I have been noticing some ports haven’t been performing that well in 2007, and I have been wondering why, but I think I have figured it out.

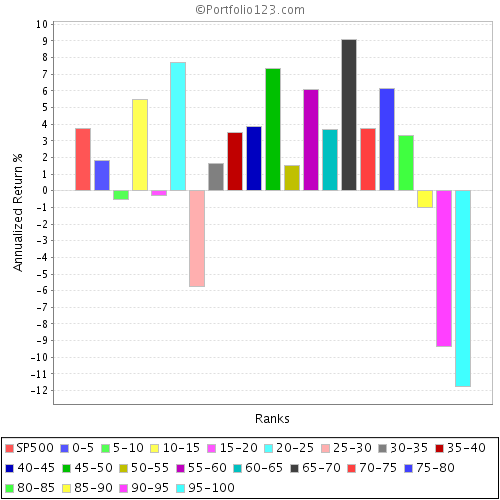

One of the most powerful factors has been Price-to-sales-quarterly in backtesting. But looking at the 2007 performance, the top decline has given negative performance. I attatch a graph showing this, four week rebalance with a minimum liquidity pre-screen: >$50m mktcap, >$200k daily turn, >$3 price.

I did wonder if this was the death of value.

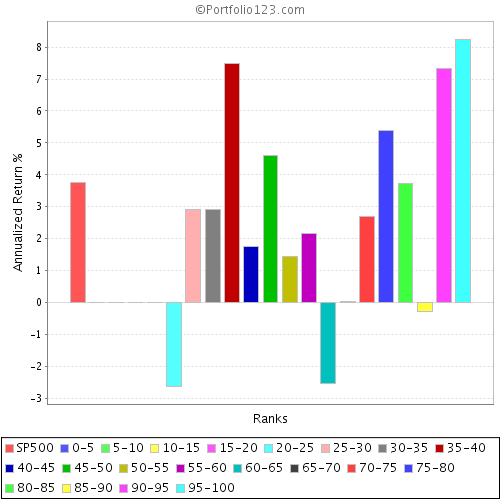

Interestingly, the same effect has not been true with Price-to-cashflow.

I just wonder if there has been something of a “bubble” in the low price-to-sales shares. As their performance has been good, people like us have piled into them driving up the price etc. etc. However, they have low ratios for a reason: Poor profit margins. Investors cannot “eat” sales, only what can be produced from them.

Perhaps the reason price-to-cashflow has not had the same problem is that investors can “eat” cashflow. Perhaps one should consider tweaking systems to favour cashflow measures over sales. On the other hand, I am always rather loathed to change trading systems based on recent performance, if you keep fiddling with the system then you can never expect to get good performance over the long run. Any thoughts?