as some might have noticed there is a new Smart Alpha model available. Below I include the model description and a couple of screen shots of the rolling backtest results.

Cheers,

Florian

7sisters Perpetuum Alpha

This 5 stock model is based on:

a custom universe with stocks in momentum;

a filter which only includes industries in momentum;

a ranking system with well researched alpha-generating factors including high cash flow, low valuation and positive earnings estimate revision.

The goal is to achieve outperformance using

high liquidity with AvgDailyTot(10)>1,000,000;

moderate trading effort (13x turnover per annum);

a 2tier profit taking mechanism implemented in the sell rules;

market timing which switches the entire portfolio to IEF during unfavourable market conditions. The timer was tested out-of-sample since May 2015 and avoided both 12% draw down periods of the S&P500 since then.

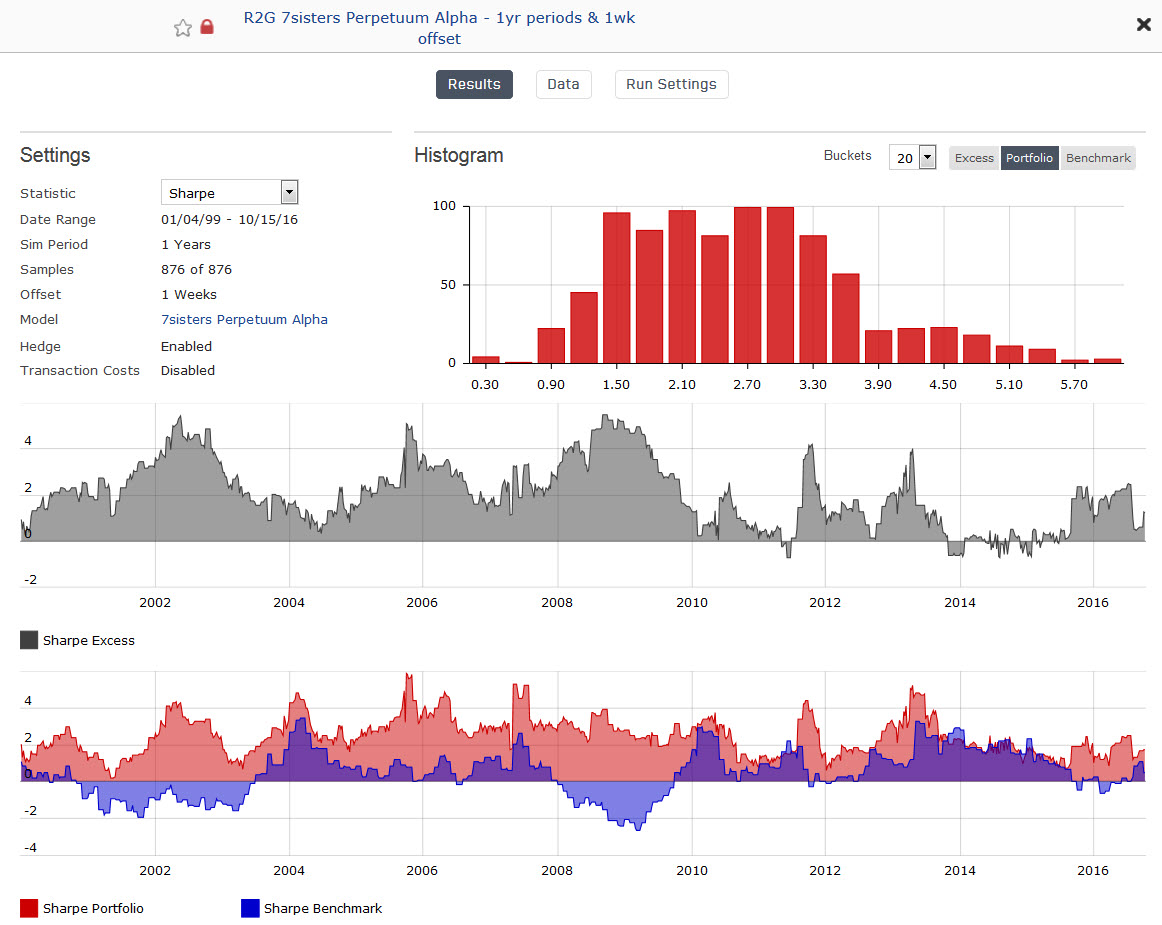

The simulation (Jan 1999- July 2016) points at a medium risk profile and the rolling backtest (1 yr periods with 1 wk offset) produced 876 investment periods with the following stats:

over 99% of investment periods delivering alpha (hence the name “Perpetuum Alpha”);

100% of investment periods delivered positive returns;

average Sharpe and Sortino ratios of 2.4 and 3.7, respectively;

highest MDD of 29.7% vs 52.6% for the S&P500 benchmark.

please see the relevant stats below. Overall still a satisfactory backtest but not as good as the SA model.

I don’t recommend to run the model without hedge due to the dynamic nature of the underlying universe. The universe is based on stocks in momentum and the number of available stocks is fluctuating strongly. The hedge periods correspond to times when the universe has very limited number of stocks, i.e. 50-300 stocks instead of 300-1000 during “normal” market conditions. With reduced number of stocks the quality of choice is obviously compromised and this leads to lower returns and more severe drawdowns.

hth,

Florian

EDIT: the last two images show rolling backtest with cash option during hedge instead of IEF. This reduces annual turnover from 1300 to 1100%, while keeping annual return and Sharpe at a similar level.

Florian - just to make sure I understand (reiterating your points above, with questions below each point):

This only holds 5 stocks at a time.

→ Shouldn’t we expect this to have very high volatility?

You create a custom universe with stocks that have momentum (for however you define momentum)

→ Doesn’t that drive lots of turnover as stocks come into/out of that universe? Or do you hold onto stocks even if they drop out of the universe?

-Within that high momentum universe, you rank according to cashflow yield and earnings estimate revisions.

→ So this is a momentum + value strategy primarily? Why not bundle the momentum and value factors into a single ranking function?

High and low is relative. In order to give you a decent answer I did the following experiment. I sorted the SA model list by 3 month performance, assuming that other recent outperforming models might use similar ranking system. Then I picked those models which only hold 5 stocks and put them each into a separate book and simulated the maximum holding period. Here are the results:

(standard deviation - model name)

23.3 - Perpetuum Alpha

31.4 - 1st! SME

32.8 - Baker’s Ultimate 5

33.7 - Keating’s Ultra Extreme Trader

29.2 - Five Hidden Gems

27.7 - Long Short Term High Liquidity

31.8 - 5 stks model

15.2 - Russell 3000

14.8 - S&P 500

So overall Perpetuum Alpha has a higher volatility compared to the S&P500 and Russell 3000, but still lower than its smart alpha peer group.

The positions are forced into the universe, yet turnover is low. Many other models consider a 5 day gain already as momentum, whereas a longer momentum / trend is required for a stock to enter into this smart alpha’s universe.

Perpetuum Alpha uses an 11 factor ranking system. The more factors a ranking system uses, the less likely it is that it picks what you actually want. In this respect the universe is a kind of filter, only allowing stocks in momentum to be ranked.

No. This is the only Smart Alpha model for which I use this approach. But it makes sense in general, and you could generate a restricted universe for any alpha-generating factor. The momentum approach is probably one of the best to use in combination with market timing. Other strategies such as low beta combined with dividend income would not necessarily need market timing.