Thank you all for the responses to my questions.

Now, I understand the investors should not panic about 5%-10% DOW main market sell-off, it is normal. It happends for last 2 years, eventually the market bounced back very stronger.

mgerstein,

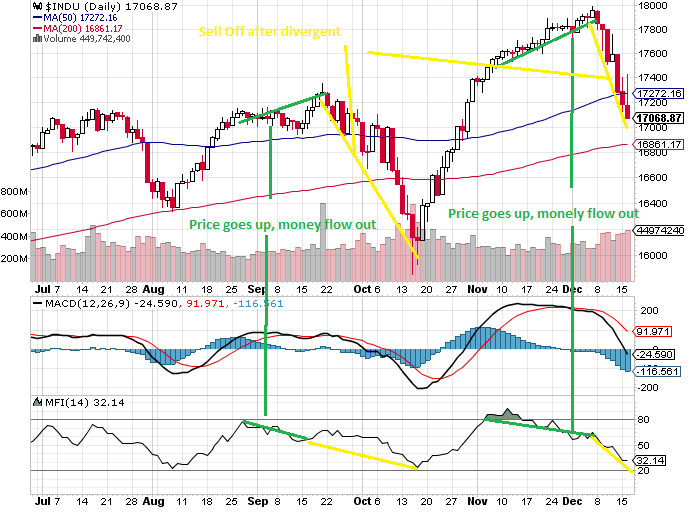

Now, I do have another question when the market sell-off like 16th Dec 2014, 5% discount from recent high (DOW 17050 from 18000), as the 3/4 of market follows main indexes, the yahoo commentary experts says, it is a great buying opportunities.

But, I don’t know what to buy using portfolio123 tool.

In case of Zack Rank, AAPL - 1 (Strong Buy), BRK.B- 2 (Buy), BBY -2(Buy), WU-2 (Buy).

In R2G the fundamental strategy worked better than small cap and trader strategy in out of sample. (Small cap strategy has liquidity limitations and slippage, etc.,)

Only, handful of R2G strategies beats S&P500 since R2G launch.

Believe, Basic user will benefit from experts, if there is portfolio123 subscriber only feature; special rankings for largecaps(may be 100 well known symbols).

Simple interface to run favourite company symbols to find buying opportunty and holding for 3 months, 6 months & 12 months

With these, well known and all time favourite stocks

BRK.B, AAPL, GOOGL, AMZN, JPM, HD, BBY, HPQ Just buy and hold strategy might double the money in 2 to 3 years .

I believe, this is far better than any R2G strategy in safetly wise and just buy, hold and watch.

I am looking for this kind of group stock recommendations to hold for next 3 months / 6 months / 1 year features from www.portfolio123.com weekly FUTURE stock performance holdings email along with Weekly past performance simulation;

==========================================================.

Note:

-

I have subscribed to IntelligentInvestment news letter (it promised 100% returns every year and it strictly follows quant and portfolio123 tools to select stocks);

My bad luck, It is in negative returns since March 2014 (for last 9 months), i unsubscribed few months ago.

-

Earlier this year, I have subscribed to 3 of the Picklehead trading systems, all of them lost money, around 20+%.

-

Built own simulation for micro and small cap with help of Denny’s guidance,

it returns 200%+ per year (after slippage and commission) for last 2 years on market open,

(Believe, you people notice on weekly performance e-mail , my name is on yearly performance rows)

a. mentally not prepared to trade this system, because of quant systems failures on Note 1. & 2.

b. I am in full-time job, i can’t watch the small cap falling down or climbing up daily basis,

c. can’t watch and buy for better slippage during market open, no edge to minimize slippage. small caps strategy success depends on slippage.

===========================================================

After being 1 year with portfolio123, and reading thru forum, i understand

You people have nearly 30+ years real investment experience (steve,denny,mgerstein,olikea,amiran,twytwy,tomyani,dwpeters,judgetrade,scott and many other experts) and have minimum 5 to 11 years experience using portfolio123.

Please, suggest basic user can directly benefit from www.portfolio123.com ?

- Without prior vast successful investment experience and

- just using simulation knowledge and

- investing time on weekly basis and only buying and selling stocks on Monday near market open.

Thanks

Kumar