I have come to expect that when income statement data is updated upon a 10Q’s release that the cash flow data is updated simultaneously. I have now discovered to my chagrin that this is not the case. The chart below shows that in the last few months the cash flow data for SGM has lagged behind the income data by several weeks three times in 2016, while in 2015 they always changed on the same date. SGM looked like a great stock when I bought it a few weeks ago; now I see I was relying on completely inaccurate cash flow data. Three of my most important factors are accrual ratio, free cash flow margin, and free cash flow yield, and I was misled by this lag to think that SGM had outstanding numbers in all three. In fact, all three are terrible because the actual 10Q shows negative TTM operating cash flow. Why is some data updated weeks after other data? This makes the ratios I rely on–particularly the accrual ratio–practically useless, at least in this case. Should I always wait for “complete statement” to be true before buying a stock? Do I need to check every company’s 10Q before buying? In this case, at least, I made a few bucks, but this worries me for all sorts of reasons.

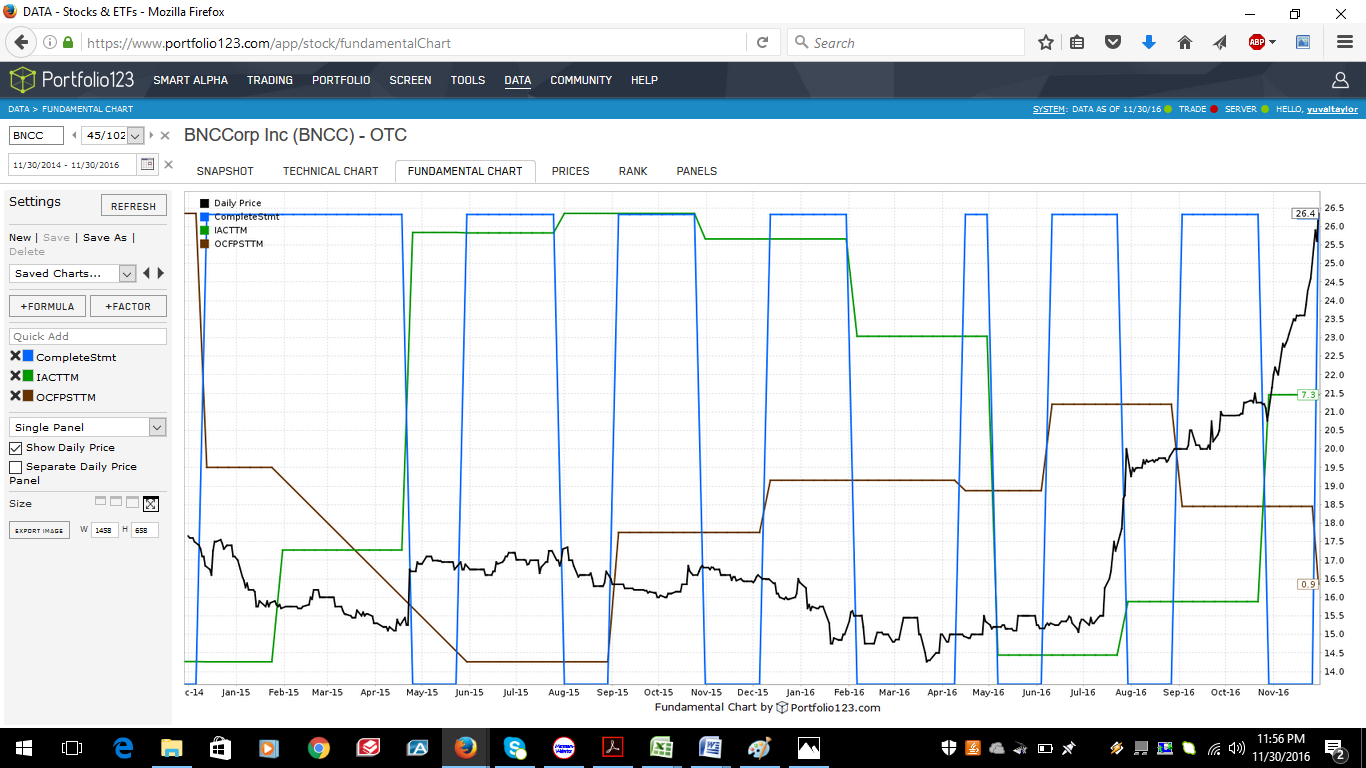

It’s even worse for OTC stock data. Check out the lag between the income and the cash flow statement for BNCC. You might as well have the data appear in different quarters.

Yuval, what are you concerned about?

- That others get to see the fundamentals before we do,

or - That a single earnings release can make such a difference in the fundamentals.

- That my port tells me to buy a stock and 3 weeks later tells me to sell it. As happened with both SGM and BNCC.

OK, I can screen for these stocks by using the following rules: CompleteStmt = 0; NetIncCFStmtQ != na and NetIncBXorNonCQ != na; Abs(NetIncCFStmtQ-NetIncBXorNonCQ) > 0.1. I did a backtest and it looks like a little over half of the stocks without a complete statement at any one time are reporting income statements from the new quarter and cash flow statements from the previous quarter. That means that when the statement is final the rankings will change significantly. I am going to try to exclude these stocks from my universe and see if that helps or hurts. This is not P123’s or Compustat’s fault, it’s the fact that earnings releases often don’t include cash flow statements, which I didn’t know until now.

At least you can take consolation from the fact that the trend is progressing toward greater completeness on the initial release. When I started, all you’d get at the outset were sales and eps. At least now, we usually get income statements and balance sheets that are if not complete are close to it. Hopefully, progress will continue and we can get all or at least parts of cash flow statements on the early release. It’s the ever present tradeoff between speed/freshness versus accuracy at the company end.

Well, there’s a silver lining to this. I’ve now discovered that cash flow statements in the financial services industry are for all intents and purposes useless. Nobody looks at them. I definitely have some fixing to do when it comes to ranking financial-sector firms. Someone wrote a dissertation on this: https://gupea.ub.gu.se/bitstream/2077/35272/1/gupea_2077_35272_1.pdf.

[quote]

3. That my port tells me to buy a stock and 3 weeks later tells me to sell it. As happened with both SGM and BNCC.

[/quote]Then you may want to look into setting the fallback option to NA. Something like this:

Sales(0, TTM, KEEPNA)

EDIT: Using KEEPNA may help you with turnover.

Another thing that you may want to consider is conditional rankings for financials. (For example, financials by income, non-financials by cash flow).

Aso, if you find non-financials with this turnover issue, then you may want to think about adding conditional ranking for those types of stocks as well. (In general, if an item does not get released in the preliminary statement then it is not very important.)

Personally, I have had great success eliminating unusual industries such as financials altogether. However, financials are now cheap and may soon have the catalyst of rising long-term rates.

I guess what really matters is whether backtest can reflect the fact that eps and sales are recorded earlier than cashflow.

Terry

Chaim -

Yes, I use lots of conditionals in my rankings for financials and am planning to add some more. I did some backtesting last night and realized that free cash flow really makes no difference to financials, but makes a big difference to non-financials; on the other hand, tangible book value to price is a great ratio for financials and relatively insignificant for other stocks. I’ve already taken into account that EV-based ratios are useless for financials, as is return on capital, and that return on equity and p/e backtest far better for financials than for other stocks. So the question becomes whether to make a ranking system complex enough to handle all those differences, to use two ranking systems (one for financials and one for non-financials), or to refrain from buying financials and just concentrate on non-financial stocks. The latter would be a huge difference in my strategy–usually my investments are about 25% in financials, and they’ve done pretty well for me. So I’m leaning toward the first option.

The KEEPNA option doesn’t seem to apply in this case as the turnover isn’t coming from NAs but from incomplete statements–the fact that earnings releases usually omit cash flow statements and they’re put into the database a few weeks before the filed 10Q.

Terry - the backtests definitely reflect this fact. Which is a relief. PIT data is where it’s at.

- Yuval

In virtually all of my systems, the first line of the Buy rules (which consists of core requirements such as price, liquidity, etc) includes the following code:

& Sector!=FINANCIAL

Financial corporations are such a mess of cash-flow and balance sheet manipulation and bizarre accounting approaches that they are excluded from consideration by the vast majority of professional money managers and 95% of professional value investors. In addition, their accounting is so complicated that partial releases are the norm, not the exception, as you have discovered.

Not to say that one can’t reap a profit from a mean-reversion or momentum trade in financials, but trying to understand what is truly under the hood of these companies is virtually impossible. They are opaque, and in the opinion of most professional money managers, uninvestable. Sure, they may do well for awhile now, since everyone expects interest rates to rise, but I have found that in a bull market most other sectors outperform financials. I have done quite well without the headache of holding them.

/C

Chris -

You may be right. I just did a summary of my closed positions over the last twelve months. 26% of my investments were in financial companies and 8.5% of my profits were made from them. That’s despite the fact that the financial sector outperformed the market in the last twelve months.

On the other hand, my backtests tell me that if I improve my systems just a wee bit I’ll make more money including financials than not . . .

- Yuval

[quote]

The KEEPNA option doesn’t seem to apply in this case as the turnover isn’t coming from NAs but from incomplete statements–the fact that earnings releases usually omit cash flow statements

[/quote]Yuval, maybe I was not clear in explaining, but I am pretty sure that KEEPNA would reduce the turnover in the situation that you are describing.

Why?

Because here is what was happening:

During the preliminary period, you had new income statement data–which produced solid rankings–and missing items from the old cash flow statement which produces another solid rank. Together the rank was high enough to buy.

A few weeks later, when the new cash flow data came in, the updated rank was low enough to sell.

But if you would use KEEPNA, then what will happen is as follows:

During the preliminary period, missing cash flow items would cause a very low cash flow rank. It would then skip this stock. Hence, lower turnover.

Chaim -

Maybe I don’t understand how KEEPNA works. There’s no NA in my cash flow data. It’s based on the latest figures. Would KEEPNA switch it to NA if the latest figures don’t match the date of the latest figures of the income statement? Would it change the default if the statement is not complete?

- Yuval

Yuval, here is what happens:

Normally, cash flow TTM items are the combined numbers for quarters 0 through 4.

However, when the latest quarter is missing and it’s preliminary, it will “fall back” and add up quarters 1 through 5 instead of returning NA.

If you use KEEPNA then it will keep the NA value and not “fall back”.

In SP500 universe, all the sectors performing same since 1999

Sector!=FINANCIAL has no impact in value based system.

Berkshires some of the major holdings WFC, USB, AXP, MTB, BK, GS are financials.

Thanks

Kumar