Hi,

I spent some time doing an analysis of the intra-day spreads and volumes for the stocks I (and many here) typically trade. Maybe the results are useful to some of you.

I collected all recommendations of around 5 R2G models I have subscribed to for varying periods with varying liquidity (less than $100K to $1MM). I also added recommendations from three of my own models (recommendations from the sims, not live, but I do trade those live) with similar liquidity. In total, I got just over 1,000 recommendations over the past year. I then programmed a little tool to query the Interactive Brokers TWS API to obtain minute-by-minute open/high/low/close prices, bids, and asks, plus volume for each minute on the day of the recommendation. I can only go back one year with this API and a handful of stocks are no longer traded. But the results should still be fairly representative for the typical models people trade on P123.

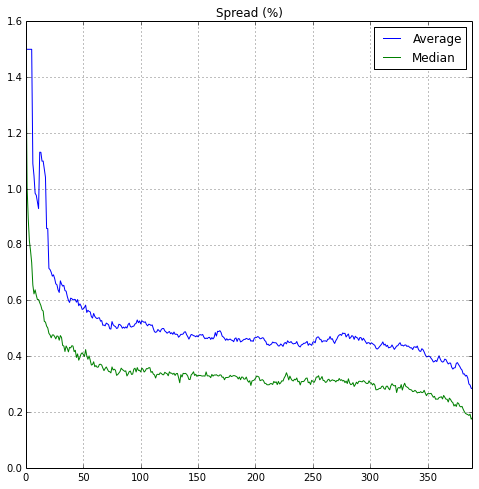

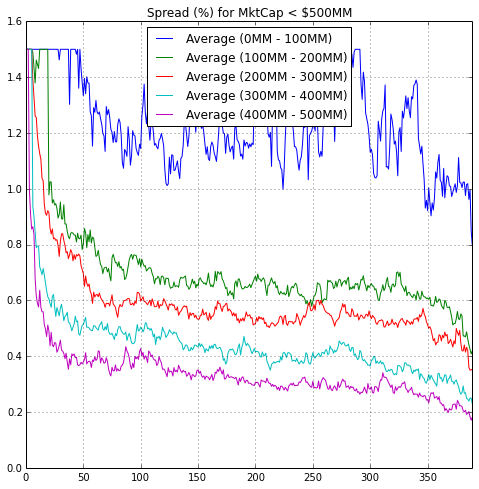

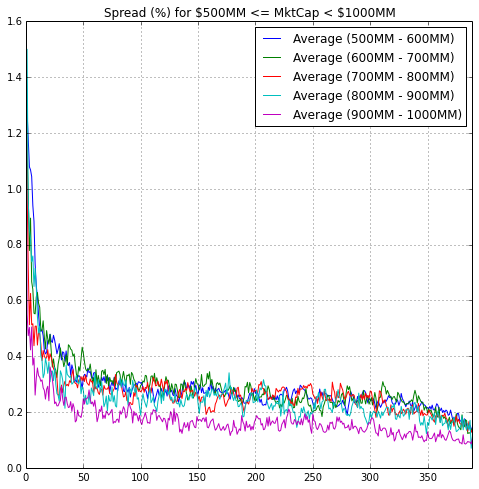

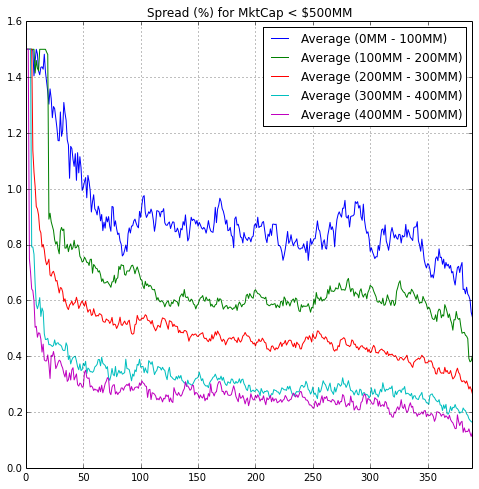

First, the bid-ask spreads. See the chart below titled ‘Spread (%)’. This shows the spread in percentage points, computed as (ask - bid) / bid * 100%, for each minute since the opening of the exchange. The minutes since opening are on the X-axis, spreads on the Y-axis. So for example, 50 minutes after opening (10:20 AM) the average spread is around 0.4%. (Btw, in this chart, I limited the spreads to 1.5%. The average spread at the open is 1,803,370%, after the first minute it’s 2.95%, drops gradually to 2.11% after 5 minutes. In the chart this is just a flat line at 1.5%).

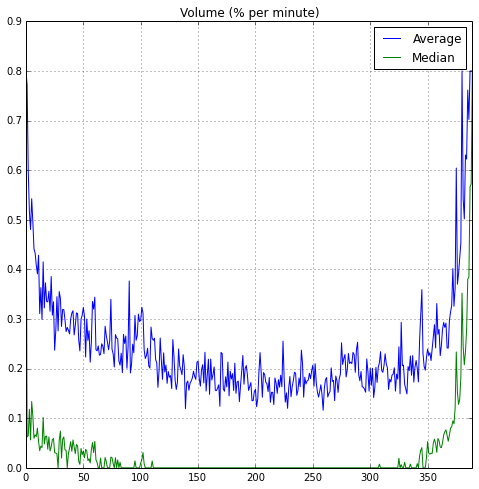

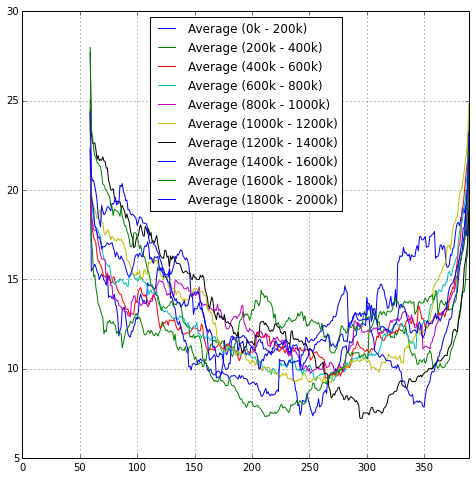

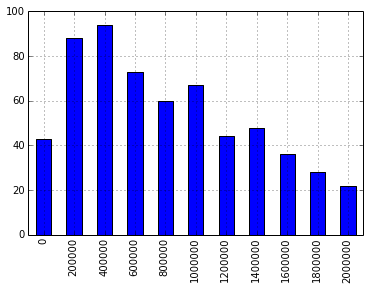

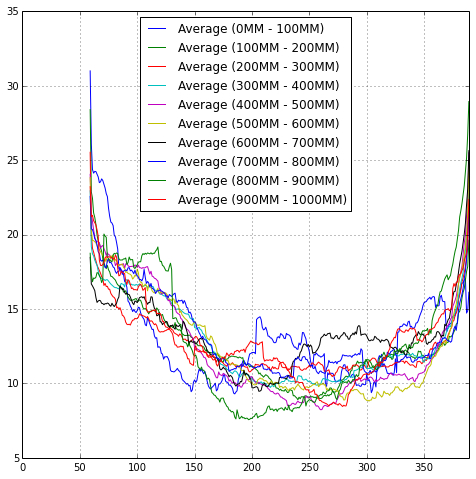

Second, the volume. The chart titled ‘Volume (% per minute)’ shows the percentage of daily volume traded each minute. What I mean by that is that, for each stock, I calculate the total volume on the day it should be bought/sold according to the recommendation, and then for each minute of that day I divide the volume of that minute by the total volume for the day. Those numbers are then aggregated per minute. So the chart shows that between 10:20 AM and 10:21 AM (after 50 minutes) the average volume is somewhere between 0.3% and 0.25% of the daily volume. (Btw, again, the numbers are limited. The opening volume 4.5% of daily volume, and the closing volume is 2.7% of daily volume).

Summarizing, the spreads are quite large in the first hour of trading, and narrow a little in the last hour. Volume is highest near the opening and closing, and many stocks do not trade much at all between 11:30 AM and 3:00 PM (median volume is 0, so half of the stocks has no volume at all).

Trying to trade at the open seems a good idea (if you’re careful with limits). But it also seems that if you want to trade higher volume you’ll have to trade either early or late in the day. Early in the day you’ll have (much) higher spreads, and later in the day our systems typically degrade in performance.