I was playing around with an idea and started with the Screener.

The idea produced encouraging results in the Screener (AR 15%) and I then implemented it in the Simulator. The results were very different. The simulation results showed a deteriorating equity curve over time, going to zero. Somehow, something was eating up all my starting capital and trading profits.

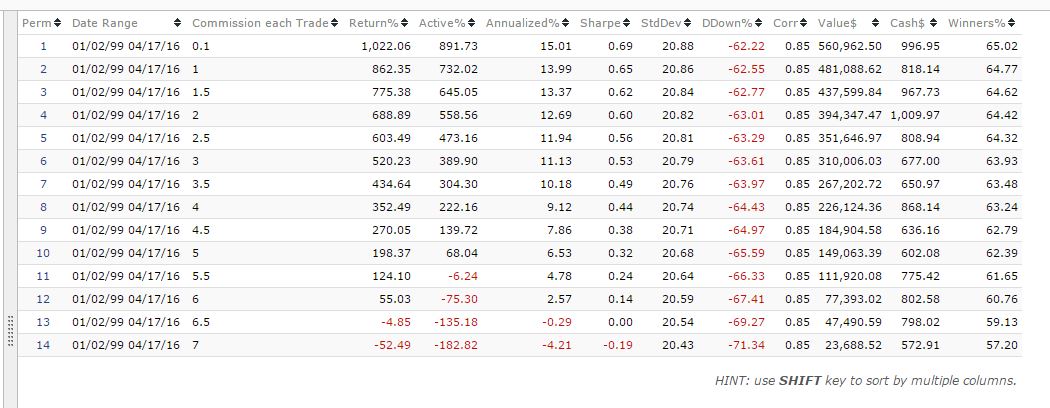

After implementing in the Simulator and investigating, I noticed that the model was higher turnover (515%) with a lower Realized Average Return (about 2.4%). This lead me to believe that either my slippage or trading commissions could be a problem. The universe is lower market cap SP500 stocks. I used variable slippage and it made little difference in the results.

I then tried slewing over commissions and starting capital. The model has 25 positions. For one test, I started with $50,000 starting capital. At $0.1 per trade, the Sim gave me performance that was very similar to the Screener. At my normal $7 per trade, it gave me the deteriorated equity curve going to zero.

I then tried with $200,000 starting capital and that ‘fixed’ the problem. It gave me pretty good results at my realistic $7 per trade. Which confirmed my earlier suspicion: the higher gross Realized Average Return from the higher starting capital could support my $7 trading costs but the lower starting capital could not.

Normally I worry about slippage but in this case it was trading costs.

- It would be nice to have both a variable slippage option as well as a commission option for the Screener. Just fixing commissions at $7 per trade would be fine with me (what I pay).

- In lieu of 1, I think I am going to go straight to the simulator to get a feel for real world performance. (This was an eye opener.). Starting capital and trading commissions do matter for lower Realized Average Return models, not just slippage.