Oliver, thank you for the kind offer.

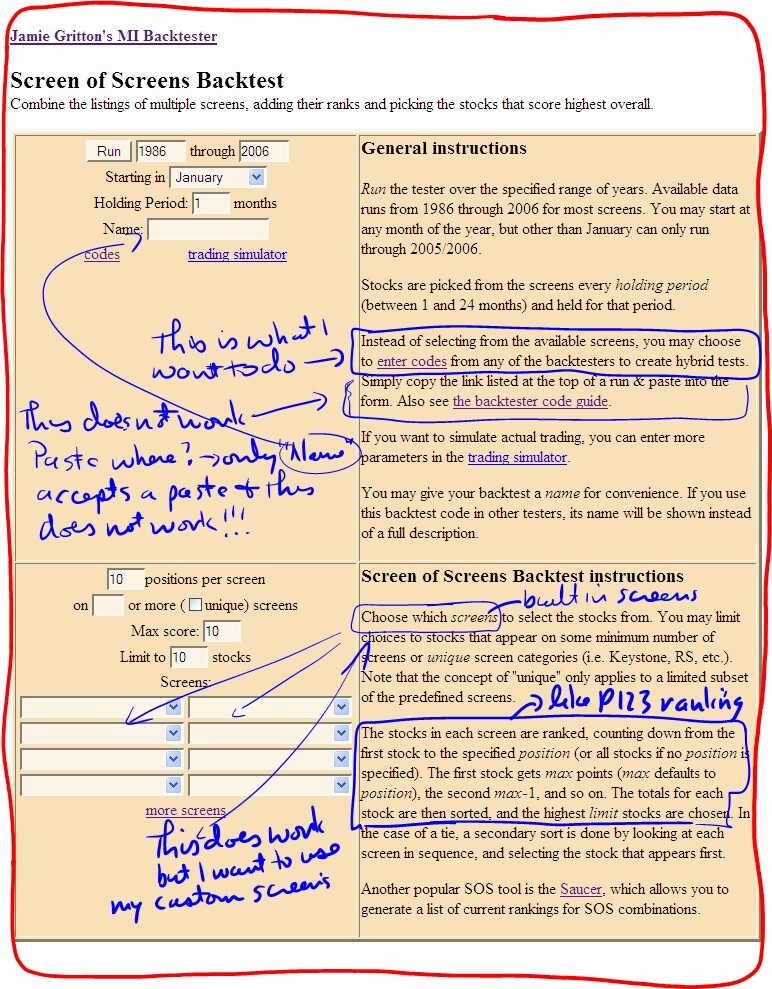

I may be trying to do something that is not possible in backtest.org (even though the documentation seems to state it is possible to do it.) What I am trying to do is get the SS (Screen of Screens) tester to run using my custom coded screens.

I can get the SS tester to run using their built in screens. I can even write the cryptic scripting code in URL format and have the SS tester automatically set itself up as specified in the URL formated codes (I give an example in more detail below).

Also I can get the SB (Screen Builder) tester to accept my custom written URLs. And the SB tester will run the test properly.

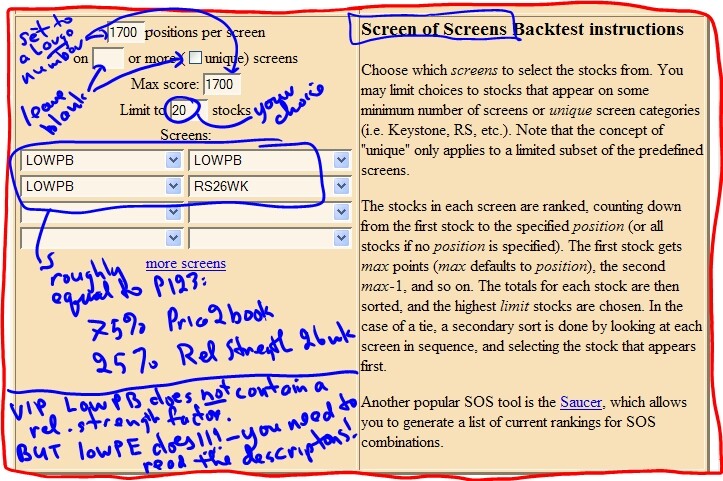

What I can not seem to get to work is to get the SS (Screen of Screens) tester to accept my custom built screens. I want to use the SS tester because it does MULTI-DIMENSIONAL RANKING in a very similar way to how Portfolio123 does. Although backtest.org does not use the term ranking in SS, the documentation says it numbers the position of each stock in each of the various “screens” specified and then totals the numbers before selecting the top stocks for rebalancing. That sounds very much like what Portfolio123 does. It should be noted that P123 is much more flexible since one can give different weights to various factors, but in backttest.org each “screen” (ie ranking factor) is given equal weight. But a workaround is to include a “screen” more than once in the list of screens and thus give it greater weight!!!

I am beginning to wonder if the SS (Screen of Screens) tester only works with built in screens – even though the set up page says one can substitute custom code for the built in code.

Do you know if I am trying to do something that is not possible in backtest.org?

OK, the above is the “executive summary” of the situation. Below explains it in more detail.

I am able to write the cryptic scripting URL that works for a single screen: For example I can write the following and it works:

http://www.backtest.org/9806SBprsrL1Xr26T20

This URL takes one to backtest.org which correctly decodes the 9806SBprsrL1Xr26T20 and sets the tester up to run for the dates 1998 to 2006 using SB (Screen Builder) with 2 screening rules: first “prsrL1” which means p2sales < 1 and those passing that screen are sorted by “r26” (26 week greatest total return, basically price appreciation plus dividends) and the “l20” (lower case L + 20, puts the top 20 stocks into the test portfolio). And when I click on “Run” the back test works as it should.

I will include a screen snap of the SS page. That page says a user can use “codes” instead of the built in screens. The page is not clear where one should paste in those codes, but there is only one field on the page that accepts pasting in, the “Name” field. And pasting the code into the Name field does not work.

Oh, I can get the SS tester to accept scripting coded into a URL if I am willing to just use the built in screens to do my ranking. For example,

http://www.backtest.org/SSpsrs999l20

This will open the SS tester and set up two ranking screens. The “ps” is the built in “PEG” screen (don’t ask my why they choose to use “ps” which sounds like price2sales to instead stand for “PEG”). The “rs” is the built in 26 week Return screen (I guess the “s” stands for semi-annual). The tester automatically selects ps and rs on two of the pull down boxes. It is all ready to go and it runs the test properly. I can place additional codes for other built in screens into the URL and this URL works properly when clicked on: the additional screens get added to the pull down screen boxes.

OK, back to the problem of trying to get the SS tester to accept my CUSTOM coded screens in place of those built in screens.

Here is the scripting code I want to run. This is a rather simple 3 screen code, but if I can get this simple one to work, I can easily build more complex ones.

SSOcpeCOr26COr13C9999l20

Here is the parsing of the above code using the rules specified on pages 3 and 4 of Backtest Codes.

SS invokes the Screen of Screen tester

OcpeC rank stocks by current p/e, remember the O and C stand for ( and ) parenthesis

This assumes one can use (cpe) type codes in place of the ss 2 char built in screens

Or26C rank stocks by 26 week total Return (I assume that is price + dividends)

Or13C rank stocks by 13 week total Return

9999 a nice high number just to be sure all stocks get ranked.

l20 sets the number of stocks in the portfolio to a maximum of 20.

And finally here is the pseudo English code (what I am trying to do in this simple model):

Invoke the SS tester,

1stScreen(rank by current p/e),

2ndScreen(rank by 26 week price appreciation),

3rdScreen(rank by 13 week price appreciation),

include all stocks in ranking by setting maximum stocks as 9999, select the top 20 stocks.

After spending a lot of time on this, I am beginning to wonder if the SS (Screen of Screens) tester only works with built in screens – even though the set up page says one can substitute custom code for the built in code.

Or is there a way to get SS (Screen of Screens) to accept custom screen definitions?

Thanks for listening.

Brian (o086)