If you are like me, you may have been initially attracted to the eye-popping theoretical simulated returns of high-turnover, low liquidity, low number of stocks models available. But in practice the results are mixed. In some of these models, I made lots of money. In others, I lost lots of money. In the end you could say it’s a wash. There is simply no way of knowing ahead of time which will perform. Even within models from a single designer, you can see highly variable performance. It’s a “lottery ticket”. Shoot to the moon or crash miserably.

In additional to uncertainty in real-time performance, I saw a major deviation between the model results P123 was reporting and my real-money brokerage account. One model (Model A) was performing flat, but my real-money account was up a whopping 50%. Another model (Model B) showed it was up 7%, but my account was only up 1.5%. The designer of Model B suggested that I make all trades within 2 hours of market open, but I was making all trades within the first 15 minutes.

Due to these challenges, and others such as transaction costs and hassle of trading large numbers of stocks, I started developing low-turnover strategies. Some of these models are nearing the one-year out-of-sample real-time performance.

Little to no optimization is used, and the stocks it picks are checked to see if they make sense, and the historic simulated performance is checked to see if it makes sense and fits in a pretty wide range of expected values.

These models have one or more of the following characteristics:

-Stable dividends

-Growing dividends

-Safe dividends

-Defensive sectors that resist cycles (consumer staples, utilities, healthcare)

-Low turnover “investing”, not high turnover “trading”

-Well known factors such as value, quality, growth, financial safety

-Reasonable expectation of earnings, sales, cash flow

-Low voliatilty in stock price or business fundamentals

-Conservative accounting

-Influenced by Marc Gerstein’s forum posts and online course

So far, these model appear to perform well. I would judge these models not on whether they beat the market index, but whether they continue to pick stocks with the intended characteristics.

“Ultra Low Turnover” means the holding period is significatnly longer than one year. “Long Term Capital Gains” means the model will try to hold the stock at least for 1 year, to reduce taxes.

Some of these models are free, the others are low priced.

Defensive Dividends - Long Term Capital Gains - 10 stocks

https://www.portfolio123.com/app/r2g/summary?id=1372671

Healthcare Investor - Low Turnover - 10 stocks

https://www.portfolio123.com/app/r2g/summary?id=1376455

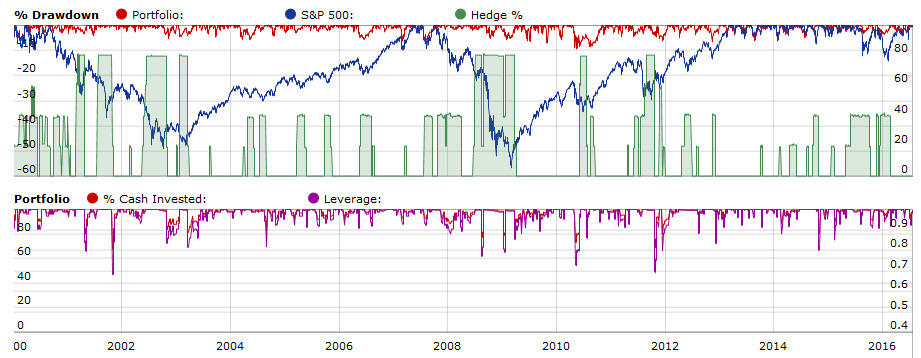

Hedged Investor - 3 month rebalance - TLT Constant Hedge - 20 stocks (free)

https://www.portfolio123.com/app/r2g/summary?id=1383766

Large Cap Consumer Sectors - Ultra Low Turnover - 10 stocks

https://www.portfolio123.com/app/r2g/summary?id=1417539

Large Cap Defensive Dividends - Long Term Capital Gains - 10 stocks

https://www.portfolio123.com/app/r2g/summary?id=1386764

SP500 Defensive Investor - Long Term capital Gains

https://www.portfolio123.com/app/r2g/summary?id=1410449

Staples Investor - Ultra Low Turnover - 10 stocks (free)

https://www.portfolio123.com/app/r2g/summary?id=1392722

As usual, stocks are risky, I’m not a RIA, and I make no gaurantees.