I’m looking for systems based on the work of Meb Faber and Alpha Architect. I like simple allocation systems that use ETFs or Mutual Funds. Are there those types of systems here at P123? Right now I especially interested in systems with foreign allocations as well.

This should be easy by creating a custom list with the ETFs you want to use. Then use moving average crossovers for buy and sell rules.

Though the last time I tested the Ivy portfolio, it wasn’t pretty. I’d be more interested in the GTAA strategy that invests in the cheapest country ETFs, but P123 does not currently have the ability to determine the valuation of country ETFs.

I don’t have a foreign allocation port but I created these two ports back in 2012 using a 4 week rebalance. There is a 5 ETF version, and a 2 ETF version. The 2 ETF version selects from the 5 based on momentum ranking. The results are not “pretty” but better than putting money in the bank.

https://www.portfolio123.com/port_summary.jsp?portid=847826

https://www.portfolio123.com/port_summary.jsp?portid=847823

Steve

Thanks Steve, I was too lazy to recreate the sim that I apparently deleted.

Thanks guys. I hope to see more ETF rotational portfolios here at P123.

I think it’s becoming pretty popular nowadays for those who want to outsource a portion of their portfolio (at least from my experience as a Seeking Alpha reader).

ETF strategies should do well here on P123 with all the tools you have; heck many guys are using Excel (ex. http://itawealth.com/portfolios/ ) with good results. Lazy types like me would rather let those who enjoy building models have at it. =)

Admittedly, I spend most of my free stock reading time on SA and have noticed a lot of interest in rotational allocation strategies this past year. I hope more of you super smart P123 guys post there and drive awareness to your models.

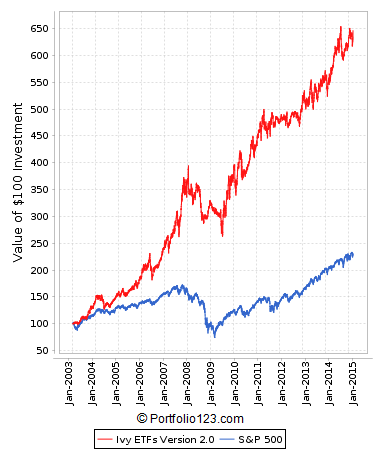

Creating rotational ETF portfolios with P123 is actually quite easy. Based on the learnings from Mel Faber’s Ivy Portfolio and Gary Antonacci’s Dual Momentum (two excellent books!), I use simple momentum-based ranking systems and moving average cross-overs. The other “secret” is a universe of not highly correlated ETFs.

For the portfolio shown below, I use this list of ETFs, invest in max 4 and rebalance 4-weekly:

- DBC: Commodities

- EWG: German Equities

- EWJ: Japanese Equities

- EWZ: Brazilian Equities

- FXI: Chinese Equities

- GLD: Gold

- ICF: Latin American Equities

- IEF: Mid-term US Bonds

- INP: US Real Estate

- RSX: Russian Equities

- SPY: US Equities

- TLT: Long-term US Bonds

The annual return since 2003 is 16.2%, with a max DD of 33% in 2008/09.

As for the fantastic returns (50% and more) of some Seekingalpha rotation strategies, I would be very careful. There are a quite a few authors who use leveraged ETFs and volatility ETFs - and present 3-year or 5-year backtests. Needless to say that inverse volatility ETFs and 3x-leveraged US Equities ETFs produced fantastic returns over long periods of the last 5 years, but can you reasonably expect the same returns over the next 5 years?

Another nice “trick” is to trade among a short list of ETF highflyers, such as a solar ETF, biotech ETF and micro-brew ETF (ok, you get the point …) and arrive at spectacular results. In hindsight, it is always easy to pick the best-performing ETFs, but how will these authors know the outperformers of 2016-2020?

Last but not least, many high-return strategies are doomed to fail due to excessive over-optimizing. Whenever I see a system that works great with a moving average of 83 days, but collapses at 80 and 86 days, respectively, you know the grim reaper must be around the corner …

As I said above, reading the two recommended books is the right step to “decent”, but reasonably attainable returns over the long run.

Bazooka,

Here you go:

https://www.portfolio123.com/app/r2g/summary/1358122

A simple R2G momentum based rotational model. I’ve invested in this for about 6 months. If no one invests in 3 months or so, I’ll take it down. Or you can build your own as mentioned in the thread.

Best,

Tom

Most of the high return etf rotation systems on seeking alpha have a ridiculous amount of data mining (you can easily break down their system with a sensitivity test by mildly varying the parameters) so expect their out of sample returns to be significantly worse than the backtest.

Scott

Cyberjoe,

Thanks a ton. Can the same thing be done with Fidelity Sector mutual funds? I’ve heard people pick/rotate assets from a list of 32 and I even read somewhere that a random choice of 12 would have beaten the market under most scenarios and simulations.

Tomyani,

Thanks for the link. I’m just know learning about momentum and “dual momentum” strategies. I hope you guys leave these things trading since it’s nice to cross compare simple strategies to the more complex ones.

*Yes; I’m aware to take caution of some the eye popping SA articles that use leverage and/or volatility; actually I wish more people would post simple strategies there, backed by academic literature, with realistic index beating returns and sharpe ratios

Sure, sector funds/ETF can be used for rotation strategies. You may want to check out the R2G model “Best Sector” (or similar) by geov: https://www.portfolio123.com/app/r2g/summary/1115335 However, this is no “pure play” system, but relies on market timing and hedging.

As far as the number of assets is concerned, I have experimented with larger lists of ETFs. Unfortunately, this does not help your performance very much, but drives turnover up, which is bad on April 15 ![]()

As mentioned above, make sure you select ETFs/funds that do not move in parallel. A rotation system can only work when ETF A goes up, while ETF B is flat or goes down.

That model above looks good, almost too good =) Do you guys open up the model to subscribers so one can see how it exactly works?

If you want Meb Faber-style ETFs or select mutual funds that tactically rotate based on moving averages, then the ETFReplay website was built for that purpose. No fundamentals. No stocks. No CEFs. Just ETFs and select mutual funds with technical analysis.

If you want something better, create a solid universe of ETFs on P123 that aren’t highly correlated which includes at least one that is anti correlated. Then develop a solid ranking system. Then buy the Top 15-25% of the ETFs based on ranking, and hold until they fall out of the top 40-50%.

Doug Short mimics Meb Faber’s system and publishes which etf’s are in and out.

You’d have to manage your re-balancing yourself to suit.

He does a pre month preview and post month post.

Personally, if I were tempted to go down this route, I would want to keep it as simple as this to reduce trade costs, curve fitting etc.,

Steady if unspectacular. No guarantees that relationships will work in the future.

http://www.advisorperspectives.com/dshort/updates/Monthly-Moving-Averages.php

Ressurecting this thread, because I’ve kind of rigged together a makeshift GTAA strategy.

Created a custom universe of global ETFs from this list (I’m sure there’s many more out there that could be added. These are mostly MSCI, but iShares also has a ton)…

http://seekingalpha.com/insight/etf-hub/asset_class_performance/countries

Created a custom list of the cheapest global countries using the screener below and match them up with an ETF where applicable … (ex. CAPE < 12 and P/B < 1.5). The more lenient the screen, the larger the universe.

Create ETF portfolio using the custom universe, InList in buy rule with the custom list of cheapest countries, and use the “Price Uptrend - Basic” P123 ETF Ranking to add some price momentum to the value in the universe to pick out a 5-10 etf portfolio. Might even look into using some timing using a moving average with EMM in a buy rule to move to cash during extended global drawdowns.

There’s no way to really backtest this, and the custom global value list has to be continually updated after quarter after Star Capital releases their data every quarter, so it will require some tracking out of sample to gauge success before I would put any real money into it. Still, a global strategy would be a welcome component to my overall investing approach. Even after a recent lift off in the last 6 weeks many countries are still dirt cheap right now with CAPE under 10 and due for mean regression, EMM seems to be picking up some steam after multi-year underperformance, and the US is uncomfortably expensive to me by many metrics of valuation.