Marco, All:

I need help.

I’ve been a member for six weeks, and I’ve spent the first one hundred hours reading the threads that have been posted over the years. I’m extremely impressed with the intelligence, integrity and generosity of the community, and wish to express my gratitude to all who have shared their experiences here.

The problem I have seems to be a common one among newcomers: What’s in the bucket?

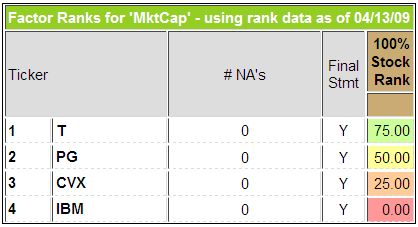

I ranked the Dow 30 by MktCap and set my Historical Performance Graph to output 30 buckets, thinking I should get one stock per bucket. I ended up with seven empty buckets. I thought the problem might be NAs or Final Statement Ns, but Johnson and Johnson was the only culprit, with one N. Nevertheless, I built three more universes of 30 stocks each, careful to ensure zero NAs and Ns, and I also ranked by another single factor, StockID, and also by a simple Ranking System named Momentum.

Not only did all my rankings return seven empty buckets, but they were always the same seven, counting from left to right: 6,11,14,21,24,27, and 30. Trying to simplify, I built universes of two stocks, three stocks, four stocks, etc., all the way up to 20, and then ranked using single factor Ranking Systems, matching the number of buckets with the number of stocks in the universe.

Universes containing two to ten stocks filled their respective matching buckets, but starting with my Eleven Stock Universe, things got weird, as they were with my 30 stock experiments.

For those of you who may wish to try replicating my results, here are the particulars:

Eleven Stock Universe: Buckets 6 and 11 Empty

Thirteen Stock Universe: Bucket 10 Empty

Fourteen Stock Universe: Buckets 10,12, and 14 Empty

Fifteen Stock Universe: Buckets 6,11, and 14 Empty

Seventeen Stock Universe: Buckets 12, and 16 Empty

Nineteen Stock Universe: Buckets 10,14,16 and 19 Empty

At one point I ran a Simulation on a five stock universe, using the same criteria I’d used on the Ranking, then turned to the Transactions:All section and calculated the return in the lowest bucket through four quarterly rebalances. The lone stock in the bucket changed at two different rebalances, and my computation of the Annualized Return matched the return shown for that bucket at the bottom of the Ranking>>Performance>>LOG Processing readout, which was great. I understand how that works now. The gain or loss in each bucket for a given period (3 months in this case) is calculated and added to the remaining periods; that number is then divided by the number of periods (4 in my experiment) to get the average return per period; finally, the average periodic return is “compounded” to arrive at the Annualized Return.

I am not able to conduct a similar test running a Sim using a Thirty Stock Universe because I buy 30 stocks at the inception and can’t identify what stock is or is not in an empty bucket. It doesn’t seem to matter how many rebalance periods I use, or the overall length of time the Sim or Ranking System runs. I still end up with seven empties. See the attachments. (If I can figure out how to attach them).

What Up?

(A Different) Denny