I was wondering if anyone has any experience with price-blind strategies.

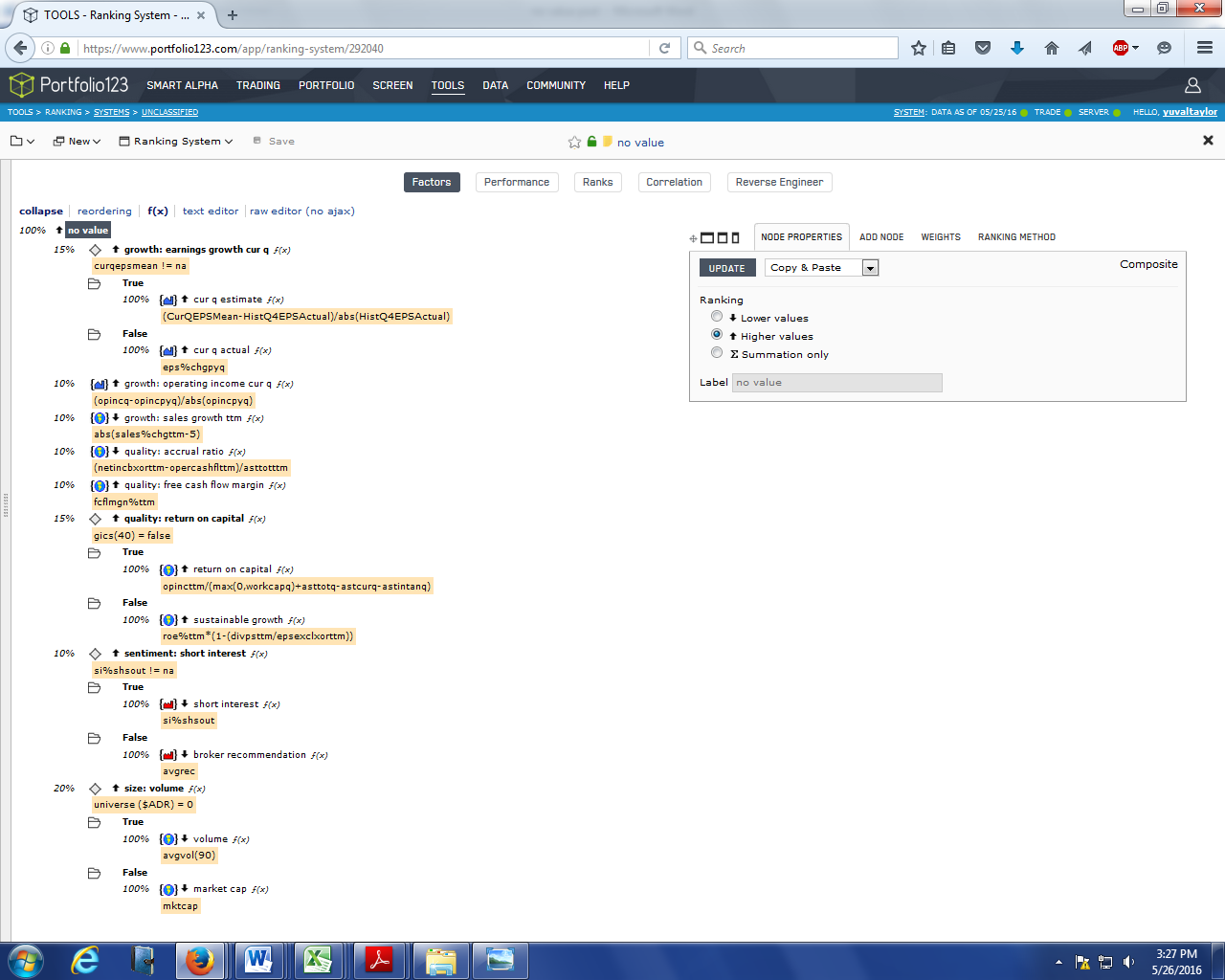

I have a ranking system that’s based on only eight factors: three growth, three quality, low short interest, and low volume. There’s not one reference to price (or market cap or enterprise value) in it. No value factors, no momentum. You can find the system here: https://www.portfolio123.com/app/ranking-system/292040.

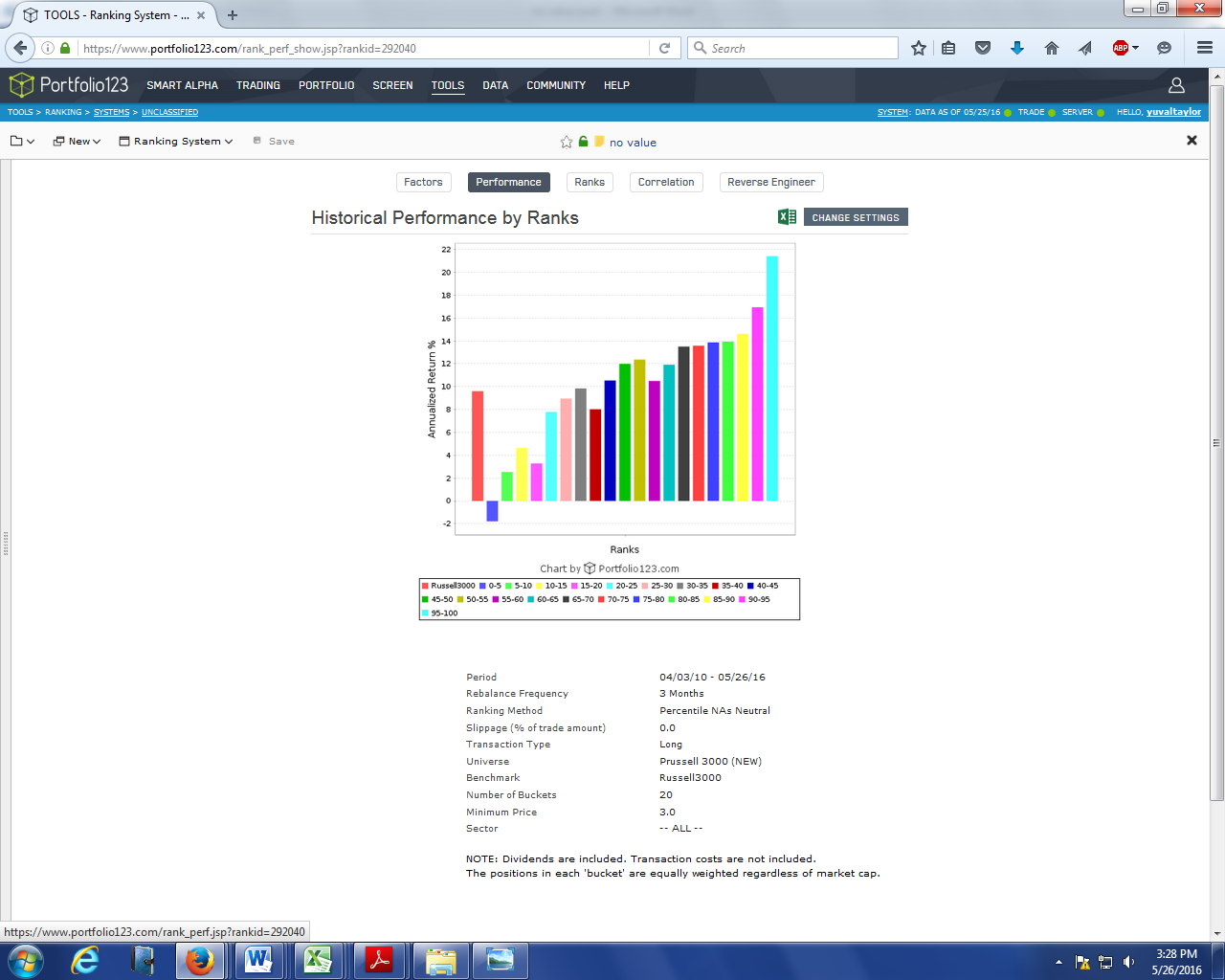

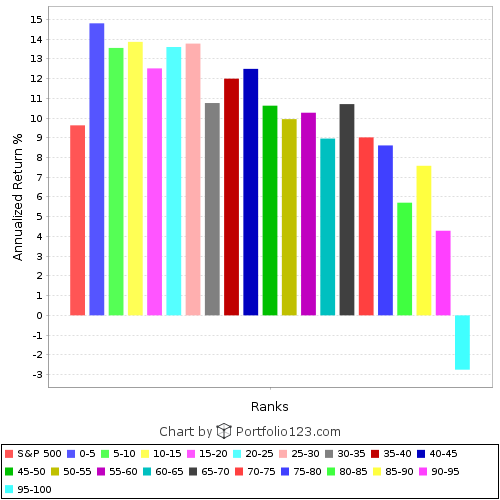

No matter how many stocks you choose from this system—the top 5 or the top 100—and no matter what universe you choose them from (SP1500, R3000, a universe that includes ADRs, even the SP500, though not quite as well), and no matter what time range you use, you’re going to handily beat the corresponding benchmark (so long as you don’t rebalance too often: a 3-month or 6-month rebalance works best; the slippage from a 4-week rebalance will hurt your returns). None of the growth and quality factors I’m using are terribly unconventional: EPS growth, EBIT growth, revenue growth (5% being ideal), accrual ratio, free cash flow margin, return on capital. Other growth and quality measures may work just as well or better—try them. It’s not overengineered—it’s vastly simpler than the ranking system I use myself. I’m sure you can optimize this system and improve its backtested results—I haven’t bothered. This system outperforms in bear markets and bull markets. It performed well in the last five years but it also performed well in the crazy markets of 1999 to 2001 and the various markets in-between.

I think T. Rowe Price would have liked this system. It reflects his basic thinking. Price did take value into consideration—he tried to avoid stocks with a p/e ratio much higher than its historic average—but I don’t think that was a major focus for him.

But this system contravenes Graham-Dodd, as well as the EMH.

Here’s my reasoning. The price of a stock is determined not by its intrinsic value, which is non-existent, but by the buying and selling of that stock on the secondary market. A company that is currently not attracting a lot of attention but, due to strong performance, will soon attract more interest among investors is going to see its price go up. This is very easy to understand, and not so terribly hard to predict. All you need to know is what investors are looking for when they begin to invest or substantially increase their investment in a company: revenue and earnings that are sustainable and improving. That will never go out of fashion because that’s the fundamental basis of any company’s success.

Perhaps price shouldn’t play such a big part in our stock-picking, and perhaps chasing after prices—whether low (value) or high (momentum)—causes us to lose sight of what matters most in the long run: a company’s likelihood to outperform. And that has nothing to do with the price of its stock.

Has anyone else explored price-blind strategies? Any thoughts?