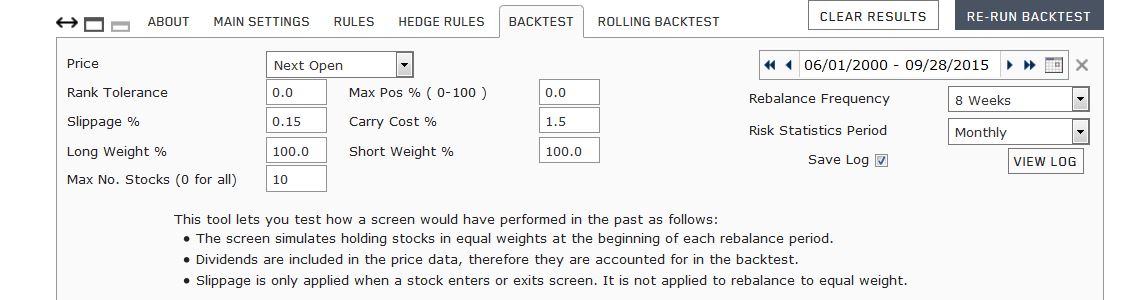

Could you explain me how the backtester calculates return period by period.

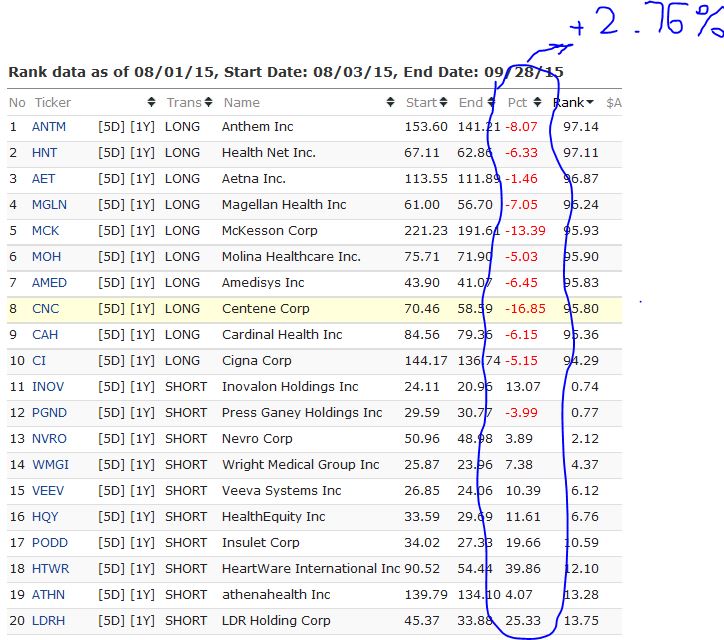

You can see at the picture that equall weighted average returns across all stocks in portfolio equals 2.91% howewer the backtester shows that profit is 5.06%.

This is long-short portfolio, 100% long/100% short.

Any chances to explain the calculation of return, I attach more screenshots.

What is the source of the diffrence (4.89% and 2.76%). What’s more why the total return form last period changed form 5.06% to 4.89% … in from yesterday to today.

P123, I need your help ![]()

A screen backtest equally weights all stocks that pass the screen per rebalance.

Select the ‘Save Log’ option when running the backtest to see the period return per stock with equal weight.

With this data, first compute the average long return and average short return. Then take the average of these two weighted by your long/short weight settings. Finally deduct the carry cost to get the period return (also given in the log).