I created two different custom series with the same rules but they show very different outcomes. The only difference between the two series is that in the first one, I put my criteria in the rules tab and in the second one I put my critieria in a custom universe. I don’t understand why they don’t produce the same (or at least very similar result). I made both series public and describe them further below. Thanks for the help to whoever responds!

First Custom Series: “Low$$EqWght$1to$5V2D”

https://www.portfolio123.com/app/screen/summary/561?st=1&mt=8

The only rule in this first series is:

LN(UnivAvg(“AvgDailyTot(2,2)>500000 AND Close(2)>1 AND Close(2)<5”,“Close(0)/Close(1)”))

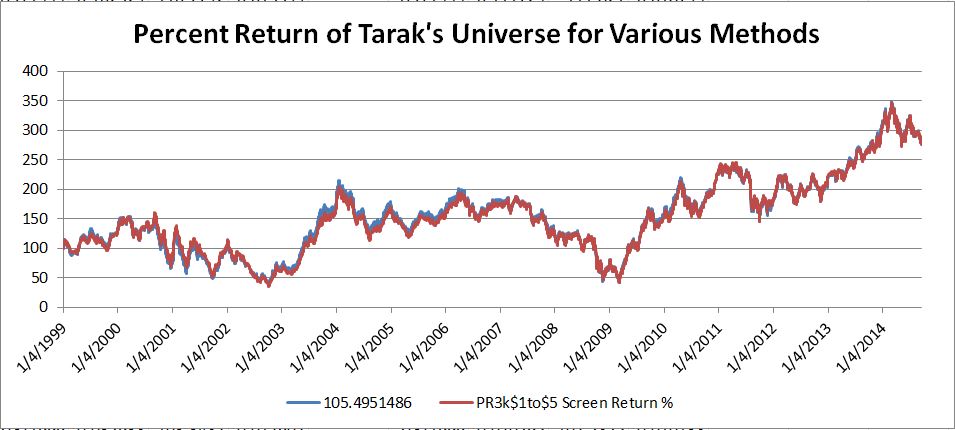

The above public custom series is an equal weighted cumulative lognormal return index for PR3000 stocks w/ vol>$500k and stock price b/w $1 and $5. The final value of the series is 2.64, which implies a 1300% increase in index value between 9/1/2001 and 9/14/2014. (e^2.64=14.0, which implies a 14x increase in value or 1300%).

Second Custom Series: “PR3k$1to$5CustUniv”

https://www.portfolio123.com/app/screen/summary/562?st=1&mt=8

The above public custom series is the same as the first except I put the 2 criteria listed below into a custom universe:

AvgDailyTot(2,2)>500000

Close(2)>1 and Close(2)<5

Public custom universe used above is named “PR3k $1to$5 Stock Price” and is linked here: https://www.portfolio123.com/app/screen/summary/113929?st=1

Then the only rule in my second series is:

LN(UnivAvg(“TRUE”,“Close(0)/Close(1)”))

This second series has a final value of 1.41 which is much lower than the 2.64 from the first. The 1.41 final value implies e^1.41=4.1x growth or 311% growth over the full period… very different outcome compared to the first series.

Thanks for the help!