is mean reversion: the stock got beaten unfairly, priced below its intrinsic value and now it will revert to its justified price. This assumption doesn’t apply to companies like GILD because their business model is too unpredictable. Allow me to explain.

What’s happening with GILD is that their HCV drugs have cured most of their patient base - so they have stopped using it. They need new patients to purchase their drugs but (1) due to hefty price, insurers and Medicare/Medicaid only purchase these drugs for the sickest patients (2) to be able to sell more they are reducing the price, (3) other competitors such as ViiV are coming up with their own drugs to take market share. In the last earnings call, the CEO said that the HCV revenues were expected to decline from 14 billion in 2016 to 9 billion in 2017. The thing is, he may be just conservative because he may not really have much certainty. My point is that drug sales (especially curing drugs) can be so volatile that the info on past financial statements is not necessarily indicative of the future.

There are other issues in biotech as well. Lot of these companies have a monopoly on their drugs due to patent protections they enjoy. Once the patent protections expire, generic drug makers are allowed to produce biosimilar drugs, which undercut their profits. So once they “fall off the patent cliff”, it’s anybody’s guess how indicative their past performance will be.

You can also see a similar issue with energy companies. If I’m not mistaken, the Greenblatt Ranking/Magic Formula should perform much better in 2015 if you screen out the energy companies. In 2015, the gas prices hit rock bottom, which reduced the profits of the energy sector. Here, past financial statements are not indicative of future performance due to volatility of gas prices, thus Magic Formula and other fundamental analysis tools may not work as well. When you are buying an energy/gas/commodity/mining company, you are also placing a bet on the prices of gas/commodities/metals.

So you can simply filter out energy, biotech and mining companies. I think this improves the results somewhat for the Greenblatt ranker for the year 2015 - as it otherwise gives energy companies a high ranking for that year.

But as always, as Stephen Penman wrote in Accounting For Value, when buying a business, know the business. Screens can be useful but ultimately you have to make a judgment about the future profits of a company.