You will get a security warning when you try to login. Some key points:

You must use the universe ‘All Fundamentals - CAN (BETA)’

Be sure to use something like Close(0)>1. Lots of penny stocks

We don’t have canadian indeces yet

Only run simulations/screen backtests. No live ports yet.

Only one server handles all requests, so sims will be slower

We are not handling Canadian holidays yet. Some results might be strange.

Please see the Help section for a brief intro to Canadian data (click on Canadian flag in BETA server)

Canadian data is NOT the same. A lot of companies have interim periods with missing data, so TTM ratios can be N/A even for things like SalesTTM

ALSO

The BETA server points to a completely rebuilt dataset, even for USA companies for things like estimates, revisions, insider, institutional. When we built the point-in-time data for Canada we also rebuilt USA to make sure all was ok. To our surprise some key estimate data, and others, did not match our snapshots that we take every week. The differences do not seem significant, and the differences only start after we switched to Compustat in July of 2012, so it has to do with live updates. The initial explanation form Compustat is the they are in fact “what the market knew”, and that it’s ok. But to be honest we did not fully understand their explanation and we’ll investigate further. I’ll have some examples tomorrow.

In any case, we’ll run tests all this week and next week. If you could use the BETA server for USA tests as well as Canada it would help us a lot (in exchange we’re not going to charge extra for Canada )

Sector Concentration

In your documentation you mention the concentration issue inside Financials, Energy, Materials. This highlights the importance of having sector weights data as we discussed earlier this week. I will give good examples: Info Tech used to be 33% of the index in 2000 and is now like 1.9% as of today. Energy used to be 13.2% in 2002 and is now 24.7% as of today. These are huge changes that we cannot take in consideration right now and I will not be able to sell an equal weight sim to any Canadian institutionals. Or even preset SecWeight levels are not gonna be helpful because it’s a look forward bias. You didn’t know in 1999 energy would be the double in weight. You didn’t know tech would collapse either.

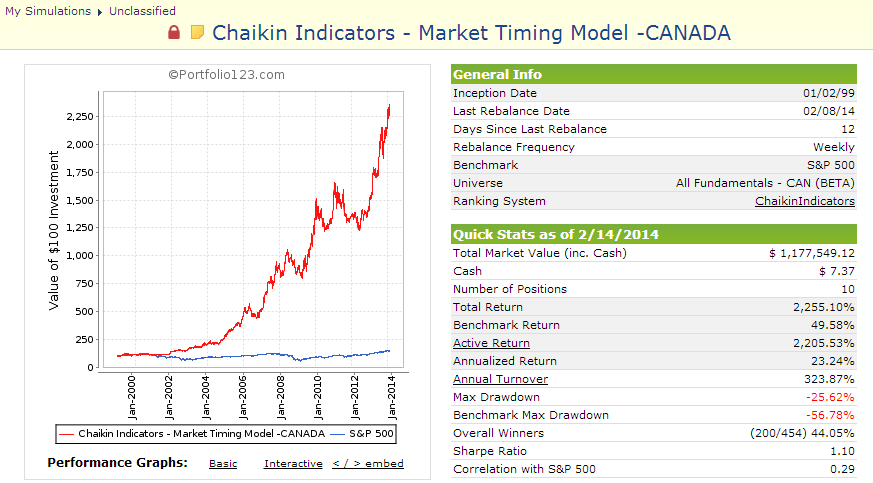

All, I ran one sim that is the same as one of my active ports. The Canadian results are much closer to my U.S out-of-sample returns than my over-optimized backtest for U.S. stocks. Correlation with S&P 500 was just 0.32.

aurelaurel - I don’t want to be a sourpuss but don’t forget that 400 of the 2200 stocks on the Canadian exchange (TSX?) are also traded on US exchanges. So there is a fair amount of overlap,

Great, thanks! I hope to take a look at it if I find the time.

[quote]

The BETA server points to a completely rebuilt dataset, even for USA companies for things like estimates, revisions, insider, institutional. When we built the point-in-time data for Canada we also rebuilt USA to make sure all was ok. To our surprise some key estimate data, and others, did not match our snapshots that we take every week. The differences do not seem significant, and the differences only start after we switched to Compustat in July of 2012, so it has to do with live updates. The initial explanation form Compustat is the they are in fact “what the market knew”, and that it’s ok. But to be honest we did not fully understand their explanation and we’ll investigate further. I’ll have some examples tomorrow.

[/quote]Marco, are you using your snapshots for the data since the switch?

Since you are finding differences between your database and Compustat it would indicate that you are snapshotting (is that a word?) the data as it comes in and using those PIT snapshots-which would be wonderful. Yet, there are differences between sims and live data (I mean besides for the fact that ports use Friday’s close) which would indicate that you are just using the Compustat data as is. Please clarify. Thanks.

Was afraid of that. I think it run out of memory with two universes loaded. We will probably need to upgrade all production servers before launching which will delay this a couple of weeks

FDP Demo - I ranked earning yield for canadian sectors instead of universe

The error about daily time series not translating properly to weekly signals. There has to be something up, I just don’t understand the logic behind it. How can something that triggers let’s say a Tuesday of week X, should in theory trigger a buy on monday of X+1, but instead triggers it on monday of X+2.