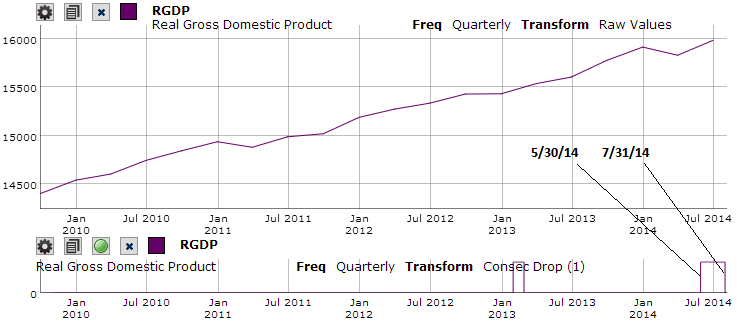

The MARKET->MACRO charts now generate point in time binary signals . Please see the attached image. It shows Real Domestic Product (quarterly data) and a binary transformation that evaluates to true when a q-to-q drop occurs.

As you can see the signal goes to true on 5/30/14 for Q1 that ended 3/31/14 and therefore appears shifted.

The raw values are shown point-in-time as of the end date of your chosen period, although the data date is labelled for the quarter date. It’s a bit confusing at first but there’s no good way to represent revisions

To see the actual value that triggered the binary signal enter end date of 5/30/14. You will see that Q1 was 15902.7 on that date. It has been recently revised lower to 15831.7, but 15902.7 was still a drop Q-to-Q

We will soon add more binary transformations, breadth indicators, custom series, and a way to use all this in simulations.

Q1 of 2011 appears like a drop TODAY, but that value has been revised. If you enter the end date of 9/1/2011 there was no drop, which is why the binary signal did not trigger

Marco - Something isn’t right with “smoothed U.S. recession probabilities” (RECPROB). When I add it to my MACRO chart, it erases my backtest chart prior to 9/4/12, as though the data for RECPROB doesn’t exist prior to that date, when in fact it does. If I take RECPROB out of the MACRO, the backtest chart reappears. You can see this in my MACRO chart “New Macro Chart”. This was working yesterday.

(BTW: Thank you very much for this functionality - it is very useful).

Debbie, please try it now. RECPROB was added to FRED around 2012, so all point-in-time start dates are 2012 onwards, even for very old data.

In these cases we estimate the average lag from recent data, however RECPROB seems to have an average lag of 2-3 months but it’s monthly data. We did not expect monthly data to have lags greater than 31 days. We now made the estimation of lag handle these unusual cases

OK - I get it - but it is confusing. Raw data chart is adjusted (unless you change the end date as you describe above) and binary transformations use point in time data. Perhaps there could be a toggle between point in time and adjusted data for the raw data.

“UNRATE Chg% (bars) greater than (pct)” is not working. When set at 12 bars, 0% it’s stuck on “1” since ~1960.

There is also a spelling mistake. “Chg% (bars)” should probably be “Chg (bars) greater than (pct)”. Although I may be missing the intent of this, which would explain both issues.