I have recently begun to wonder whether I should keep a port with EPS revsions. I will touch on my concerns but I’m not trying to make a point one way or the other. Also I would be happy with any opinion including just general impressions.

Outline of concerns:

P123 and Zacks earnings revision data are really different. Possibly (probably) the Reuters data is also different. Maybe that is okay. Maybe they are all good data just different criteria, analysts etc

CompuStat may be changing the data at a later date. Maybe this is okay because Marco is now taking snapshots. The fact that some of the data may be Reuter’s data does not make me fell better (see concern #1). However, they may not be doing this very often: perhaps just correcting errors.

I did take the earnings revision data out of one of my ranking systems and the sim still does very well: indeed, it does better over the last year even after switching from 5 to fifteen stocks. Is this because the last year has snapshot data or is it just fluctuation and noise? The 5 stock model does much better over the Max period: about 80% for the 5 stock model with earnings revision and 37% for the 15 stock model with no sentiment data whatsoever. The 15 stock model has much less turnover (Sell: Rank < 98 instead of RankPos <5) and a much higher Avg Return which I am beginning to think may increase robustness and the reduce severity of drawdowns (without much proof or experience).

Should I start using this last ranking system and scrap the EPS revision data. Or is the EPS revisions data still pretty good, if not perfect, and just hang in there for more out-of sample data?

I feel that EPS and expected EPS has significant value, but I don’t rely heavily on it. That is because the scatter in the data, especially analysis’s projections, become just noise when comparing 1 week to the next, or last month’s for that matter. I prefer a smoothing approach. We smooth prices, why not EPS? Even the S&P 500 EPS has a lot of scatter so we smooth that. The desire to get the very latest data (Who’s data, when is it actually available) has caused me to sell some very good stocks in the past just weeks before they make a good run (although they may have a few days loss before the turnaround).

From my own experience, forward EPS is still useful but earnings revisions are actually detrimental. I think earnings revisions is one of those factors that used to work but its efficiency has since eroded. When you think about it, analysts usually begin to revise earnings when the stock has already had a big move. It comes even latter than earnings surprise.

It probably works better with smaller stocks but given the economics in equity research, fewer shops are covering small caps. So the data are probably not even available.

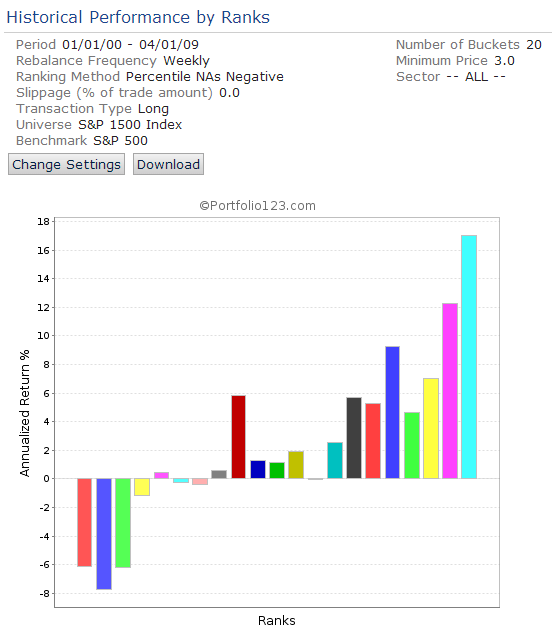

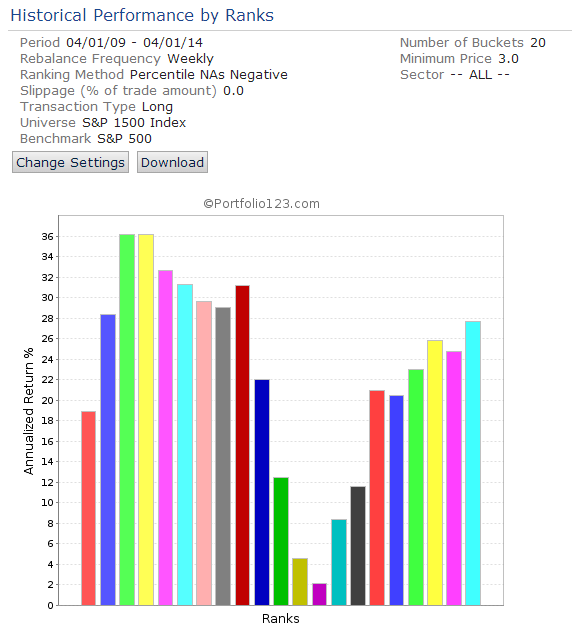

My own analysis suggests that the usefulness of earnings revisions has undergone a significant decline in the last 5 years. See the graphs attached, a simple ranking of CurFYEPSMean/abs(CurFYEPS4WkAgo).

Before hand it was quite an easy trade, now the impact is not zero, however, it certainly isn’t as straight forward as it was. I think something similair happened many years ago to earnings surprises, where the simple “buy into earnings surprise” was an effective trade - now it isn’t.

I think we need to be prepared for the fact that the market may become more efficient over time and close the gap on easy money - never has it been truer that “past performance is no guarantee of future results”.

P.S. unless you have about 50 positions in your simulation, trying to ascertain the usefulness of particular factors by adding/removing them is unlikely to give you a statistically confident result.

Oliver, great post as usual.

We need to be aware that “well working” variables will simply stop working at times that can only be determined in hindsight.

A few years ago it was all about a low “Price/Sales Ratio” and how “fabulous” it worked. It stopped working (well) soon thereafter. Now it is “earning revisions” that worked well for years and has lost its sex appeal. Zack’s has built its whole business on it.

As you pointed out, the markets are getting more efficient all the time, old “good looking” models with those factors stop working (and we don’t know when). A reason to look at models with high alpha with a good dose of scepticism.

Yup I think we also need to delve into why these things have worked in the first place. If it pays to buy into surprises or earnings revisions, that means the market is slow to react to the information. The time delay is what creates the window of opportunity for the trade. However, as the market processes the information more quickly the window of opportunity declines and the time delay may become zero - this is the limiting case in the “efficient market hypothesis”.

Perversely, if too many people are doing the “backtest” and it becomes a race to buy in as soon as the change is announced, it is possible the market will actually over-react to the news, in which case the thing works in reverse. Notice how the top bucket in the last 5 years is actually the bottom in the period 2000-2009 - I wonder if people were rushing in to short negative earnings revisions and now get caught in a short squeeze.

Personally I think the solution is to take the logic a step further, and try to ascertain what is an “appropriate” reaction and determine whether the market has under, or over reacted. That is a lot harder work, but then who said trading was easy?

Traditionally, revisions have been the major reason why investors have cared about any aspect of analyst data; those have been what moved the stocks. That said, as has been noted by others, times change. The sell side isn’t quite what it used to be so it’s not clear that revisions per se have the power they once did nor can we confidently assess how powerful they’re likely to be or not be going forward. But contrary to what others have said, this has nothing at all to do with market efficiency/inefficiency. It has to do with very real, clearly identifiable and well publicized ways in which the sell side has changed, as have its methods of developing estimates and its relationship with the companies it covers, the buy side and the financial media.

That said, I don’t think we’re anywhere close to the point where we should consider abandoning them. (Many things that don’t seem interesting in factor-usefulness studies actually turn out quite potent when one starts with an investing idea and then uses the factors and formulas to translate the idea into language that can be used on a computerized platform.) I’m still seeing situations where a model may require, as one of its elements, some sort of near-term catalyst and estimate revision is one thing among many that often contributes nicely. Essentially, estimate revision is one of many sentiment gauges we can use.

I was already leaning toward making some changes and your advice helped me decide. I will probably decrease the use of earnings estimate revisions in my ports, but I won’t throw the baby out with the bathwater.